Table of contents

- What Is Bitcoin Loan and How Does It Work?

- Why Do People Borrow Against Bitcoin Instead of Selling It?

- Best Platforms by Bitcoin Lending Rates: Comparative Table

- Sats Terminal

- Nexo

- Ledn

- Lava

- Debifi

- Fuji Money

- Conclusion: What Is the Best Bitcoin Lending Platform?

Table of contents

- What Is Bitcoin Loan and How Does It Work?

- Why Do People Borrow Against Bitcoin Instead of Selling It?

- Best Platforms by Bitcoin Lending Rates: Comparative Table

- Sats Terminal

- Nexo

- Ledn

- Lava

- Debifi

- Fuji Money

- Conclusion: What Is the Best Bitcoin Lending Platform?

According to estimates by Ledn and Protocol Theory, the consumer market for Bitcoin-backed loans is currently worth approximately $3 billion and could grow to $1 trillion within 5 to 10 years, according to the CDN prod report. Interest in Bitcoin lending is also growing: 88% of surveyed crypto holders would consider a loan secured by digital assets, while only 14% currently use one.

Bitcoin lending platforms give investors access to liquidity without selling their BTC. Users deposit BTC as collateral, receive USD, USDC, or another asset, and maintain exposure to Bitcoin. But this is not free money. Each platform has its own Bitcoin lending rates: LTV, margin call, liquidation threshold, fees, and collateral storage model.

With so many variables, choosing the best Bitcoin lending sites becomes nearly impossible. That’s why we’re here to help.

This guide breaks down the best platforms to borrow against Bitcoin 2026: CeFi services, DeFi aggregators, non-custodial protocols, and Bitcoin-only solutions. We’ll compare them based on Borrow APR, BTC Lending APY, Max LTV, Margin Call LTV, Liquidation LTV, fees, loan terms, custody models, and best use cases.

What Is Bitcoin Loan and How Does It Work?

A Bitcoin loan is a loan secured by BTC. Users do not sell their Bitcoin. Instead, they lock it as collateral and receive funds, most often in USD, USDC, or another fiat currency or stablecoin. This type of loan is used by investors who want to maintain exposure to BTC while accessing funds for expenses, business, hedging, or other strategies.

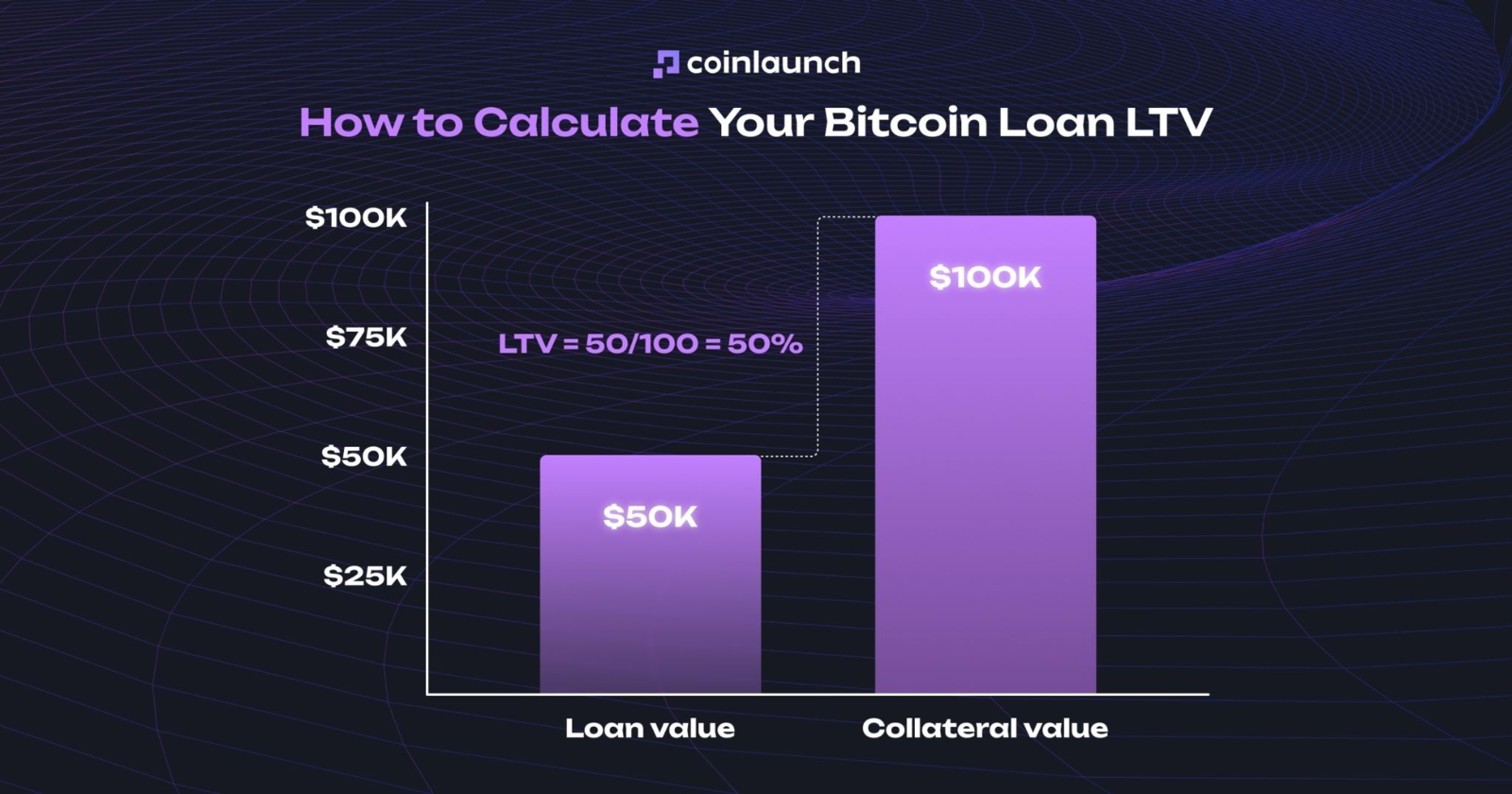

The mechanics of Bitcoin loan sites are based on LTV, the ratio of the loan amount to the collateral value. If BTC is worth $100,000 and the platform offers a 50% LTV, the borrower can receive $50,000. The higher the LTV, the larger the available loan amount, but the higher the liquidation risk.

How to calculate Bitcoin loan LTV. Source: coinlaunch.space

To borrow funds, the user pays an APR, the annual cost of the loan, including interest and fees. Terms vary by platform: in CeFi, collateral is held by a custodial service; in DeFi, it is held in a smart contract. Multi-signature or a separate escrow mechanism may also be used.

If the price of BTC rises, the LTV decreases: the collateral becomes more valuable, and the position becomes safer. If the price falls, the LTV increases. Once it reaches a certain level, the platform issues a margin call and requires the borrower to add collateral or partially repay the Bitcoin backed loan.

If the borrower fails to meet the margin call and the price continues to fall, the position is liquidated: the platform sells part of the BTC collateral to close the loan.

Why Do People Borrow Against Bitcoin Instead of Selling It?

The main advantage of borrowing against Bitcoin is access to liquidity without having to sell BTC. The borrower receives funds while maintaining exposure to Bitcoin. If the asset’s price rises after the loan is taken out, the user continues to benefit from that appreciation. Selling BTC means losing that opportunity: the position is closed, and re-entering the market may become more expensive.

A Bitcoin loan can also be used as a risk management tool. For example, a borrower can access liquidity against BTC and open a hedge in the futures market to partially offset a potential price drop. However, they must account for the APR, fees, funding rate, and potential liquidation threshold if the market moves against the position or the LTV rises sharply.

Best Platforms by Bitcoin Lending Rates: Comparative Table

Platform | Sats Terminal | Nexo | Ledn | Lava | Debifi | Fuji Money |

BTC Borrow APY | from 3.65% | from 1.9% | 9.99%-11.49% | ~7.0% | from 9% | N/A |

BTC Lend APY | Up to 1.36% | Up to 4.70% | N/A | N/A | N/A | N/A |

Max LTV | 71% avg | 50% | 50% | 60% | 70% | N/A |

Margin Call LTV | Protocol-based | 71.40% | 70% | 70% | 75% | N/A |

Liquidation LTV | Protocol-based | 83.33% | 80% | 80% | 90% | 66.67% |

Origination Fee | No platform fee | None | 2% | 2% annual capital charge | 1%-1.5% + duration fee | Minting fee |

Loan Term | Provider-based | Open-ended | 12 months | Open-ended | 1-24 months | Open-ended |

Custody Model | DeFi aggregator | CeFi | CeFi | CeFi | DeFi lending marketplace | DeFi |

Requires KYC | No | Yes | Yes | Yes | Protocol-based | No |

Best For | BTC loan aggregation | Large Bitcoin backed loans | Bitcoin-only users | Bitcoin crypto-banking | Non-custodial BTC loans | L-BTC synthetic loans |

Not all protocols let users earn interest by lending Bitcoin. Some platforms do not offer an interest-earning feature, while others operate through stablecoins such as USDC. Therefore, “N/A” in the “BTC Lend APY” category means that BTC lending is not available on that platform. The exceptions are Sats Terminal and Nexo.

Sats Terminal

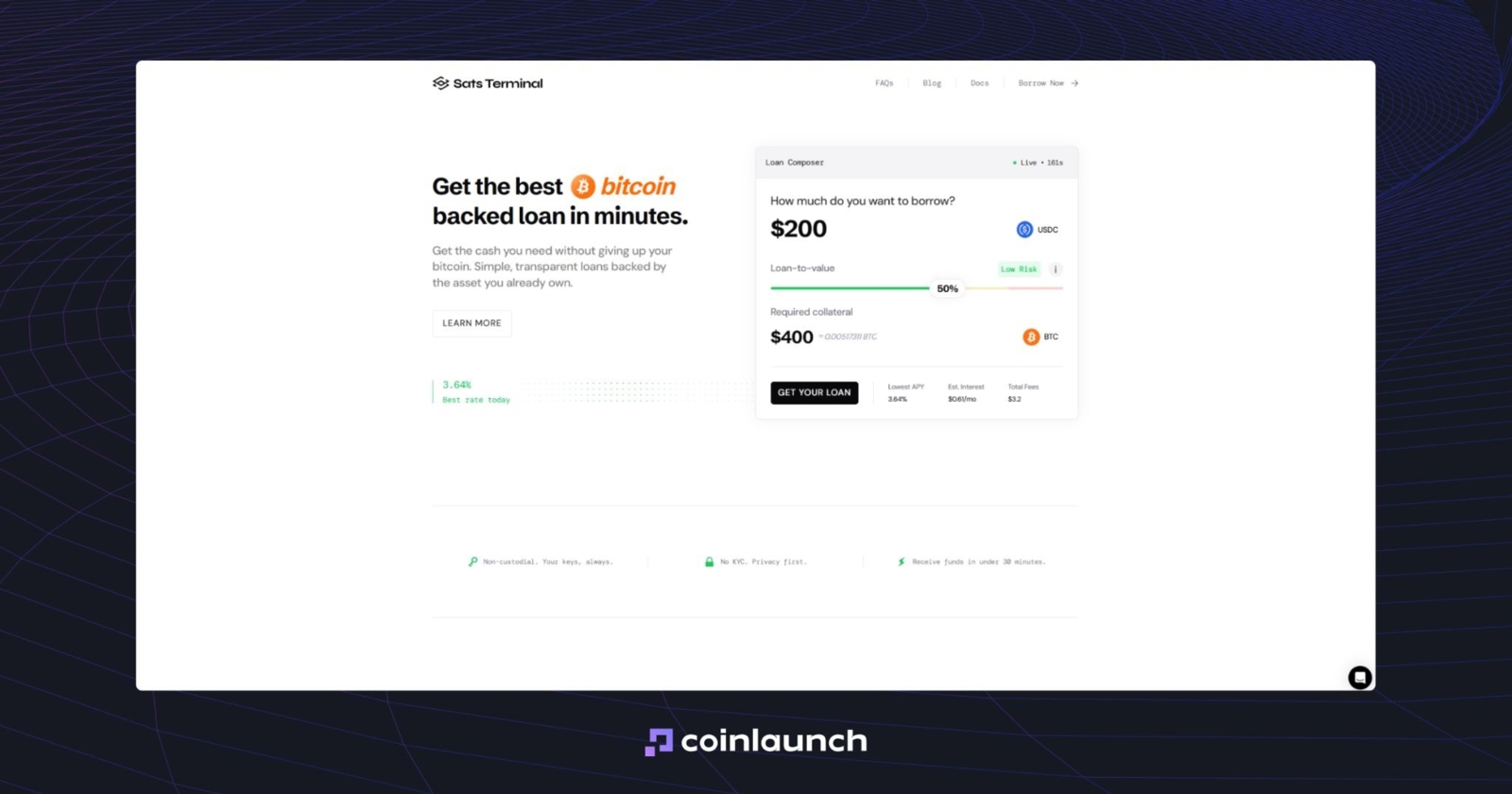

Sats Terminal is a Bitcoin lending platform and aggregator for BTC loans. Instead of manually comparing Aave, Morpho, and other lending markets, users enter the loan amount, select an LTV, and immediately see the key loan terms: interest rate, collateral amount, and liquidation price. The platform supports Bitcoin-USDC loans only.

Sats Terminal homepage. Source: satsterminal.com

Type: DeFi Bitcoin lending aggregator.

Regulation: Sats Terminal operates as a DeFi platform for Bitcoin-backed loans. According to the official website, users retain control over their assets, and KYC is not required. However, Sats Terminal is not a direct Bitcoin lender: it aggregates offers from multiple markets and routes transactions through a verified provider.

Security: Sats Terminal does not hold users’ BTC. Collateral is locked in a smart contract and returned after the loan is repaid. Users can send BTC directly from the native Bitcoin network instead of manually bridging assets or buying wrapped BTC. The platform provides secure infrastructure, BTC collateral management, and transaction tracking for users to move funds across multiple leading Bitcoin lending protocols.

Track Record: In April 2025, Sats Terminal closed a $1.7 million pre-seed round led by Coinbase Ventures and Draper Associates. By the time Borrow launched, the platform had processed over 1.5 million quotes, facilitated 175 BTC in volume through its products, and reached 95,000 users.

Beyond lending, Sats Terminal is developing Bitcoin-native products: Runes Swap, Spark Swap, Runes SDK, and Borrow BTC Loans.

Sats Terminal Bitcoin Lending Terms: Sats Terminal does not have a standard interest rate or fixed LTV — rates and terms depend on the specific offer. Currently, the average Net APY across available options is 3.70%, and the average Max LTV is 71%. Available options include borrowing USDC against BTCB collateral on BNB and Starknet, as well as borrowing USDC against wBTC collateral on Arbitrum.

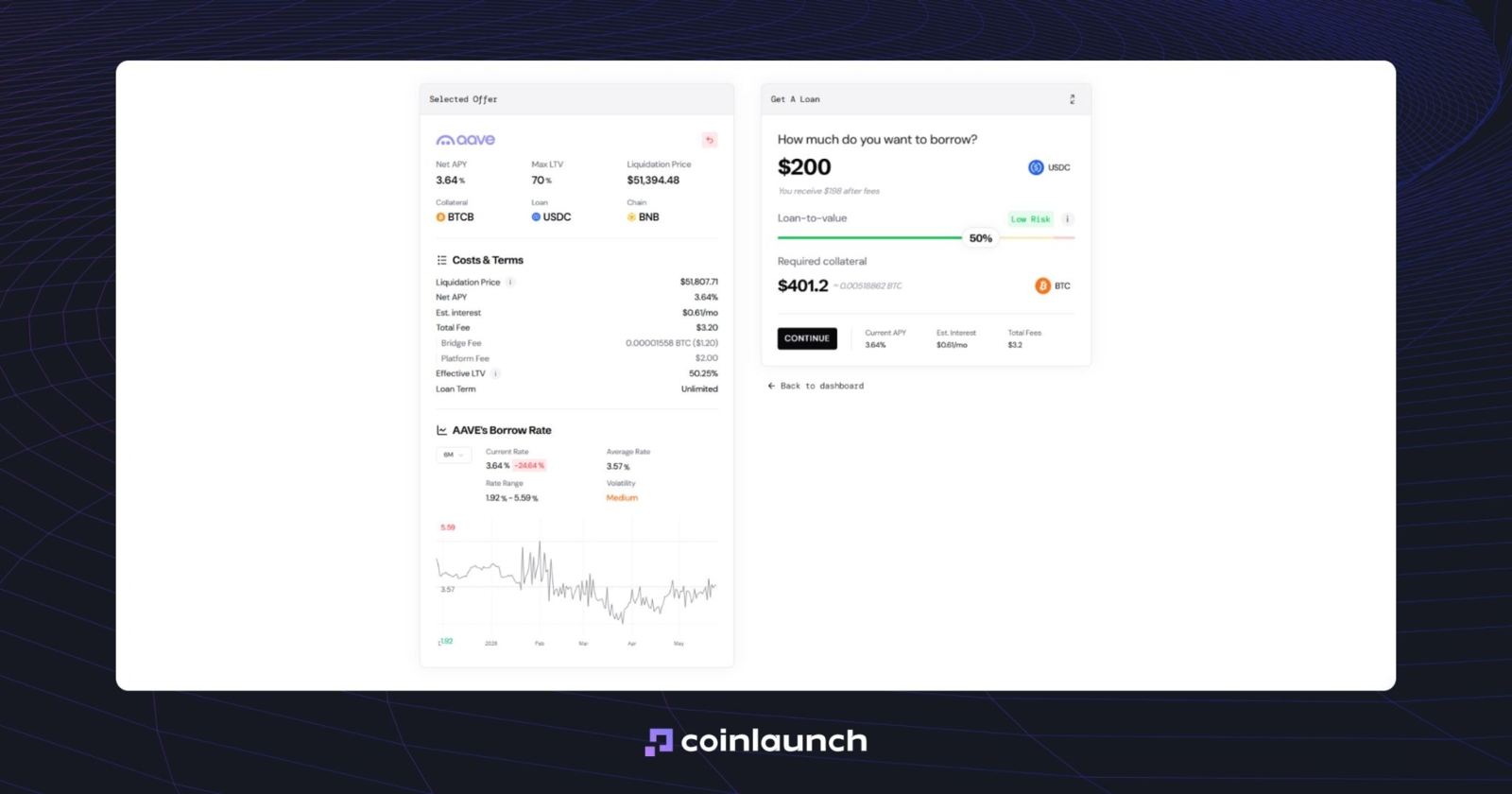

An example of a Sats Terminal position. Source: satsterminal.com

For example, for a $2,000 USDC loan with 50% LTV, Sats Terminal requires $4,000 in collateral. This position is classified as Low Risk.

In the Earn category, the average APY is 1.05%. Available options include the Sats Terminal BTC Yield Strategy, Steakhouse Turbo cbBTC, Moonwell Frontier cbBTC, and Arcadia cbBTC Pool. All four strategies are classified as Safe.

✅ Best for: Users who want to borrow against Bitcoin without manually analyzing protocols or using CeFi platforms. The platform is specifically designed for Bitcoin borrowers because it supports only BTC loans.

Nexo

Nexo is a CeFi Bitcoin lending platform built around its Credit Line product. It lets users borrow against Bitcoin without selling their cryptocurrency. Loan rates start at 1.9% APR, and Nexo offers up to 50% LTV on BTC collateral. Nexo has operated since 2018, and in Q1 2026, it was one of the few companies to grow its AUM, adding $11.18 million, or 0.63% quarter over quarter.

Nexo's homepage. Source: nexo.com

Type: CeFi.

Regulation: According to the website, Nexo operates in more than 199 jurisdictions, including the U.S. The platform announced its return to the U.S. market in April 2025, with a full-scale comeback in February 2026.

Security: Nexo’s partners, Ledger Vault and Fireblocks, power the platform’s security. Ledger Vault stores collateral for Nexo crypto loans, while Fireblocks handles monitoring and management. The company also protects accounts through SMS and email authentication, biometrics, anti-phishing codes, and other security measures.

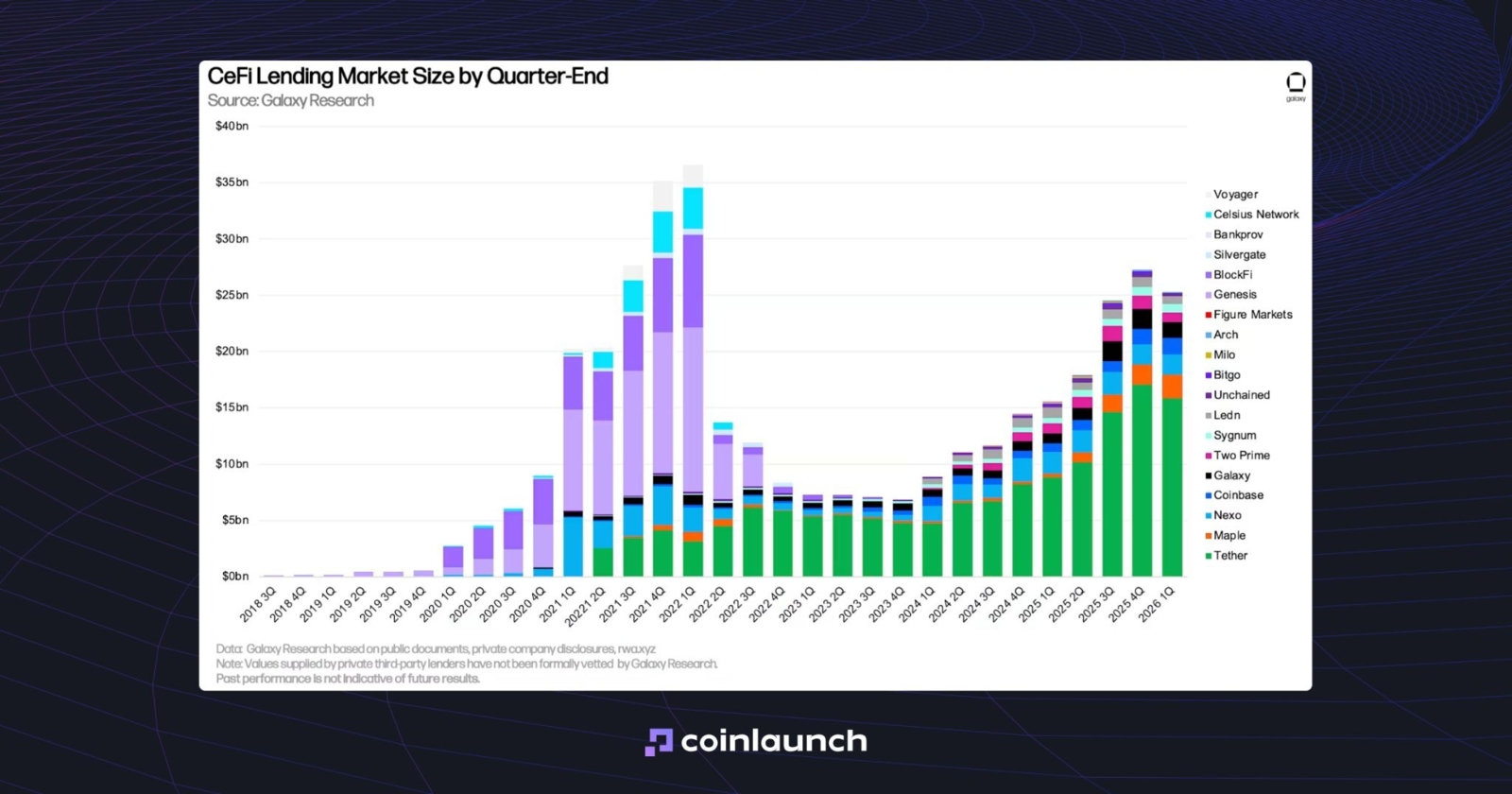

Track Record: According to the platform, Nexo has over $7 billion in assets under management, $430 billion in transaction volume and collateralized credit issued, and $1.4 billion in Nexo interest rate paid. As of Q1 2026, it ranks third among the largest CeFi lending platforms.

CeFi Lending Market Size by Quarter-End. Source: galaxy.com

Nexo Crypto Lending Terms: Users can borrow between $50 and $2 million. The maximum LTV for a Nexo BTC loan is 50%. Users can draw funds on an ongoing basis and repay their debt without fixed dates or minimum payments.

Nexo sends margin call notifications by email at three LTV levels: 71.4%, 74.1%, and 76.9%. At these levels, the platform does not force-close the position. Automatic repayment of the BTC loan is triggered when LTV reaches 83.33%.

✅ Best for: Users who prefer Bitcoin-backed loans in the CeFi segment. It is also an option for large BTC holders: the $2 million borrowing limit suggests that Nexo is geared toward investors with significant capital.

However, Nexo is not just a Bitcoin loans player: in addition to BTC, the platform also supports ETH and stablecoins.

Ledn

Ledn is a CeFi Bitcoin lending platform founded in 2018 by Adam Reeds and Mauricio Di Bartolomeo. The company began operations in Toronto and moved its headquarters to the Cayman Islands in 2023.

Ledn’s core offering is a Bitcoin-backed loan. Users deposit BTC as collateral and borrow in USD, USDC, or another currency. The initial LTV is 50%, and the standard loan term is 12 months. However, the loan can be repaid early.

Ledn's homepage. Source: ledn.io

Type: CeFi.

Regulation: Ledn operates as a CeFi Bitcoin loan app. In February 2026, S&P assigned a BBB- rating to the company’s senior notes. This is the lowest investment-grade rating: the agency classifies such debt as non-speculative under normal market conditions.

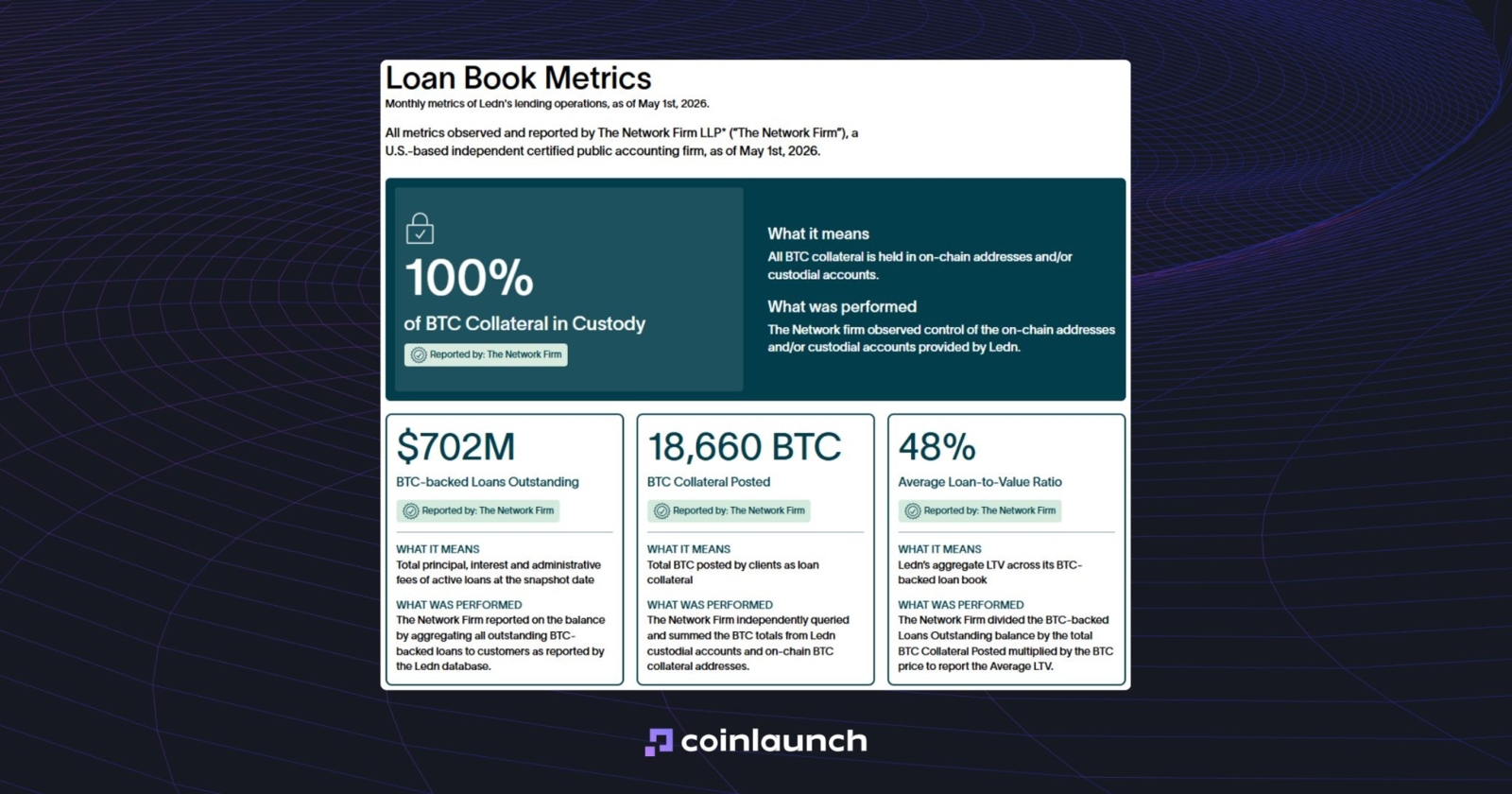

Security: Ledn conducts Proof of Reserves through The Network Firm. The latest audit, dated May 1, 2026, showed that the BTC locked as collateral was 1:1 backed or overcollateralized. This is an important factor when assessing is Ledn safe, but it does not guarantee complete platform security.

Track Record: According to the dashboard on the Ledn official website, the platform has originated $702 million in Bitcoin backed loans, held 18,660 BTC in collateral, and maintained an average lifetime LTV of 48%.

Ledn lending statistics dashboard. Source: ledn.io

Beyond lending, the company offers Trade, DCN, and Growth Accounts for USDC and USDT with yields of up to 8.5% APY.

Ledn Bitcoin Loan Terms: The minimum loan amount is $1,000 in BTC. The initial LTV is 50%. When LTV rises to 70%, Ledn requires additional BTC collateral. At 80%, the platform starts liquidating part of the collateral. Loan rates start at 11.9% APR and drop to 9.99% APR for larger amounts. The base loan term is 12 months, but the loan can be repaid early.

Ledn also offers B2X: the platform issues a dollar-denominated loan and immediately uses it to purchase additional BTC. As a result, the collateral includes both the initial and purchased Bitcoin.

✅ Best for: Ledn is a classic only Bitcoin lender. It works for Bitcoin holders who do not use Ethereum, Solana, or other altcoins, hold only BTC, and want to get BTC loan.

Lava

Lava is a Bitcoin lending platform built around its Bitcoin Line of Credit (BLOC). Users can borrow against Bitcoin holdings to access USD liquidity without selling their BTC. According to Lava, the credit line has no fixed term and no mandatory monthly payments: interest is added to the balance, and the BTC loan can be repaid in full or in part at any time.

Lava Bitcoin loans are typically processed in less than 5 seconds, with an average processing time of about 400ms.

https://x.com/lava_xyz/status/1983228392238383330

Type: CeFi

Regulation: Lava emphasizes data protection and does not collect unnecessary information. The company’s website does not disclose its regulatory status. But here’s the con: Lava requires users to complete KYC verification through Persona.

Security: The company describes a model based on asset self-custody, on-chain reserves, and no rehypothecation. BTC is stored in separate Lava wallets, with keys distributed among multiple participants.

Track Record: The Lava website lists Founders Fund, Susquehanna, and Khosla Ventures as investors. Total funding raised: $227 million. Beyond BLOC, the platform offers the Lava Card, commission-free BTC buying and selling, a dollar-denominated interest-bearing account, and bank withdrawals.

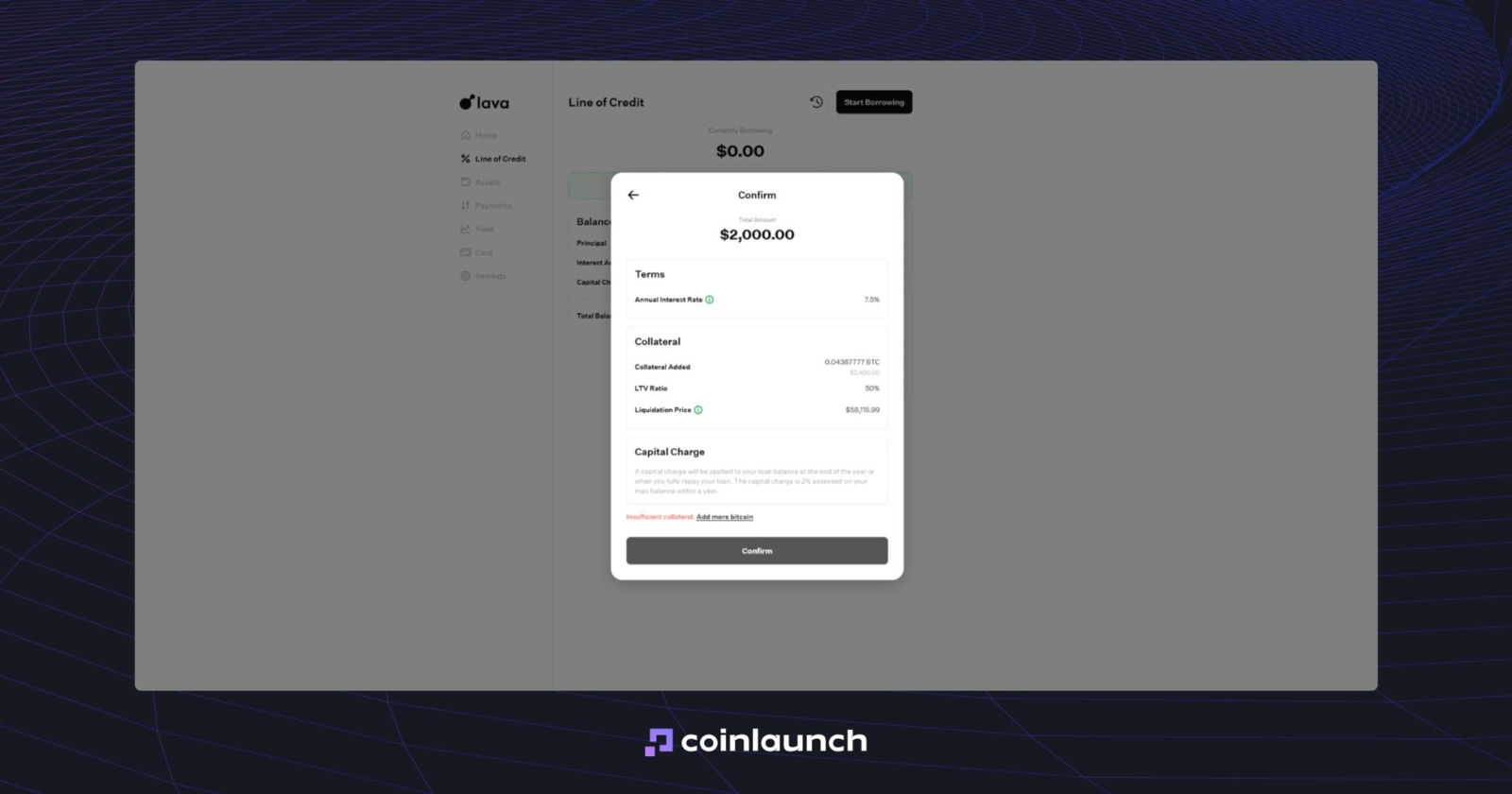

Lava Bitcoin Lending Terms: Users can loan BTC in amounts ranging from $100 to $1 billion+. The interest rate depends on the total credit line balance: 7.5% for balances under $100,000 and 6.5% for balances of $100,000 or more. It is fixed for one year. The maximum LTV for opening a loan is up to 60%. If LTV exceeds 80%, the system automatically adds BTC from the user’s available balance.

The Bitcoin borrowing page on the Lava Bitcoin lending platform. Source: lava.xyz

Lava charges an annual capital fee equal to 2% of the highest outstanding balance for the year. For example, if the peak debt was $5,000, the fee would be $100, even if the user later reduced the balance to zero.

✅ Best for: Lava is less like a Bitcoin loan app and more like an online crypto banking platform. It works best for users who want Bitcoin borrowing, interest-bearing accounts, a debit card, commission-free BTC purchases, and bank withdrawals in one place.

Debifi

Debifi is a non-custodial Bitcoin lending platform. Users can get BTC loan without transferring collateral to the platform for safekeeping: BTC is locked in a multi-signature escrow account, and the borrower receives funds in fiat currency or stablecoins. The loan is issued by a third-party institutional lender, not Debifi. The platform therefore, works more like a marketplace than a standalone Bitcoin loan app.

Debifi’s slogan and design. Source: debifi.com

Type: Non-custodial Bitcoin lending marketplace.

Regulation: Debifi does not operate like a traditional CeFi platform. Loan offers come from third-party Bitcoin lenders that complete verification and sign a separate agreement with the platform. Borrower KYC is not mandatory, although individual Bitcoin lenders may still require it.

Debifi does not have access to user data: borrowers share it directly with the lender. The KYC status for each loan is displayed in advance, allowing users to immediately see which offers fit their requirements.

Security: Debifi uses a 3-of-4 multisignature escrow model. Access to collateral requires three out of four signatures, meaning no single participant can withdraw the BTC independently. For comparison, Bitcoin Card uses a 2-of-3 setup.

Once the loan agreement is signed, the platform assigns a separate escrow address to the position. Collateral remains locked there until repayment or liquidation. Debifi states that collateral is never reused and that users receive automatic notifications when LTV rises. Liquidation is triggered once the lender’s threshold is reached.

Track Record: Debifi exited beta in June 2025. During the 12-month testing period, third-party institutional Bitcoin lenders issued more than $20 million in loans through the platform. The lender network expanded from two participants to more than 30 organizations, including Berglinde and STOKR.

In January 2026, the average LTV on the platform was 60%, APR ranged from 8.5% to 20%, the average BTC loan size was $60,000, and loan terms ranged from 1 to 24 months.

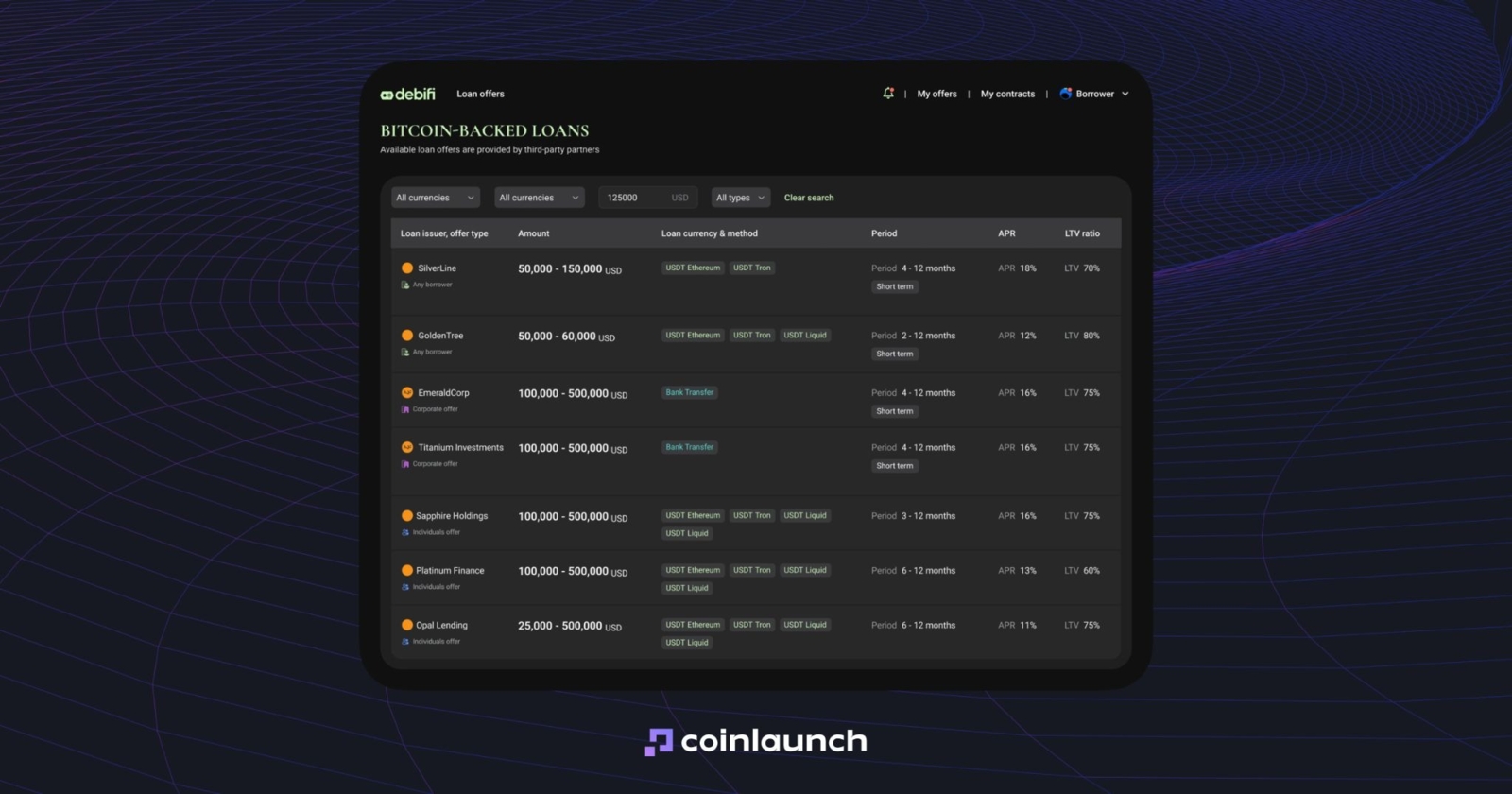

A representative list of Bitcoin lenders on Debifi. Source: debifi.com

Debifi Bitcoin Lending Platform Loan Terms: Terms vary by loan offer. The offers page shows the lender, offer type, amount, currency, repayment method, term, APR, LTV, and verification status.

Debifi charges borrowers a loan origination fee. The base fee depends on the loan amount: 1.5% for loans up to $300,000, 1.2% for $300,001 to $1 million, and 1.0% for loans over $1 million. A term-based fee also applies: 0% for the first year, 0.3% for the second, and 0.6% for the third.

✅ Best for: Users who want to borrow against Bitcoin and compare different non-custodial lenders.

Fuji Money

Fuji Money, or Fuji Finance, is a non-custodial Bitcoin lending protocol on Liquid. Users lock L-BTC in a smart contract and borrow fUSD or other assets available on the platform. Fuji does not custody the collateral itself: BTC remains in the contract, and the borrower unlocks it after repaying the debt.

Fuji Money's homepage. Source: fuji.money

Type: DeFi Bitcoin lending protocol on Liquid Network.

Regulation: The official website does not provide information about platform licenses or regulatory status.

Security: Collateral is locked in a Liquid smart contract. Fuji uses an oracle to track the price. If the collateral value falls below the minimum requirement, a liquidator can claim the collateral by burning the Fuji asset and submitting a signed oracle message.

Track Record: Official sources do not provide data on loan volume, TVL, user count, or locked L-BTC.

Fuji Money Bitcoin Loans Terms: The smart contract mints 1 fUSD for every $1.1 in BTC locked as collateral. To reclaim BTC, the borrower burns the same amount of Fuji assets minted against that collateral.

✅ Best for: Users who want to borrow synthetic assets against L-BTC inside Liquid.

Conclusion: What Is the Best Bitcoin Lending Platform?

When it comes to choosing the best Bitcoin lending platform for you, there is no simple answer to that question. Whether you hunt only Net APY gain or are worried about custodial crypto platforms, it all depends on which you value the most.

CeFi platforms like Nexo and Ledn work for users who want a Bitcoin loan with support and custodial storage. Or DeFi platforms with no KYC requirements and non-custodial lending. That’s on you to choose. Meanwhile, some of the platforms may offer only borrowing or lending BTC, not both.

If you are new to borrowing against Bitcoin, Sats Terminal is the best starting point. The platform supports both Bitcoin lending and borrowing by aggregating the best offers from verified providers in a simplified, user-friendly interface.

Users can view loan terms in a single interface: interest rate, LTV, collateral amount, and liquidation price to find the best loan terms for their BTC within a few clicks. By aggregating multiple lending markets, it also delivers one of the biggest Net APYs and LTV ratios in DeFi lending with the ability to switch between lending strategies pre-sets to get “Highest APY” or “Lowest Risk” options.

Was this article helpful?

Share this blog post

Research

Jason Shaw

August 6, 2026

15 min

The Best Crypto Marketing Agency for 2026: Our Insider's Shortlist backed by Real Reviews and Case Studies

Research

Jason Shaw

August 5, 2026

14 min

Best Solana DEX List: How to Choose the Best DEX on Solana

Research

Daniel Bennett

August 4, 2026

21 min

9 Top Web3 Branding Agencies of 2026: Crypto & Blockchain Design Studios, Judged on Shipped Work

No Comments

No comments yet