Table of contents

- What is a Crypto Lending Platform

- Why Do You Need Crypto Lending Platforms?

- How to Find the Best Crypto Lending Platforms

- Best Crypto Lending Platforms: Comparative Table

- Sats Terminal

- Nexo

- Ledn

- Arch

- Aave

- Morpho Protocol

- Compound Finance

- Kamino Finance

- Final Verdict on the Best Crypto Lending Platforms

Table of contents

- What is a Crypto Lending Platform

- Why Do You Need Crypto Lending Platforms?

- How to Find the Best Crypto Lending Platforms

- Best Crypto Lending Platforms: Comparative Table

- Sats Terminal

- Nexo

- Ledn

- Arch

- Aave

- Morpho Protocol

- Compound Finance

- Kamino Finance

- Final Verdict on the Best Crypto Lending Platforms

By the end of Q1 2026, Galaxy Research valued the crypto lending market at $67.42 billion. The market is getting crowded, and choosing the right platform is becoming harder with every new launch.

The crypto lending ecosystem includes CeFi platforms that offer custodial storage and support, DeFi lending protocols with smart contracts and automatic liquidations, aggregators, and tools for managing loans and strategies. Platforms range from user-friendly CeFi services to DeFi protocols that prioritize asset control and aggregators that simplify term comparison.

This guide breaks down how crypto lending platforms work, why investors use crypto-backed borrowing, what criteria to use when choosing the best crypto loan platforms, and which services lead the market.

What is a Crypto Lending Platform

A crypto lending platform is an entity that lets users borrow against assets including BTC, ETH, and XRP. The mechanics mirror traditional bank loans, but instead of a bank, the borrower uses either a CeFi or DeFi lending platform. CeFi relies on centralized custodians to hold user funds, while DeFi uses decentralized protocols where funds are not held by a third party.

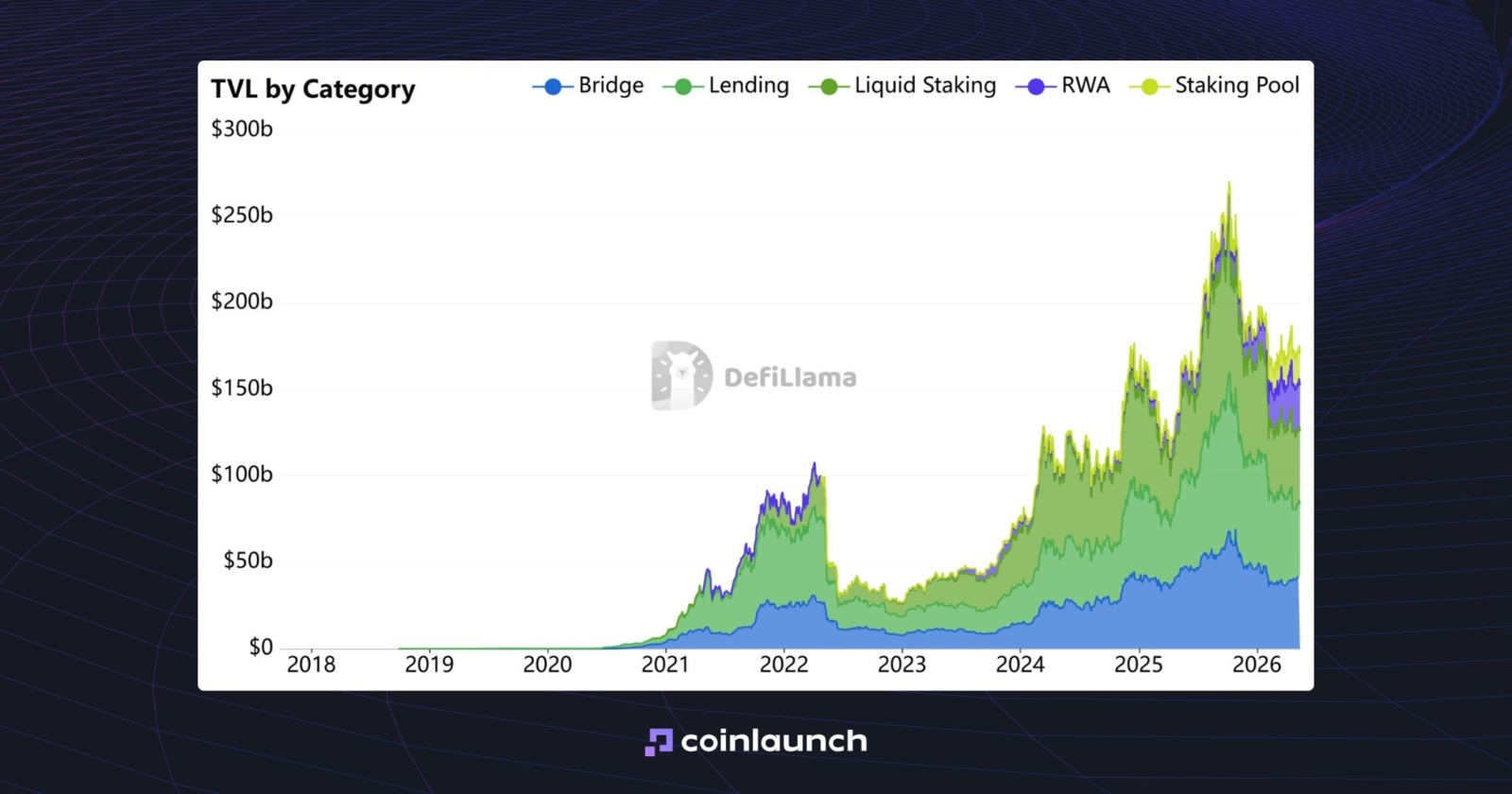

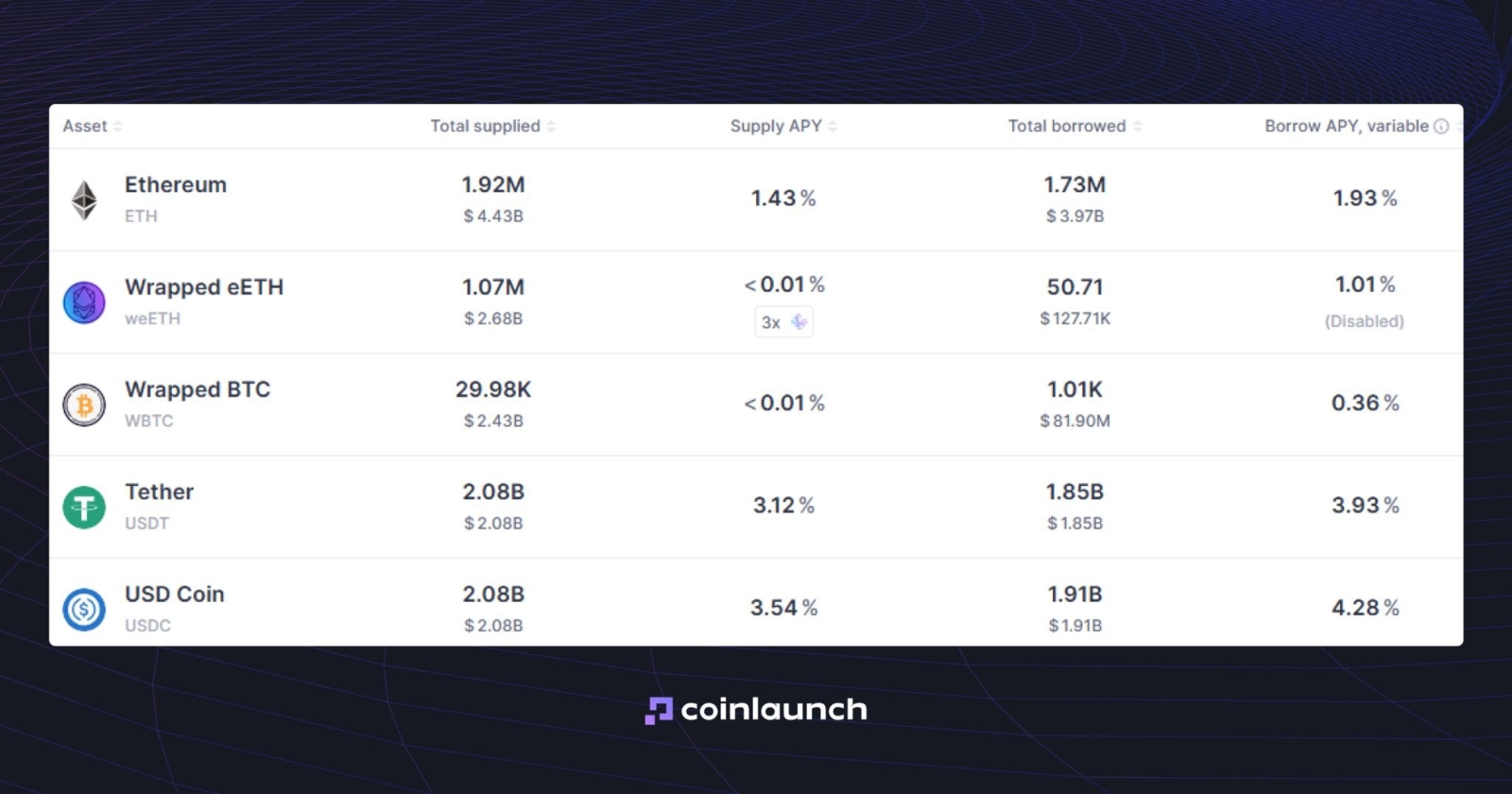

Crypto loan platforms, and crypto lending as a whole is currently the dominant DeFi category by Total Value Locked (TVL). At $42.6 billion, it narrowly leads Liquid Staking ($41.7 billion) and Bridges ($41.6 billion).

TVL by top five categories: Lending, Liquid Staking, Bridge, RWA, and Staking Pool. Source: defillama.com

Crypto lending platforms help investors access additional liquidity when they need it. Rather than sell their assets, they borrow against their crypto and keep their positions intact.

Why Do You Need Crypto Lending Platforms?

The main advantage of crypto lending platforms is access to funds without selling your crypto assets. Investors often seek liquidity for short-term needs without wanting to exit their long-term positions. Selling BTC, ETH, or another asset means forfeiting potential upside if the cryptocurrency’s market value rises.

The borrowed funds can be used for other investment goals: participating in upcoming token sales, CEX promotional campaigns, staking, restaking, short-term market plays, and other strategies. For entrepreneurs, such a loan can also serve as a source of working capital: the cryptocurrency remains as collateral, while the funds are used to cover business expenses.

DeFi protocols also use crypto lending, for example in the Yield Farming category, to diversify the range of investment strategies offered. For instance, “The GOAT crypto lending platform” might allow users to borrow against BTC, receive stablecoins, use them for farming, and then use the resulting yield to cover interest payments.

How to Find the Best Crypto Lending Platforms

Choosing the right lending platform requires a focus on several key areas: media visibility, security, TVL, and interest rates. Determine which criteria matter to you, then start your research from there.

- Media visibility. This is the least effective way to choose a crypto lending platform: popularity on social media is often manufactured and rarely guarantees quality. Even if a hundred KOLs say the project is good, it means nothing. Their opinion may be biased.

- Security. To find the safest crypto lending platform, look at its reputation: how long it has been on the market, whether it has suffered any security breaches, and how well the protocol is protected. If it is a CeFi platform, check when the last Proof of Reserve report was issued and whether it covers 100% of the assets in the accounts.

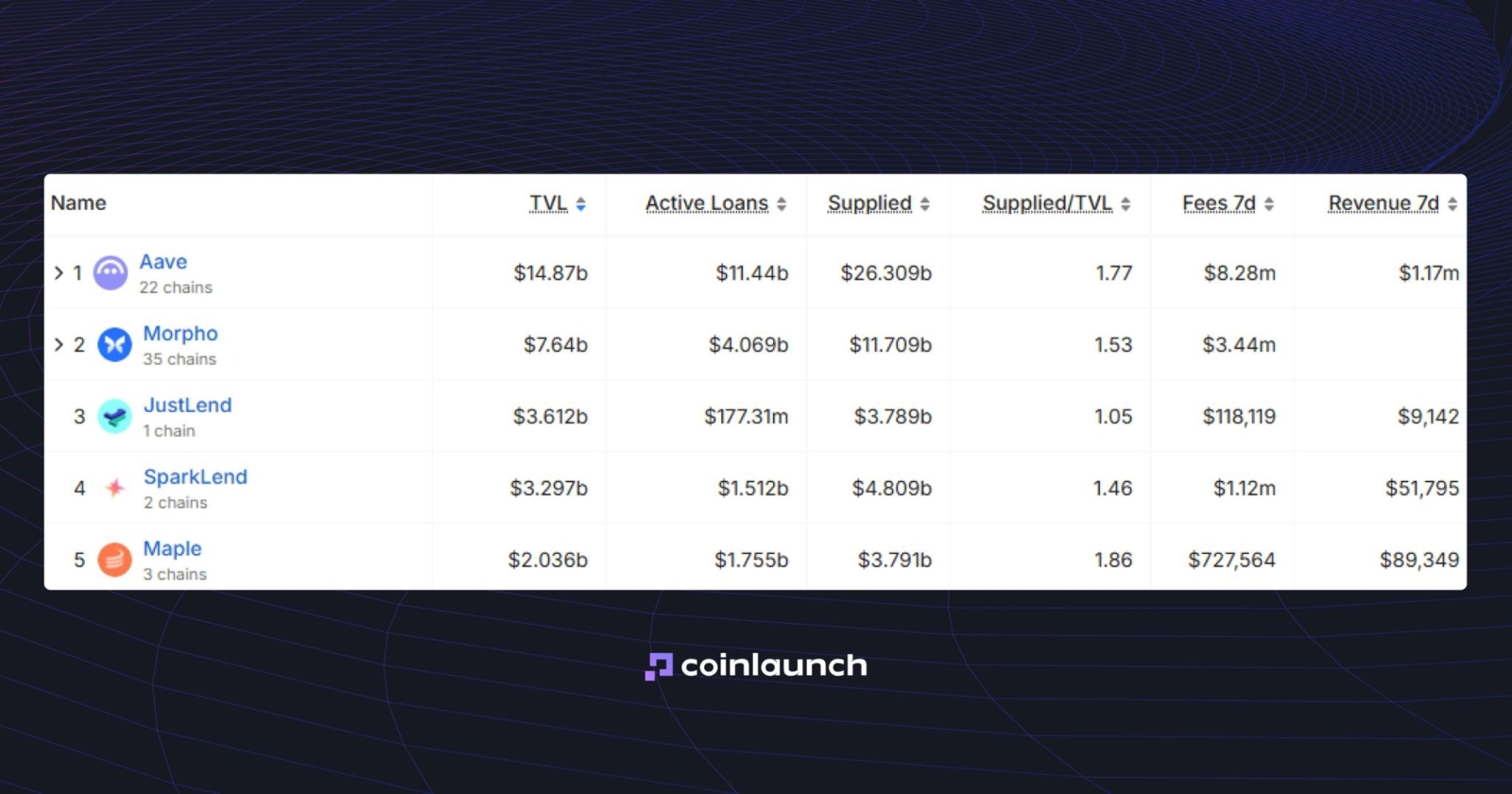

- TVL. This reflects the platform’s liquidity and adoption. On services like DefiLlama, you can view crypto lending platform rankings by TVL.

Top 5 crypto lending platforms by TVL. Source: defillama.com

- Interest rates. More than a hundred lending protocols compete on the market, and manually reviewing the terms for each one is highly inefficient. To streamline the process, use specialized aggregators like Sats Terminal: the platform analyzes data from multiple protocols and displays lending information in a single interface.

Best Crypto Lending Platforms: Comparative Table

Platform | Supported chains | LTV threshold | Borrow APR | Lend APY | Security | Requires KYC | Best for |

Sats Terminal | 6 | Avg max LTV: 69.8% | Avg borrow: 5.97% Net APY | Avg lend: 5.42% APY | Non-custodial; Audited by CertiK | No | BTC loan and USDC yield aggregation |

Nexo | 24 | 83.33% | 1.90% | USDC up to 9.5%; BTC up to 5.7% | Custodial; | Yes | Large crypto-backed loans |

Ledn | Bitcoin-only | 70% margin call; 80% liquidation | 10.74% avg | Up to 8.5% | Custodial; | Yes | Bitcoin-only loans |

Arch | 4 | 70% warning; 80% margin call; 90% liquidation | 9.37% avg | 11.50% | Qualified custody via Anchorage; | Yes | BTC/ETH/SOL/XRP loans |

Aave | 13 | Asset-based | From 1% to 12% | 6.50% | Non-custodial; Audited by Sherlock, OpenZeppelin, etc. | No | DeFi lending |

Morpho | Ethereum, Base + other deployments | 87.90% | 3.65% | 4.89% | Non-custodial; Audited by ChainSecurity, OpenZeppelin, etc. | No | Custom lending markets |

Compound | EVM chains | 84.20% | Variable | Variable | Non-custodial; Audited by OpenZeppelin, ChainSecurity, etc. | No | Established DeFi lending |

Kamino Finance | Solana | 76.56% | 4.22% | 3.92% | Non-custodial; 20 external security reviews | No | Solana lending |

Sats Terminal

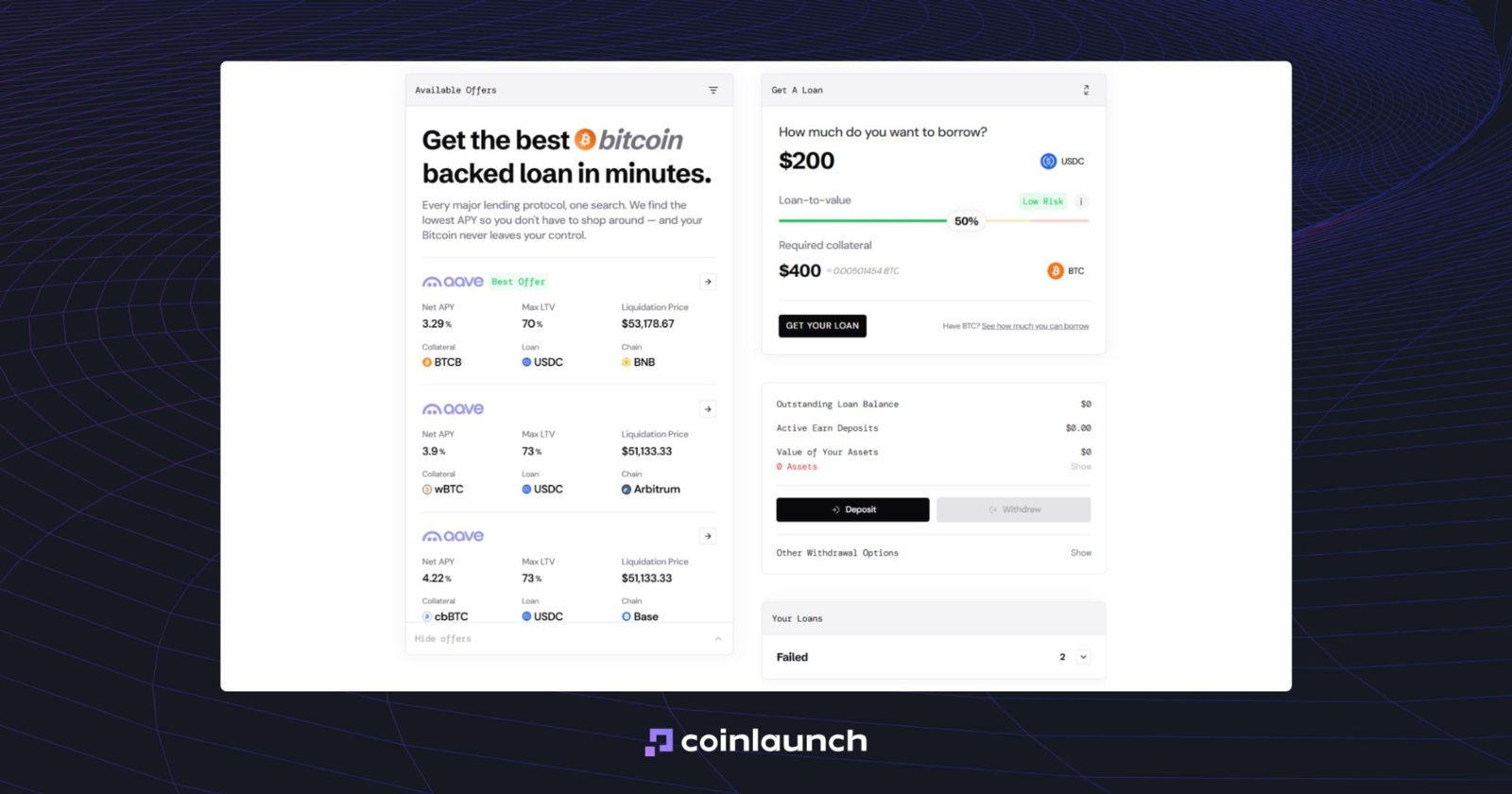

Sats Terminal is a Bitcoin lending aggregator. In a single app, users can access positions from Aave, Morpho, Kamino, Ledn, and Arch, compare loan terms, and select a suitable BTC-backed position. By consolidating rates, LTVs, collateral amounts, and liquidation thresholds into a single view, Sats Terminal eliminates the need to search for and analyze each DeFi lending protocol manually.

The platform helps users set up a BTC-backed loan, calculate the required collateral, and finalize the loan through their chosen platform. Users do not need to bridge assets or purchase WBTC separately: they simply send BTC through the native Bitcoin network, while Sats Terminal handles the routing and delivers USDC to an EVM network.

Sats Terminal interface. Source: satsterminal.com

Sats Terminal interface. Source: satsterminal.com

In addition to lending, Sats Terminal is developing other Bitcoin-native products: Runes Swap for token swaps, Spark Swap for Spark-based swaps, and the Runes SDK for developers.

The platform has approximately 95,000 users and has processed 175 BTC to date. The project is backed by YZi Labs, Coinbase Ventures, MH Ventures, and Draper Associates, which invested $1.7 million in it.

Nexo

As of May 2026, Nexo serves over 7 million customers. Since 2018, transaction and secured loan volume on the platform has exceeded $403 billion. One of the most notable cases in its history is the $1.2 million Nexo crypto loan issued to Brock Pierce for the purchase of a home in Amsterdam.

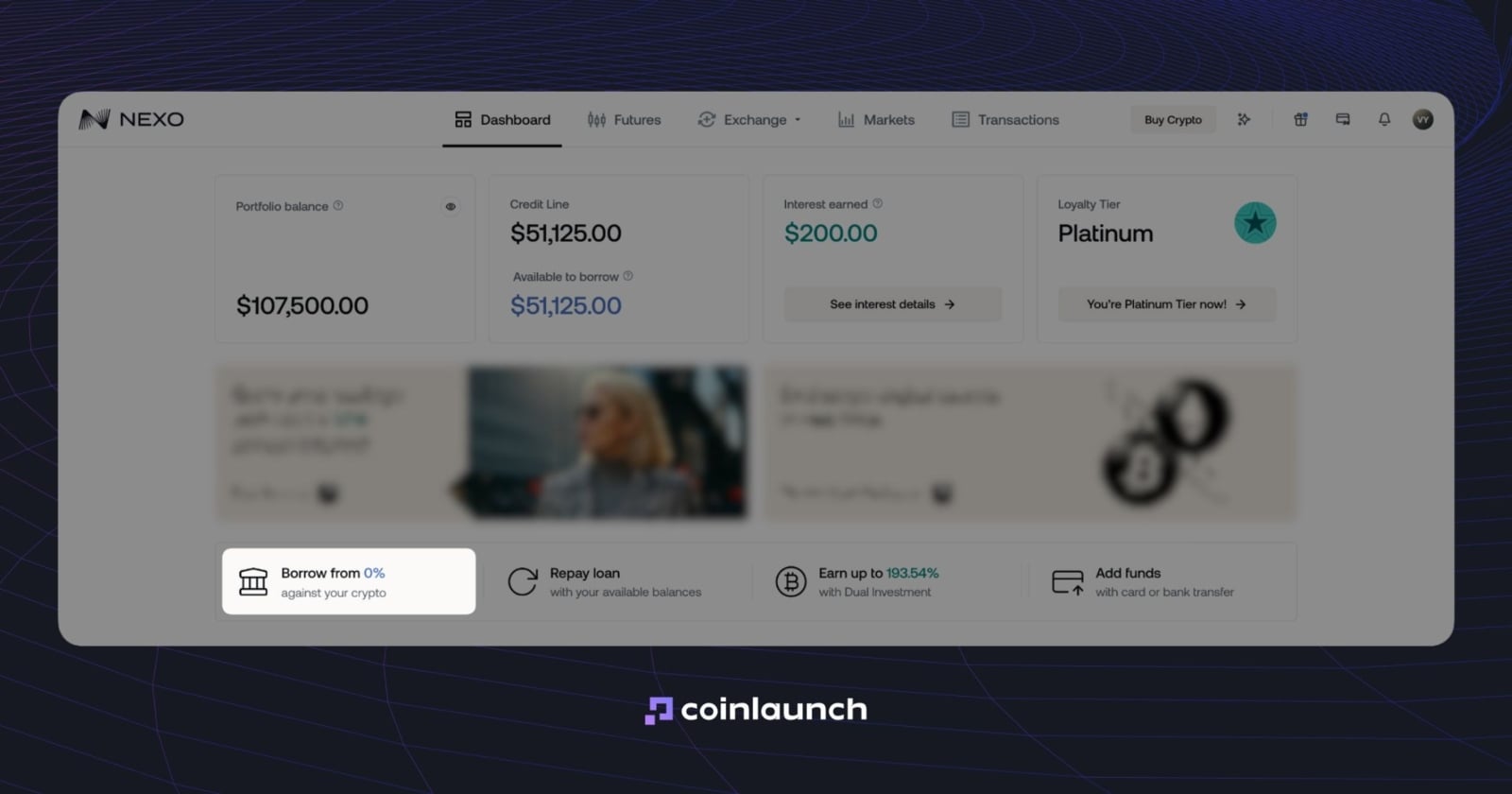

Nexo is a CeFi platform that lets users access liquidity without selling their crypto assets. Users pledge cryptocurrency as collateral and receive funds in stablecoins or fiat. The service is not limited to lending: the platform also offers exchange, spot trading, and futures, and supports over 100 assets.

Nexo crypto loans are offered through a product called “Credit Line.” The platform automatically calculates the available credit line, while Nexo Oracle manages the terms. Rates for the standard Credit Line start at 1.9% per year, and a 0% rate is available through a separate product called Zero-interest Credit.

The “Zero-interest Credit” option on the Nexo website. Source: nexo.com

The “Zero-interest Credit” option on the Nexo website. Source: nexo.com

LTV depends on the asset: 50% for BTC and ETH, 15% for NEXO, and up to 90% for stablecoins.

The platform also offers returns on cryptocurrency deposits: Nexo interest rates reach 13% per year in Flexible Savings and 15% in Fixed-term Savings. NEXO token holders can access a Loyalty Program that reduces loan rates based on the share of NEXO in the user’s total funds.

After exiting the U.S. market in 2022, Nexo announced its return in April 2025 and relaunched its flagship products there in February 2026. The platform currently operates in more than 199 jurisdictions.

Ledn

Before discussing what Ledn is, it is worth noting that it is a CeFi platform. The project was launched in 2018 by Adam Reeds and Mauricio Di Bartolomeo. The company was originally based in Toronto but moved its headquarters to the Cayman Islands in 2023.

Ledn’s main product is bitcoin-backed loans: users pledge Bitcoin as collateral and receive a loan in USD, USDC, or another currency. The standard loan term is 12 months, but it can be repaid early. The minimum loan amount is $1,000 in BTC, and the starting LTV is 50%. If the LTV rises to 70%, the platform requests additional collateral; at 80%, it liquidates part of the collateral.

Interest rates on these loans start at 11.9% APR and drop to 9.99% APR for larger amounts. Ledn also offers the B2X product: the platform issues a dollar-denominated loan that is immediately used to purchase additional Bitcoin, so both the initial and newly purchased BTC serve as collateral, which is namely looping creating a leverage on your position.

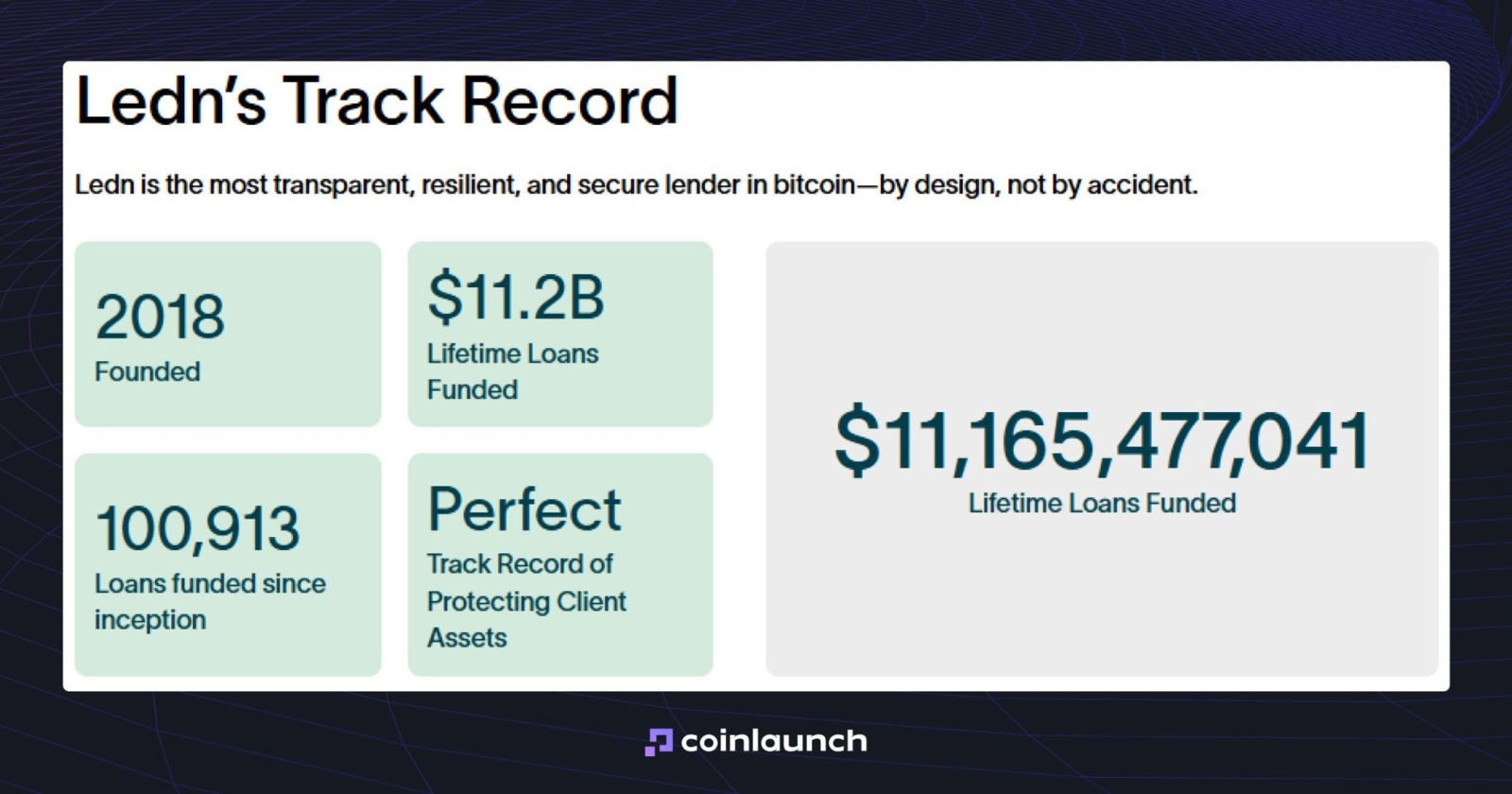

According to the platform, Ledn has $702 million in bitcoin-backed loans, 18,660 BTC in collateral, and an average lifetime LTV of 48%. This data is available on the dashboard on the Ledn official website.

Ledn statistics. Source: ledn.io

Ledn statistics. Source: ledn.io

S&P assigned a BBB- rating to Ledn’s senior notes in February 2026, the lowest investment-grade rating. In practice, this means the agency considers the debt non-speculative under normal market conditions.

Beyond lending, Ledn offers Trade, DCN, and Growth Accounts for USDC and USDT with yields of up to 8.5% APY. The company also publishes Proof-of-Reserves audits through The Network Firm. The latest report, dated September 30, 2025, showed reserves matching or exceeding 100% of the Bitcoin locked as collateral.

We also tried testing Ledn interest rates for different assets and loan amounts through its Bitcoin loan calculator, but the tool returned a 403 error after clicking “Apply now.” Most likely, accurate loan terms become available only after completing KYC and opening a loan request.

Arch

Arch Lending, founded in 2022, specializes in crypto-backed loans. The company operates in most countries and 44 U.S. states. In August 2024, the project raised $70 million from Galaxy and $5 million from other investors.

Arch lets users borrow in U.S. dollars or USDC against crypto collateral. As a CeFi platform, it requires identity verification, while Anchorage Digital, a federally chartered U.S. crypto custodian, holds the collateral. Arch Crypto accepts four collateral assets: BTC, ETH, SOL, and XRP.

For BTC, the initial LTV is 60%, with the first margin call at 70% and partial liquidation at 80%. For ETH, the thresholds are 55%, 65%, and 75%; for SOL and XRP, they are 45%, 55%, and 65%, respectively. Loan terms range from one to 12 months. Clients can extend the loan or repay it early. The website also includes a loan calculator that lets users estimate Arch Lending interest rates in advance.

Crypto Loan Calculator. Source: archlending.com

Arch charges a 1.49% origination fee when users apply for a loan, and partial repayments carry a 2% fee. Interest rates on Arch loan start at 7.25% per year under the updated terms adopted in May 2026, down from 8.49%.

According to the company, the platform has serviced over $500 million in loans and worked with more than 1,000 borrowers.

Arch also offers two additional products. Perpetual Income lets users receive regular payments backed by BTC: the client deposits at least 1 BTC, while the platform automatically renews the loan and manages the strategy. TaxShield is a solution for U.S. clients that uses BTC collateral to purchase mining equipment through Blockware and reduce tax liability.

Aave

The Aave lending protocol is the largest platform. It was originally launched as ETHLend: under this name, Stani Kulechov launched the project in 2017 and raised $16.2 million through an ICO for the LEND token. The team later rebranded to Aave, which means “ghost” in Finnish.

The protocol relies on liquidity pools. Some users deposit assets into these pools and act as lenders, while others borrow from them. Aave uses an overcollateralized model: to borrow funds, users must first deposit collateral worth more than the loan amount. Aave’s borrowing rates are not fixed and depend on pool utilization: the higher the demand for loans, the higher the rate.

Aave interest rate by total supplied. Source: aave.com

Initially, Aave operated exclusively on Ethereum, but over time it expanded to other networks, including Avalanche, Polygon, Optimism, Arbitrum, and Base.

Aave became the first platform to launch crypto flash loans: the mechanism was introduced in Aave V1 in 2020. An Aave flash loan is an unsecured loan that must be taken out and repaid within a single transaction, or approximately 12 seconds. Otherwise, the transaction is canceled. The Aave flash loan fee is 0.05%.

Flash loans provide instant liquidity for short-term trades executed within a single transaction: for example, buying low on one exchange, selling high on another, and repaying the loan within the same transaction.

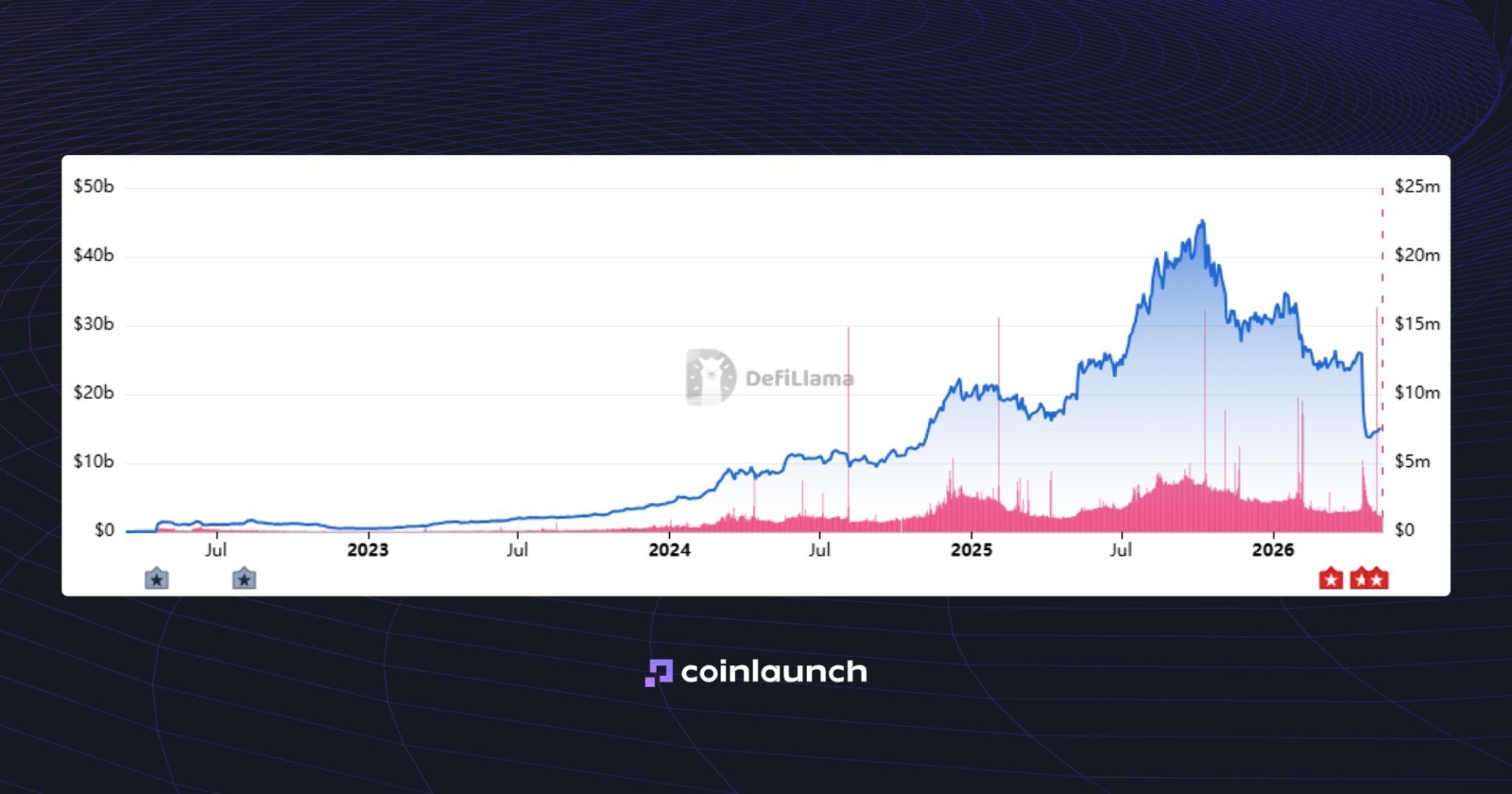

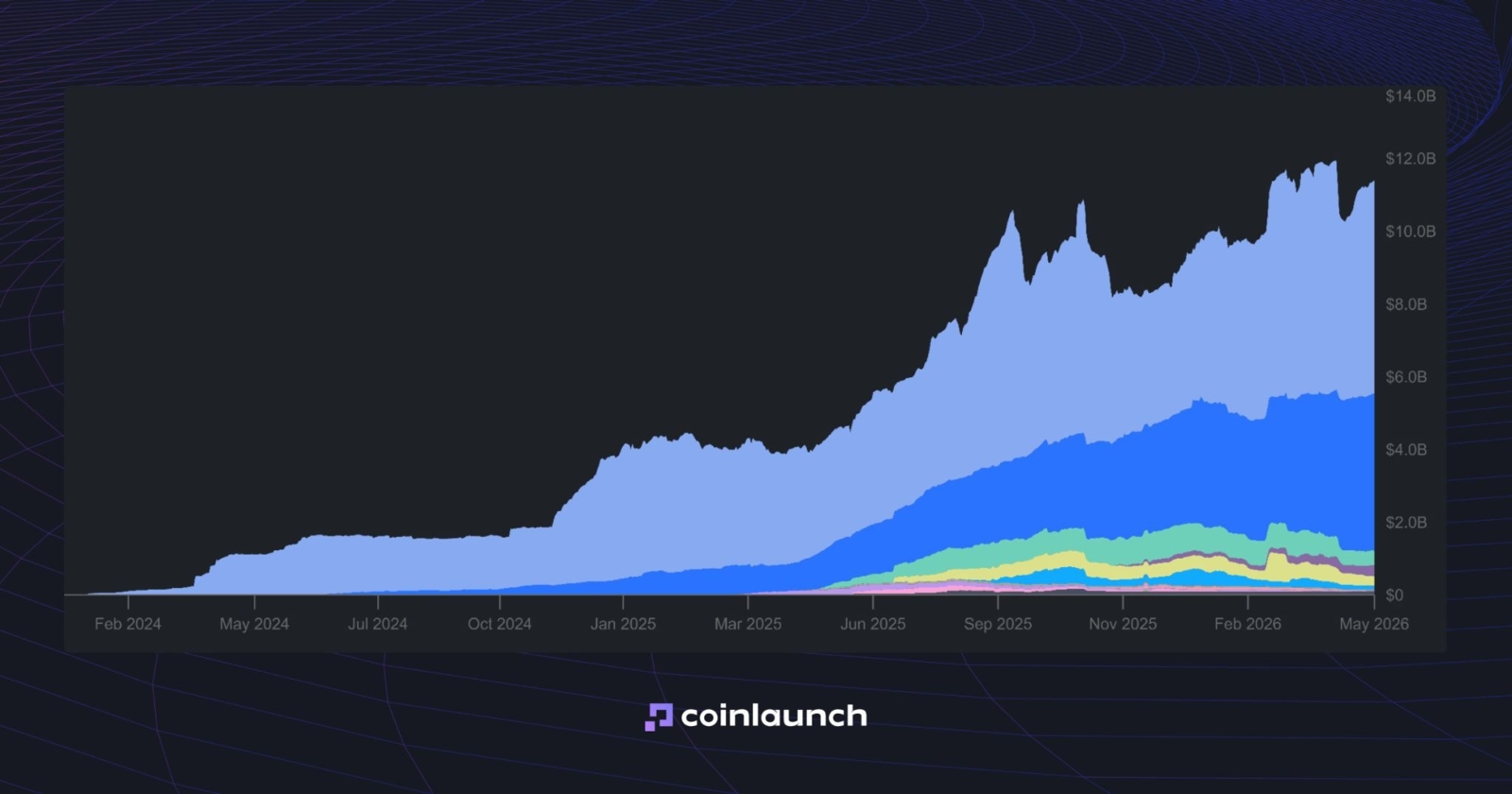

Currently, most liquidity is concentrated in Aave V3. TVL for this version is approximately $14.8 billion, while Aave V4 has around $37.4 million. V3 uses separate markets with their own liquidity pools, while V4 uses a Hub & Spoke model, where liquidity is concentrated in a central hub.

Aave V3 TVL Trend Chart. Source: defillama.com

Aave V3 TVL Trend Chart. Source: defillama.com

The Aave DeFi lending protocol is the largest by total value locked (TVL). Its TVL is nearly double that of Morpho, which ranks second. Aave remains the clear market leader by popularity.

The average yield is around 1.16%, but deposit and loan rates vary by asset and demand. The Aave ecosystem also offers staking through the Safety Module and Umbrella, as well as swaps routed through ParaSwap or CoW Protocol, depending on the network.

Morpho Protocol

The Morpho DeFi lending protocol supports Ethereum, Base, Polygon, Unichain, and several other networks. The project launched in June 2022 and has raised approximately $70 million to date: $19 million in 2021–2022 and another $50 million in 2024. Morpho’s investors include Ribbit Capital, a16z crypto, Coinbase Ventures, Variant, and Pantera Capital.

Morpho’s lending model can be confusing because its architecture evolved in several stages.

The early product, Morpho Optimizers, operated as a layer on top of Aave and Compound: the protocol matched lenders and borrowers in a P2P format. If a match was found, a position was opened; if not, liquidity was placed in the underlying Aave or Compound pool. This model now belongs to the previous version, Morpho V0.

Morpho’s main product today is Morpho Blue. It is a permissionless and immutable protocol where any user can create isolated lending markets. Unlike Optimizers, liquidity sits inside Morpho rather than Aave or Compound.

According to Morpho’s own data, by May 2026, total deposits in the protocol had reached approximately $11.4 billion, active loan volume stood at $3.79 billion, and TVL was $7.61 billion. Most of the volume remains concentrated on Ethereum and Base.

Morpho Deposits & Loans Chart. Source: morpho.org

To assess whether Morpho lending is safe, it is worth looking at past security incidents. Morpho has had only a few, and none resulted in user funds being lost.

On April 10, 2025, Morpho experienced an incident caused by an incorrect configuration during the transition from Bundler2 to Bundler3. Whitehat c0ffeebabe.eth intercepted the transaction and later returned the funds. According to Morpho’s official statement, no users were affected.

Compound Finance

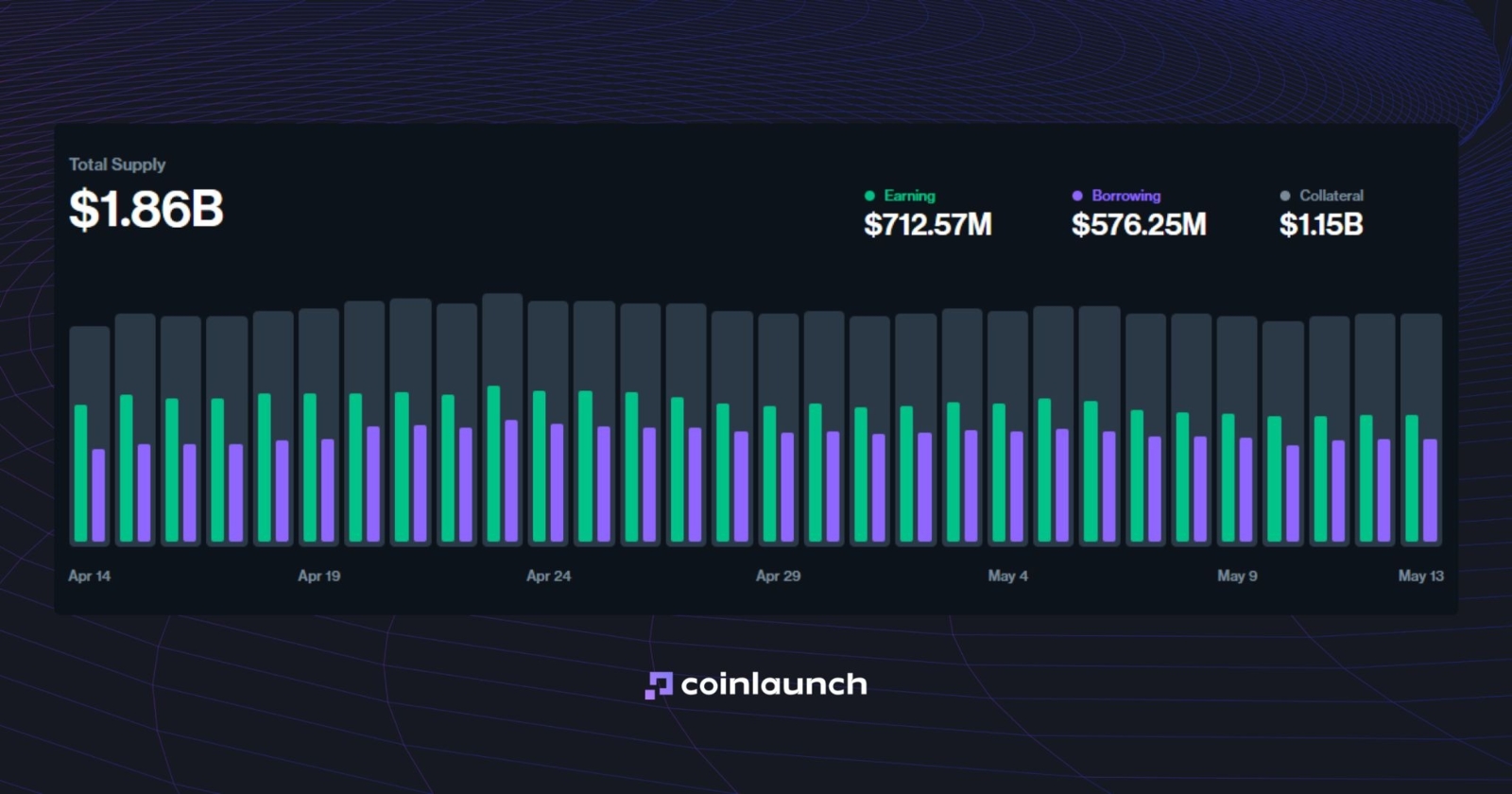

On the Compound DeFi lending protocol, users can deposit assets to earn interest or use cryptocurrency as collateral for loans.

According to Compound’s own data as of May 2026, total deposits stand at $1.86 billion, income-generating funds at $712.57 million, loans at $576.25 million, and crypto borrowing at $1.15 billion.

TVL by category. Source: compound.finance

Rates on Compound depend on liquidity demand and the parameters set by the protocol’s governance system. Compound loan terms for lenders and borrowers fluctuate with market activity. At the time of writing, yields for liquidity providers range from 0.05% to 3.33%, while borrowing rates range from 1.03% to 3.82%.

The COMP token governs the protocol: token holders can delegate voting rights to themselves or another participant and take part in decisions about the platform’s development. According to the dashboard, the system has 18,000 delegates, 220,000 token holders, 538 proposals, and a $7 million treasury.

Kamino Finance

So, what is Kamino Finance? It is a DeFi protocol within the Solana ecosystem that combines lending, liquidity, and leveraged strategies.

The platform’s first product was automated liquidity pools, launched in August 2022. In November 2023, Kamino introduced the Kamino Borrow lending product and expanded its operating model: users gained the ability to deposit assets into shared liquidity pools to earn lending yield or borrow against collateral.

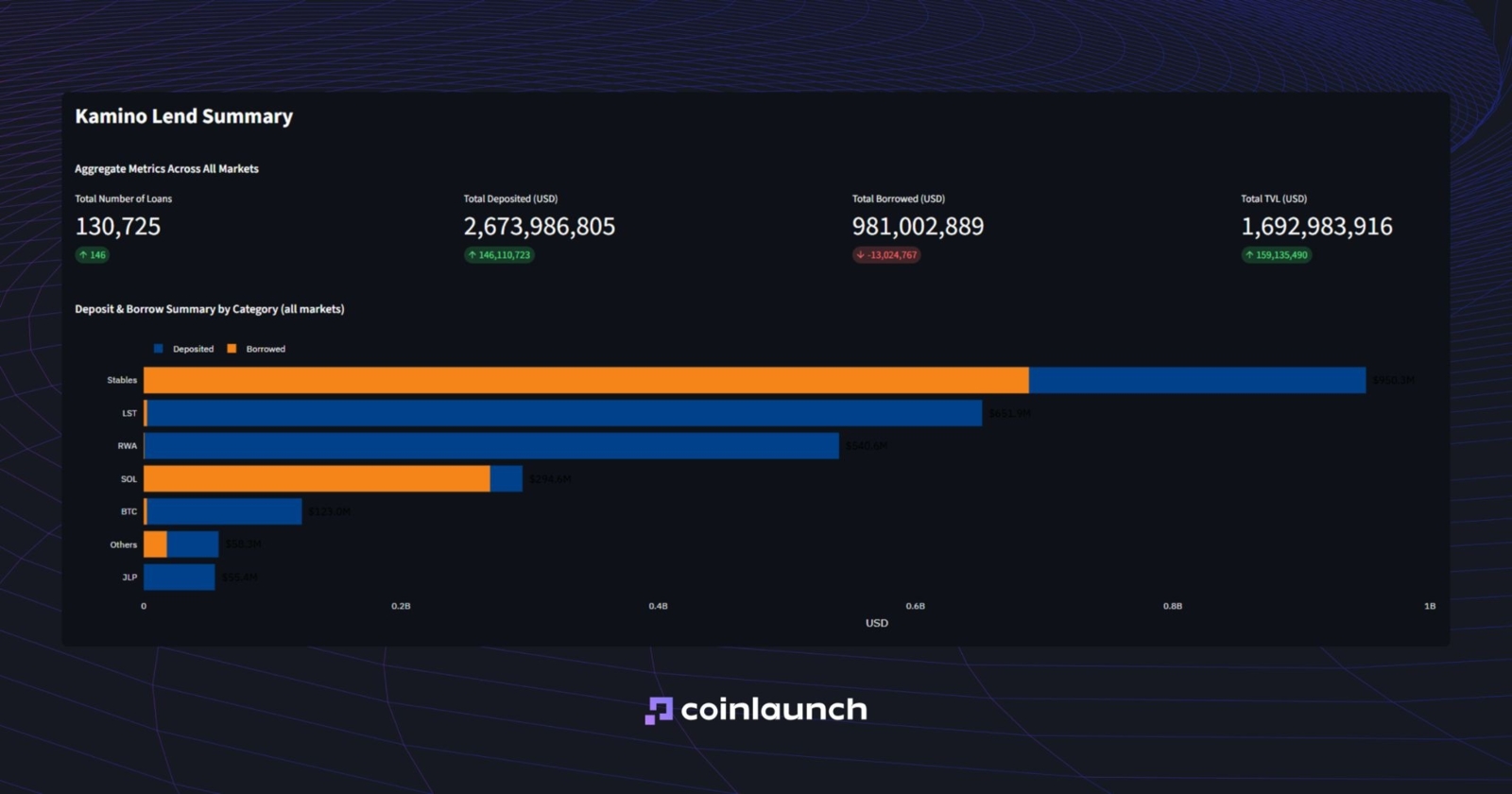

Today, the protocol has 130,000 loans, approximately $2.67 billion in deposits, $981 million in borrowings, and about $1.69 billion in TVL. Separately, the RWA Markets segment reports nearly $1 billion in assets under management (AUM).

Kamino Lend Summary Dashboard. Source: kamino.finance

Kamino Lend Summary Dashboard. Source: kamino.finance

Kamino uses a peer-to-pool model. Instead of directly matching lenders and borrowers, the protocol distributes liquidity through shared pools. Interest rates depend on pool utilization: the higher the demand for liquidity, the more expensive the loan.

Final Verdict on the Best Crypto Lending Platforms

You cannot choose the best crypto lending platforms based on a single factor. A low interest rate means little if the platform has weak security, unclear LTV terms, or cumbersome position management. High TVL does not make a service perfect either: it reflects market confidence, but does not eliminate other risks.

For traditional CeFi lending, consider Nexo, Ledn, or Arch. They offer clear terms, support, fiat payouts, and custodial collateral storage. For DeFi, consider Aave, Morpho, Compound, and Kamino. They provide more control but require a stronger understanding of how the protocols work.

DeFi Saver and Summer.fi do not compete directly with lending protocols. They operate on top of existing DeFi projects.

Sats Terminal is the best starting point for crypto borrowing. Its main advantage is aggregation. Users do not need to manually compare Aave, Morpho, Kamino, Ledn, and Arch: loan terms, LTV, and collateral amounts are consolidated in a single interface. This saves time and reduces the likelihood of choosing an insecure protocol.

The final choice depends on the use case: large lending protocols are suitable for independent analysis, CeFi platforms are best for custodial loans, and Sats Terminal is the way to go for quickly finding the best offer to borrow against BTC.

Research

Jason Shaw

July 31, 2026

14 min

The Best Crypto Marketing Agency for 2026: Our Insider's Shortlist backed by Real Reviews and Case Studies

Research

Daniel Bennett

July 30, 2026

15 min

The 10 Best Web3 Marketing Agencies of 2026, Ranked by 220+ Verified Reviews and Real Case Data

Research

Daniel Bennett

July 27, 2026

19 min

9 Top Crypto SEO Agencies of 2026, Backed by Client Interviews and Case Studies

No Comments

No comments yet