Table of contents

- The Perp DEX Rush: From Niche to Billions

- Hyperliquid vs Binance: When David Trades Blows with Goliath

- Who Actually Trades Perp DEXs – and How?

- The Professional Traders: Code as Competitive Moat

- The Airdrop Farmers: Industrialized Automation

- The Retail Traders: Flying Blind

- The Tools Gap: What Retail Traders Are Missing

- The New Wave: Infrastructure Tools Closing the Gap among Perp DEXs and CEXs

- 🛠️ Hummingbot: The Engineering Approach

- 🛠️ Signum: The TradingView Bridge

- 🛠️ goodcryptoX: The All-in-One Trading Suite

- 🤖 Katoshi.ai: The AI-Native Specialist

- Choosing Your Toolkit: A Feature-by-Feature Comparison

- What's Still Missing on DEX Perp Trading Venues

- The Road Ahead: Infrastructure as the Real Disruption

- The Next Bull Cycle Thesis

- CeFi-DeFi Convergence & The Regulatory Wild Card

- Afterthought: The Infrastructure Revolution Is Already Here

Table of contents

- The Perp DEX Rush: From Niche to Billions

- Hyperliquid vs Binance: When David Trades Blows with Goliath

- Who Actually Trades Perp DEXs – and How?

- The Professional Traders: Code as Competitive Moat

- The Airdrop Farmers: Industrialized Automation

- The Retail Traders: Flying Blind

- The Tools Gap: What Retail Traders Are Missing

- The New Wave: Infrastructure Tools Closing the Gap among Perp DEXs and CEXs

- 🛠️ Hummingbot: The Engineering Approach

- 🛠️ Signum: The TradingView Bridge

- 🛠️ goodcryptoX: The All-in-One Trading Suite

- 🤖 Katoshi.ai: The AI-Native Specialist

- Choosing Your Toolkit: A Feature-by-Feature Comparison

- What's Still Missing on DEX Perp Trading Venues

- The Road Ahead: Infrastructure as the Real Disruption

- The Next Bull Cycle Thesis

- CeFi-DeFi Convergence & The Regulatory Wild Card

- Afterthought: The Infrastructure Revolution Is Already Here

The derivatives market has always been crypto's wild west – high leverage, 24/7 action, and billions in daily volume. For years, centralized exchanges (CEXs) owned this territory completely. But while Bitcoin ETFs and stablecoins grabbed the headlines in 2025, a quieter revolution unfolded in decentralized perpetuals (perp DEXs). Platforms like Hyperliquid didn't just chip away at CEX market share; they captured it at scale. This isn't just another DeFi trend. It's a fundamental market structure shift.

As of early November 2025, Hyperliquid processes approximately $3.66 billion in 24-hour perpetual volume, with open interest at $1.97 billion across 192 perpetual trading pairs and TVL exceeding $2.2 billion. However, explosive growth doesn't equal infrastructure readiness. Behind the impressive multi-billion dollar volume figures lies a complex reality where professional algo traders, hedge funds, and airdrop farming cartels armed with custom algorithms compete against retail traders wielding basic web interfaces. The real moat separating CEXs from the best decentralized exchanges isn't liquidity anymore. It's the tooling gap that keeps most traders flying blind.

This research paper will examine the evolution of perp DEX infrastructure, compare the key platforms and the emerging tools designed to close this gap, identify persistent challenges, and explore future trends to assess whether decentralized derivatives can achieve true parity with their centralized counterparts.

The Perp DEX Rush: From Niche to Billions

The trajectory of decentralized perpetual exchanges reads like a startup's fever dream. From niche experiments in 2023, dominated by players like dYdX v3 and GMX, which processed approximately ~$50B in monthly volume, the sector has exploded to processing over $1.3 trillion in monthly volume during 2025's peaks. On-chain derivatives have rewritten what seemed possible.

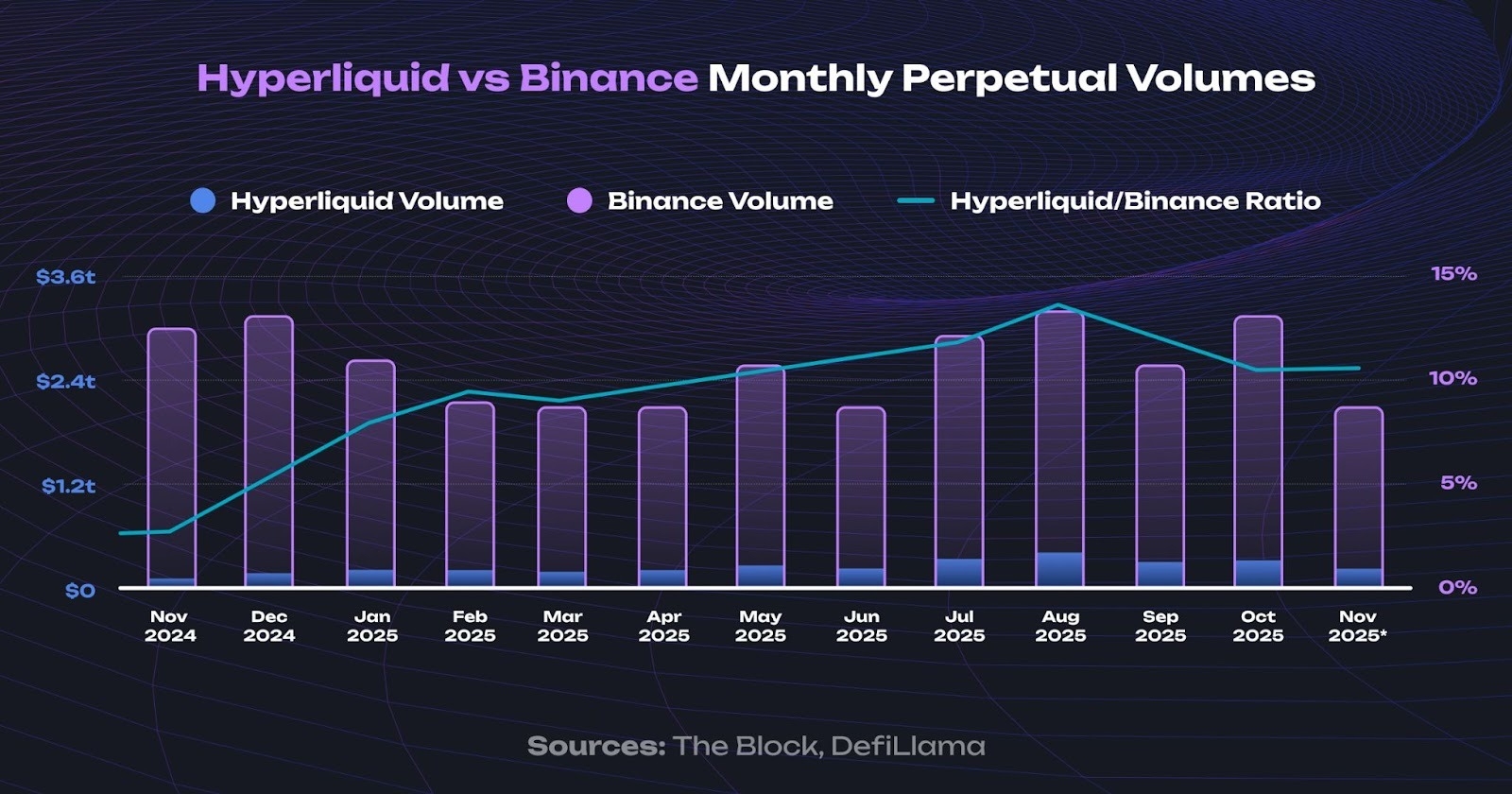

Today, Hyperliquid, alongside emerging competitors Aster and Lighter, have cemented themselves as the market's undisputed leaders. Collectively, this "power trio" generates over 70% of total perp DEX volume and captures nearly 90% of the sector's revenue. Hyperliquid alone, with its lean team of just 12 people, generated an astounding $321.7 billion in 30-day volume as of October 2025.

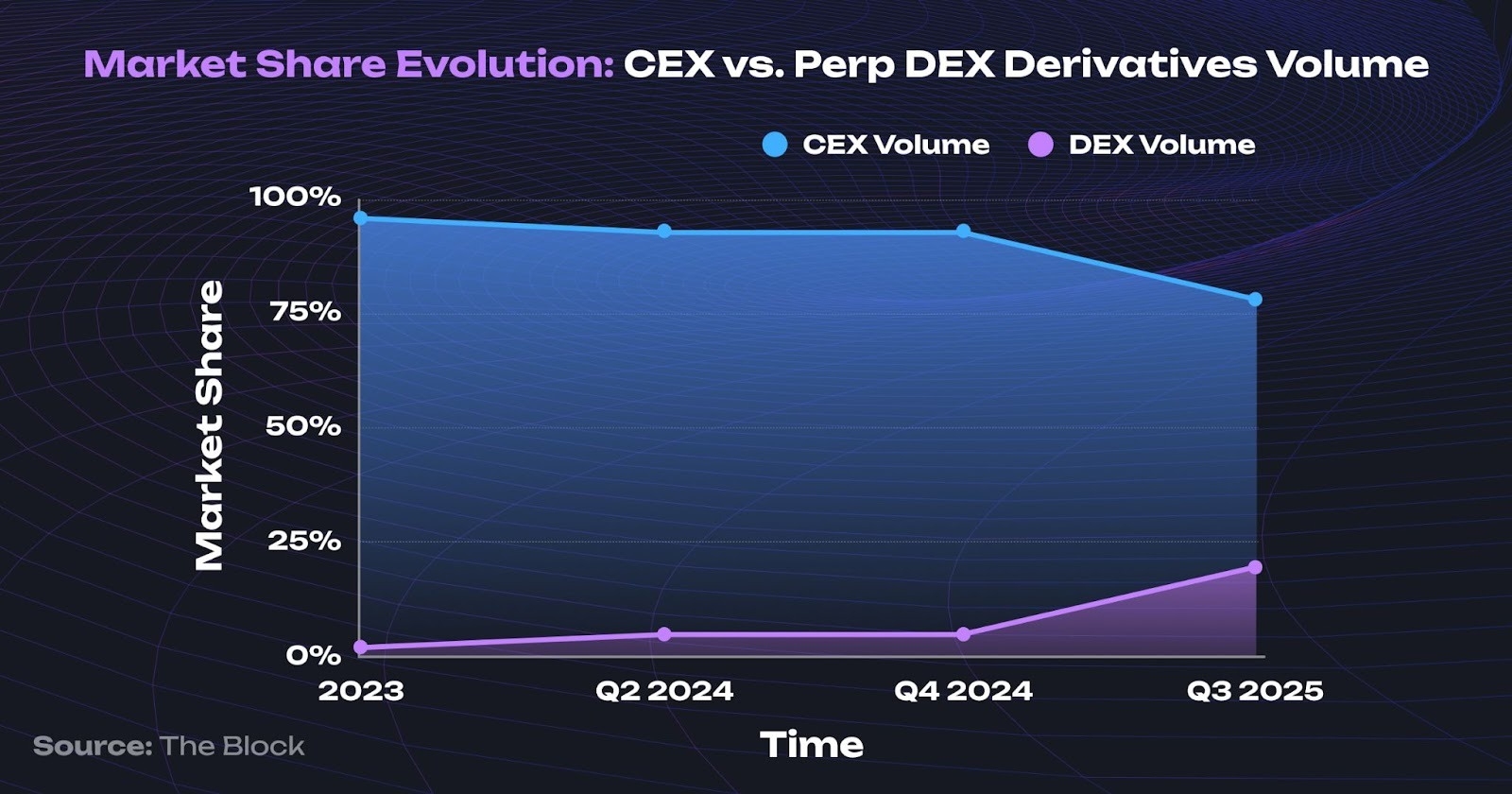

This market structure represents a massive evolution from the 2022–2023 era, when dYdX (v3) and GMX formed a duopoly. While revolutionary, they faced critical bottlenecks: dYdX’s reliance on StarkEx limited composability, preventing integration with other dApps, while GMX’s liquidity pool model struggled with scalability and risks during high volatility. Despite being the market leaders, perp DEXs in that era captured less than 3% of global open interest due to high latency and unpredictable costs. The new generation of high-throughput, fully on-chain orderbooks has effectively removed these barriers, allowing DEXs to finally compete for high-frequency volume.

And then there is Hyperliquid, a breakthrough in its own category. As the first dedicated perpetuals L1 blockchain, it was built for a single purpose: high-throughput, low-latency order book trading. For the user, this means its operation doesn't depend on Ethereum network congestion, for example, caused by a popular NFT mint. This ensures stable, low, and predictable fees, completely separate from Ethereum's gas volatility. This delivers a user experience that mirrors a CEX in speed and cost-effectiveness, now backed by institutional-grade liquidity, without sacrificing the core tenets of decentralization.

During various periods in 2025, Hyperliquid commanded over 70% of all perp DEX volume. By early November, fierce competition from rivals like the Aster perp dex had fragmented the market, reducing Hyperliquid's dominance to approximately 50%. While this validates the perp DEX thesis – that the market is vast enough for multiple giants – it also raises critical questions about volume authenticity. The key takeaway, however, is this: the top five perp DEXs now collectively hold a 20-30% slice of the entire global perpetuals market (CEX + DEX combined).

This surge is fueled by a fundamental shift in value proposition. Previously, traders paid a premium for decentralization; now, they get superior pricing alongside self-custody. With a fee structure of 0.035% for takers and just 0.01% for makers, Hyperliquid significantly undercuts incumbents like Binance (~0.10%), effectively reversing the historical cost advantage of centralized exchanges while maintaining a strict no-KYC policy.

Hyperliquid vs Binance: When David Trades Blows with Goliath

To fully appreciate this market structure shift, we must compare the leaders of both worlds: Hyperliquid, the pioneering on-chain orderbook DEX, and Binance, the undisputed centralized giant.

Metric | Hyperliquid | Binance |

|---|---|---|

24h Perp Volume | ~$7.58B (Nov 3, 2025) | ~$19.05B (all products) |

Open Interest | Not disclosed | |

Perpetual Pairs | 192 | 600+ |

Maker/Taker Fees | 0.01%/0.035% | ~0.10%/0.10% |

Custody | Self-custodial | Exchange-held |

By August 2025, Hyperliquid's volume reached ~11.89% of Binance's derivatives operations. Yet, a deeper analysis reveals a bifurcated market. Reports from firms like Oak Research estimate that 10–30% of total DEX volume is driven by "airdrop farming"sophisticated Sybil networks running automated, delta-neutral strategies across hundreds of wallets. This confirms that a significant portion of platform activity is not organic manual trading, but rather professional-grade automation, creating a stark divide between those with algorithmic tools and retail traders using basic web interfaces.

Who Actually Trades Perp DEXs – and How?

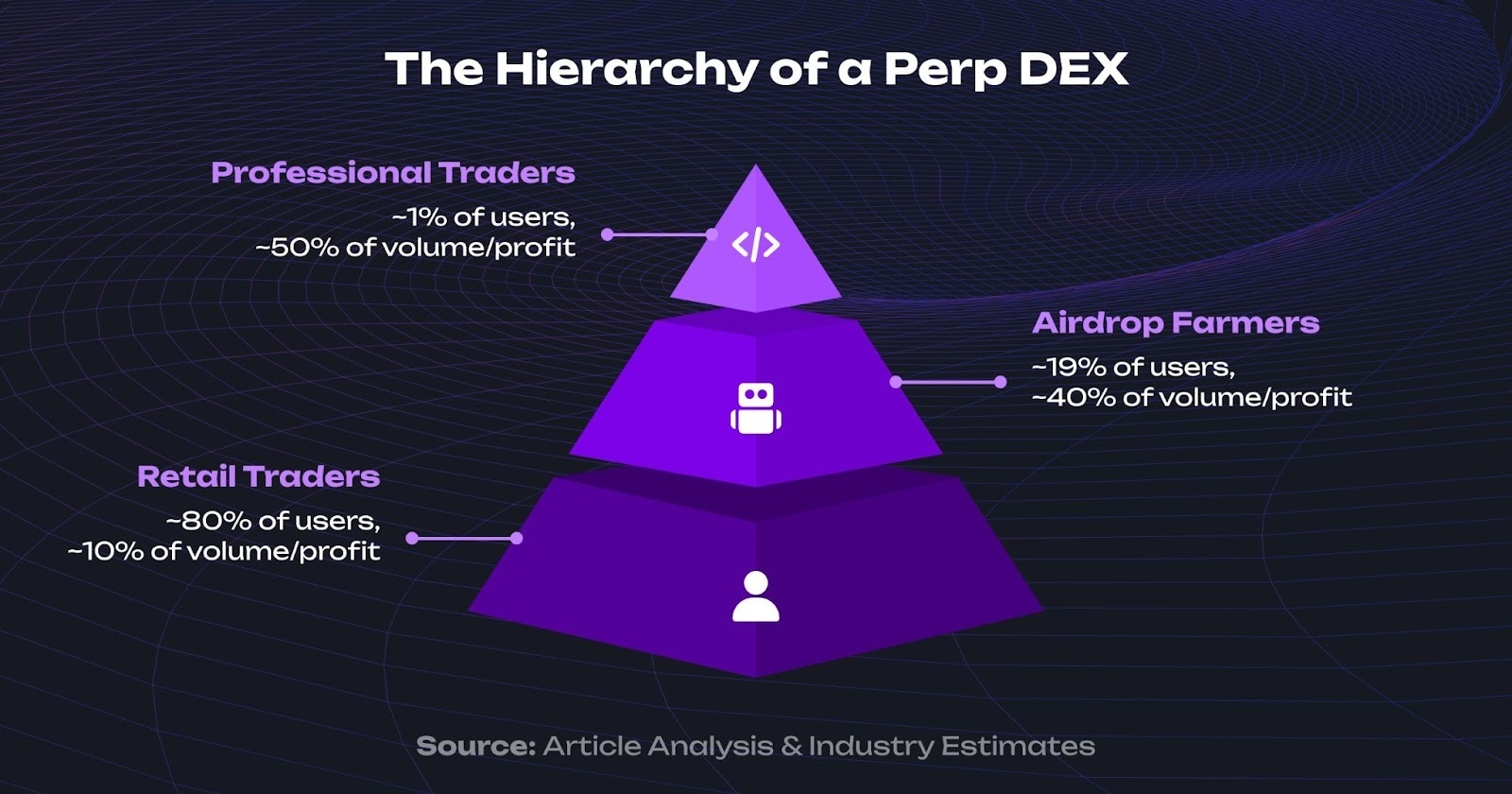

Visit any perp DEX's statistics page and you'll see billions in volume. Zoom in on the actual wallets, and the picture fragments into three distinct, warring factions with vastly different capabilities. It's not a level playing field; it's a hierarchy of technological advantage.

❗️Spoiler: Our research suggests that API trading, essentially automated trading, makes up about 90% of Hyperliquid’s total volume.”

The Professional Traders: Code as Competitive Moat

At the top of the food chain sit quantitative funds and market makers who rely on custom high-frequency systems rather than web interfaces. A prime example is Wintermute, which actively trades on Hyperliquid. According to Pitchbook data, they employ over 140 people and are constantly hiring specialized C++ developers. This immense investment in talent forms the baseline for professional competition.

The brutality of this arena is illustrated by a story from trader CBB. While he initially earned $5M with a simple arbitrage bot, superior infrastructure from entering giants systematically compressed his edge to zero. It’s a harsh lesson in on-chain capitalism: even a winning strategy fails when you are outgunned on tooling.

The Airdrop Farmers: Industrialized Automation

Below the institutional titans are the airdrop farming operations – vast, automated Sybil networks that are less traders and more industrial-scale system abusers. The economics are brutally simple: as detailed by publications like BeInCrypto, perp DEXs launch tokens with generous airdrop allocations to bootstrap liquidity, and these airdrops almost always reward one metric above all else: trading volume.

Farmers recognize this loophole and build systems to generate maximum volume with minimum capital risk. The MYX exchange incident, where attackers allegedly captured a staggering $200 million in tokens, illustrates the terrifying scale of these professional operations.

The airdrop farming phenomenon creates data reliability challenges. Some platforms have faced scrutiny over volume authenticity – Aster, despite its rapid growth, was temporarily delisted from data aggregators amid wash trading concerns. This highlights a critical caveat: not all reported volume represents genuine trading activity. Moreover, these automated Sybil cartels leave retail traders with virtually no chance of earning fair airdrops through honest, organic manual trading.

However, not all automation is malicious. Some sophisticated algo providers run transparent operations, using tools to manage hundreds of positions. These legitimate operations have documented performance ranging from 400-2000% APY during favorable market conditions.

The Retail Traders: Flying Blind

Then there's everyone else. The retail traders who were promised a democratized financial future. They face a cruel paradox: they chose decentralization for self-custody and transparency but ended up with an objectively worse, more predatory trading experience.

Their workflow is a manual, stressful grind:

- Open a position through a clunky web interface.

- Set a basic stop-loss and take-profit, hoping they execute correctly.

- Stare at the screen, constantly monitoring (because there's no reliable mobile app).

- Manually adjust as the market moves, always a step behind the algorithms.

- Go to sleep and pray they don't get liquidated.

No trailing stops. No DCA strategies. No grid bots, no scalping bots, no technical indicator strategies, and many more. The result is a structural massacre. Since trading is a zero-sum, PvP (player-versus-player) game, the two advanced groups – the professionals and the farmers – systematically extract value from the least equipped participants. They don't just win; they win because retail loses.

The Tools Gap: What Retail Traders Are Missing

While liquidity on Hyperliquid now regularly exceeds $7+ billion, proving on-chain order books can handle institutional scale, a vast tooling gap remains. This stems from a strategic division of labor: protocols focus on building the settlement rails, leaving the user infrastructure layer to specialized third parties.

The execution disparity is stark. CEX traders operate with an arsenal of native advantages – algorithmic orders (TWAP, Iceberg), automated Grid/DCA bots, and mobile apps. In contrast, the typical native experience on a perp dex exchange is limited to basic market/limit orders and raw API access, forcing retail traders to compete manually in an automated market.

Feature | Hyperliquid (Native) | Binance (Native) |

|---|---|---|

Advanced Orders | Scaled Order, TWAP ⚠️ | TWAP, Iceberg, OCO, Trailing, Conditional, Scaled, Algo ✅ |

Built-in Trading Algo & Bots | None ❌ | Grid, DCA, Rebalancing, Arbitrage, Copy Trading, etc. ✅ |

Strategy Automation | API only. Complicated with no clear UI/UX. Web only. ⚠️ | Built-in + API ✅ |

Mobile App | Web wrapper (mobile-optimized web version) ⚠️ | Native app (iOS & Android) ✅ |

Analytics | Basic P&L ⚠️ | Comprehensive with visualization ✅ |

The architectural advantages of self-custody are undermined by raw execution friction. This isn't just an inconvenience; it creates an uneven playing field where, as highlighted in reports like Binance Research's "Navigating DeFi Derivatives", perp DEX liquidations can be significantly higher than on CEXs during volatile periods, directly because of this infrastructure gap.

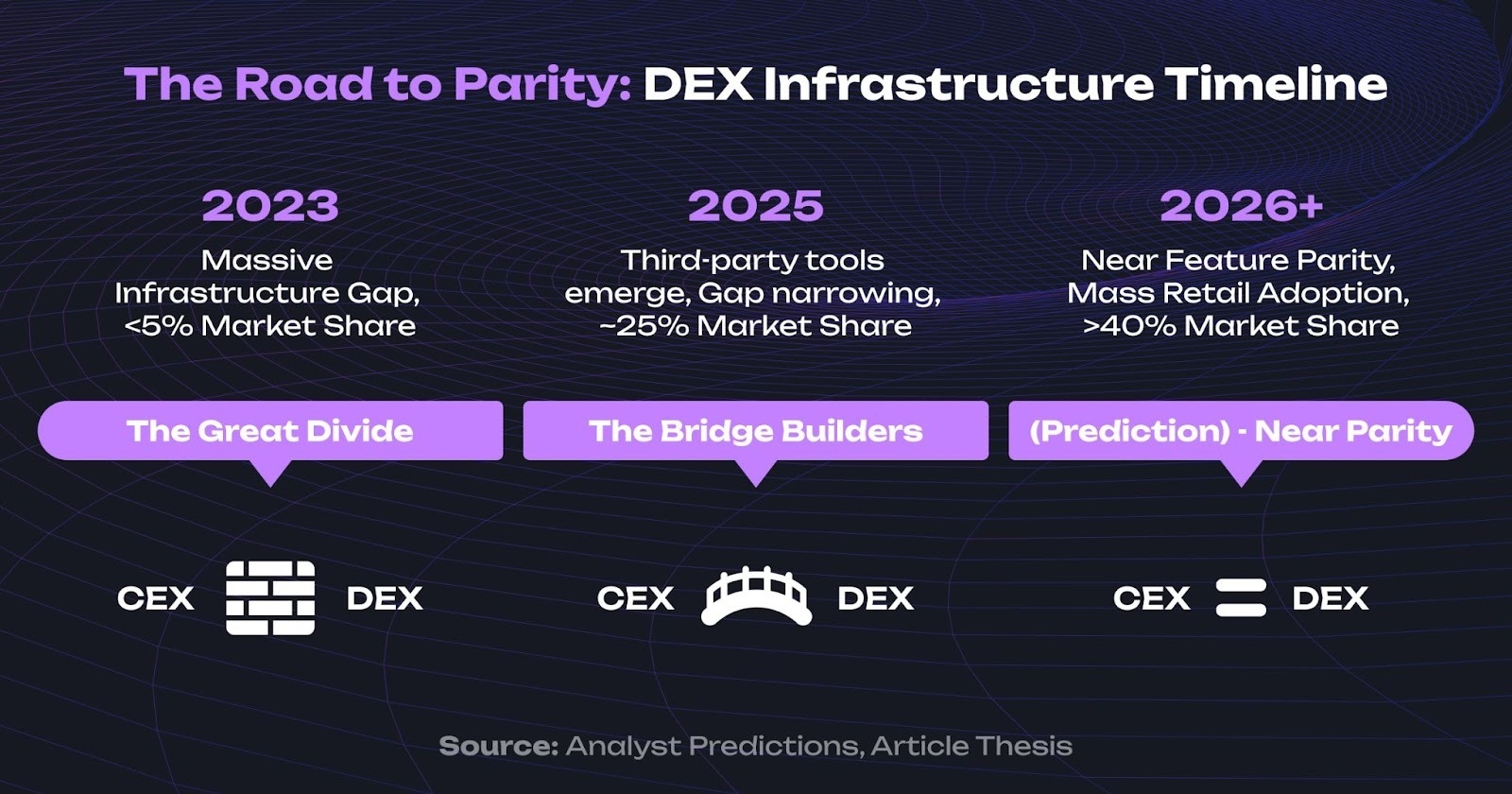

The New Wave: Infrastructure Tools Closing the Gap among Perp DEXs and CEXs

The infrastructure gap isn't closing by accident. A new generation of tools has emerged to bridge the chasm – not by changing the underlying DEX protocols, but by building the meta-layer that makes dex trading on perp decentralized exchanges actually usable. They're the picks and shovels of the on-chain derivatives gold rush, and they all support Hyperliquid.

🛠️ Hummingbot: The Engineering Approach

Hummingbot is the go-to choice for developers and quantitative traders who demand absolute control. It enables developers to code any type of algorithm via its terminal and connect it to a wide range of DEXs and CEXs.

- Core Functionality: Market making strategies with configurable spreads, arbitrage bots across multiple venues, custom strategy development via Python, and a community-contributed strategy library. It has integrations to over 30 DEXs and 50+ CEXs.

- Foundation and Traction: Founded in 2017, Hummingbot is a veteran with a large, established community and has facilitated billions in trading volume.

- Target Audience & Usability: This is not for general developers or casual traders. Its primary audience consists of professional market makers, small hedge funds, and "algo geeks" – tech-savvy traders who enjoy building and customizing their own bots in Python. The learning curve is steep, requiring a terminal-based setup and a deep understanding of both coding and market dynamics Reddit threads asking "Has anyone made actual money?" reveal the gap between theoretical capability and practical execution.

- Capabilities & Support: Its core strength is limitless customization for market-making and arbitrage,

- Security: Security relies on community-driven reviews. No public audits by security firms.

- Pricing: Free, open-source, and self-hosted, offering maximum control.

🛠️ Signum: The TradingView Bridge

Signum is a specialized tool for advanced TradingView analysts who want a simple bridge to execute strategies on-chain. It lets traders execute TradingView strategies on crypto exchanges.

- Core Functionality: Direct TradingView alert integration, strategy automation from Pine Script indicators, and multi-exchange support.

- Foundation and Traction: Launched in 2024, it's a newer player with limited public traction data but is gaining popularity.

- Target Audience & Usability: The learning curve is "configure webhooks," not "code." It’s for traders who've mastered and regularly applied TradingView. However, the interface is minimal to a fault. Complex multi-leg strategies or sophisticated portfolio-level position sizing require capabilities beyond simple webhooks.

- Capabilities & Support: Functionality is entirely dependent on TradingView alerts. It supports Hyperliquid along with multiple CEXs.

- Security: A closed-source, subscription-based service ($25/month) with no publicly available audits in 2025.

- Pricing: Subscription-based service ($25/month).

🛠️ goodcryptoX: The All-in-One Trading Suite

goodcryptoX, which has been rebrended from GoodCrypto, is a comprehensive suite aiming to bring CEX-level convenience to DEX trading, also offering a trading terminal, screener, and portfolio analytics. It is effectively a powerful Hyperliquid trading bot and much more.

- Core Functionality: It offers pre-built bots (Grid, DCA), TradingView Strategies integration. A comprehensive trading terminal and DEX Screener for real-time token discovery and Multi-Account Management for controlling up to 50+ accounts.

- Foundation and Traction: Active since 2019, the platform has a proven track record. It's experiencing rapid growth, with the cumulative trading volume of over $5B since its launch. goodcryptoX has experienced a 9.3x increase in DEX trading volume since March this year.

- Target Audience & Usability: It’s for retail traders wanting professional automation without coding; airdrop farmers managing multiple accounts efficiently; traders seeking CEX convenience with DEX self-custody; anyone tired of manual position monitoring. A no-code visual interface, native iOS/Android apps, and minutes-long setup make it the most accessible tool. A retail trader can deploy any bot strategy on Hyperliquid in minutes – choosing parameters like price step multiplier, order size, take-profit percentage – without writing code. The visual interface guides configuration while maintaining sophisticated functionality under the hood.

- Capabilities & Support: It supports 30+ centralized exchanges and multiple DEX chains for spot trading (Solana, Base, BSC).

- Security: Non-custodial, audited by Certik, and runs a bug bounty program. The non-custodial architecture is a critical security feature: it means the platform never takes control of your funds. Your assets remain in your own wallet, and the tool only executes trades that you authorize, eliminating the risk of exchange hacks or freezes that plague centralized platforms.

- Pricing: All PRO features including trading bots are completely free when trading on Hyperliquid and other supported DEXs”

🤖 Katoshi.ai: The AI-Native Specialist

Katoshi.ai is a new-generation tool focused on leveraging AI, positioned for high-volume professionals on Hyperliquid.

- Core Functionality: AI-driven signals, automated execution based on predictive models, and sentiment analysis.

- Foundation and Traction: Founded in 2024, it is an emerging tool that is gaining attention within the Hyperliquid community.

- Target Audience & Usability: While it has a no-code interface, its complex credit system and custom scripting language are geared towards quants and traders interested in experimenting with AI and data-driven approaches.

- Capabilities & Support: It is focused exclusively on Hyperliquid.

- Security: A closed-source platform with no public audits in 2025.

- Pricing: Its credit-based pricing allows for zero-fee trading via a "Vault Bot," a powerful but complex feature.

Choosing Your Toolkit: A Feature-by-Feature Comparison

Feature / Criteria | Hummingbot | Signum | goodcryptoX | Katoshi.ai |

|---|---|---|---|---|

Founded | 2017 | 2024 | 2019 | 2024 |

Target Audience | Market Makers, Developers-Algo Geeks | TradingView Users | Retail to Pro, Farmers | High-Volume Quants |

Setup Time | Days or Hours for Tech PRO ❌ | Hours ⚠️ | Minutes ✅ | Hours ⚠️ |

Pricing Model | Free & Open-Source ✅ | Flat Subscription ⚠️ | Free for DEXs, Freemium for CEXs ✅ | Credit-based (Pay to lower fees) ⚠️ |

Pre-Built Strategies | Community library ⚠️ | Paid Trading View Strategies ⚠️ | Grid, DCA, Trailing ✅ | AI-suggested ⚠️ |

Multi-Account Mgmt | Manual setup ⚠️ | No ❌ | 50+ accounts ✅ | No ❌ |

Mobile App | Terminal only ❌ | No ❌ | iOS & Android ✅ | No ❌ |

Multi-DEX Support | 30+ DEXs ✅ | Hyperliquid only ❌ | Hyperliquid, Solana, Base, BSC, ETH ✅ | Hyperliquid only ❌ |

Traction | Established, $34B+ volume ✅ | Limited data, niche growth ⚠️ | 400K+ users, $5B+ volume ✅ | Early stage, emerging player ⚠️ |

Security | Open-source, Community-reviewed ⚠️ | Closed-source, No public audit ❌ | Certik Audited, Bug Bounty ✅ | Closed-source, No public audit ❌ |

Key Takeaways:

- For Maximum Control: Hummingbot is unbeatable if you can code.

- For TradingView Purists: Signum and goodcryptoX are a purpose-built bridge, while later provides a friendly UX/UI and available on mobile.

- For Daily Usability & The Best Value: goodcryptoX is the clear winner for the vast majority of users. It dominates on ease of use, multi-account management, mobile access, and offers an unbeatable proposition: all its powerful DEX trading features are completely free.

What's Still Missing on DEX Perp Trading Venues

Despite significant progress, critical gaps remain:

- Portfolio Margin Across Protocols: CEXs offer unified margin across products within one exchange. DEX traders can't use Hyperliquid collateral for a GMX position.

- Institutional Custody + Automation: Enterprises need multi-sig wallets with automated trading capabilities.

- Advanced Social Trading: Binance lets you automatically mirror traders. While goodcryptoX offers strategy sharing, true one-click copy trading is underdeveloped.

- Comprehensive Backtesting Infrastructure: CEXs provide built-in historical data. For DEXs, this is still a fragmented process.

It's worth noting that some gaps are closing faster than others. goodcryptoX's native mobile apps and DEX screener demonstrate how retail-focused tools can already match or exceed CEX capabilities.

The Road Ahead: Infrastructure as the Real Disruption

The narrative around perp DEXs usually centers on decentralization, self-custody, and transparency. But the practical disruption happens when DEXs achieve feature parity with CEXs.

The Next Bull Cycle Thesis

The next bull cycle's biggest winners won't be platforms with the most TVL – they'll be the infrastructure plays solving the tooling gap. The picks and shovels outperform the gold miners. As a pivotal report from The Block highlighted, venture capital is now chasing revenue-generating startups, and exchanges are among crypto’s most profitable businesses. This confirms the thesis: long-term value will accrue not just to protocols, but to the sticky, indispensable infrastructure tools that give traders a real reason to stay.

CeFi-DeFi Convergence & The Regulatory Wild Card

Within 18-24 months, the infrastructure gap will shrink from an unbridgeable chasm to a manageable trade-off. As highlighted in Messari's definitive State of Solana Q3 2025 report, this trend is undeniable. The institutional capital flowing to DEXs for practical reasons: lower fees, composability, and settlement transparency

However, regulation remains the key variable. Increased scrutiny could force platforms to implement KYC, but regulatory clarity could also accelerate institutional adoption. Yet, real obstacles persist. The risks of using third-party tools are significant and include code bugs causing erroneous trades, server downtime preventing users from managing positions during critical moments, and exploits that could lead to fund theft via compromised integrations, as seen in past DeFi hacks. Since there is no centralized entity to "return" funds, the need for audited, robust tools is paramount.

Afterthought: The Infrastructure Revolution Is Already Here

The numbers tell one story: perp DEXs have captured a massive, undeniable market share that seemed impossible two years ago.

But the real story is the infrastructure emerging to support them.

For years, the choice was a bitter trade-off: accept worse tools in exchange for self-custody. That bargain is expiring. Platforms like goodcryptoX, Hummingbot, Signum, and Katoshi are collectively closing the tooling gap, bringing CEX-grade automation to on-chain trading without compromise.

The perp DEX wars won't be won by the fastest chain or the deepest liquidity pool. They will be won by the ecosystem that makes every trader – regardless of technical skills or capital – feel like they're trading with professional infrastructure.

The gap is closing. And when it does, the question won't be whether traders choose a CEX or a DEX.

It'll be why they'd ever choose to surrender custody again.

Disclaimer: This article contains information about cryptocurrency trading, which involves significant risk. Market data is current as of November 2025, but volumes and market shares fluctuate. The APY returns mentioned represent specific, optimized user experiences during favorable market conditions and are not typical results. Trading can result in substantial losses. Volume figures may include wash trading. Always conduct your own research and never invest more than you can afford to lose. This article does not constitute financial advice. Automation does not guarantee profits. The regulatory landscape for decentralized derivatives is evolving.

Research

Jason Shaw

July 31, 2026

14 min

The Best Crypto Marketing Agency for 2026: Our Insider's Shortlist backed by Real Reviews and Case Studies

Research

Daniel Bennett

July 30, 2026

15 min

The 10 Best Web3 Marketing Agencies of 2026, Ranked by 220+ Verified Reviews and Real Case Data

Research

Daniel Bennett

July 27, 2026

19 min

9 Top Crypto SEO Agencies of 2026, Backed by Client Interviews and Case Studies

No Comments

No comments yet