Table of contents

- What Is USDC Lending?

- How to Get USDC Loans Against Crypto Collateral

- How to Borrow USDC With Sats Terminal

- Does It Make Sense to Use USDC as Collateral Stablecoin?

- How to Lend USDC With Sats Terminal

- USDC Lending Rates: How Is the USDC Interest Rate Set?

- Where To Lend USDC: 6 BEST Stablecoin Lending Platforms

- Is Lending USDC Safe?

- Final Thoughts: Should You Borrow or Lend USDC?

Table of contents

- What Is USDC Lending?

- How to Get USDC Loans Against Crypto Collateral

- How to Borrow USDC With Sats Terminal

- Does It Make Sense to Use USDC as Collateral Stablecoin?

- How to Lend USDC With Sats Terminal

- USDC Lending Rates: How Is the USDC Interest Rate Set?

- Where To Lend USDC: 6 BEST Stablecoin Lending Platforms

- Is Lending USDC Safe?

- Final Thoughts: Should You Borrow or Lend USDC?

USDC lending works differently from lending BTC or ETH. Bitcoin and other crypto assets are more commonly used as collateral: users keep their exposure and access liquidity in stablecoins. USDC, by contrast, can be borrowed against crypto collateral, lent to other borrowers, or used as a yield-generating asset.

The answer to “can you borrow and lend USDC” is yes. But the better question is when it makes sense.

Borrowing against USDC usually makes little sense: the asset already functions as the dollar layer of crypto infrastructure. Lending USDC through an Earn product can be more useful: the stablecoin does not just sit idle in your wallet, but earns interest in USDC.

This guide covers how USDC lending works, how to borrow USDC against crypto collateral, why USDC is not always suitable as collateral, where to lend USDC, and what determines the USDC interest rate.

What Is USDC Lending?

USDC lending is a form of crypto lending. Users can borrow USDC against crypto assets as collateral, lend USDC to other borrowers through specialized platforms, or use USDC itself as collateral. So the answer to “what is USDC lending” is not just one thing: it is an umbrella term for lending activity involving USDC.

USDC is not the only asset used in stablecoin lending. Some platforms support USDC, DAI, and other fiat-pegged stablecoins.

Fundamentally, crypto lending follows the same principle as conventional lending: some participants provide capital, while others borrow it at interest. But instead of bank credit scores, credit history, and reputation, the system relies on collateral. For example, you can borrow USDC against BTC.

Similarly, if you want stablecoin loans in USDC, you must deposit ETH, SOL, XRP, or other assets as collateral, and the platform will calculate your borrowing limit based on that.

What is LTV in crypto? Source: coinlaunch.space

Then there is lending stablecoins. In this case, the user does not take out a loan but chooses to lend USDC. Their assets are used to issue loans to borrowers, who pay interest, with a portion credited back to the USDC holder.

How to Get USDC Loans Against Crypto Collateral

USDC loans work like other crypto-backed loans. You deposit BTC, ETH, SOL, or other crypto collateral, and the platform determines how much you can borrow in USDC. This is the basic answer to how to borrow USDC: you do not sell the asset, but use it as collateral to access liquidity.

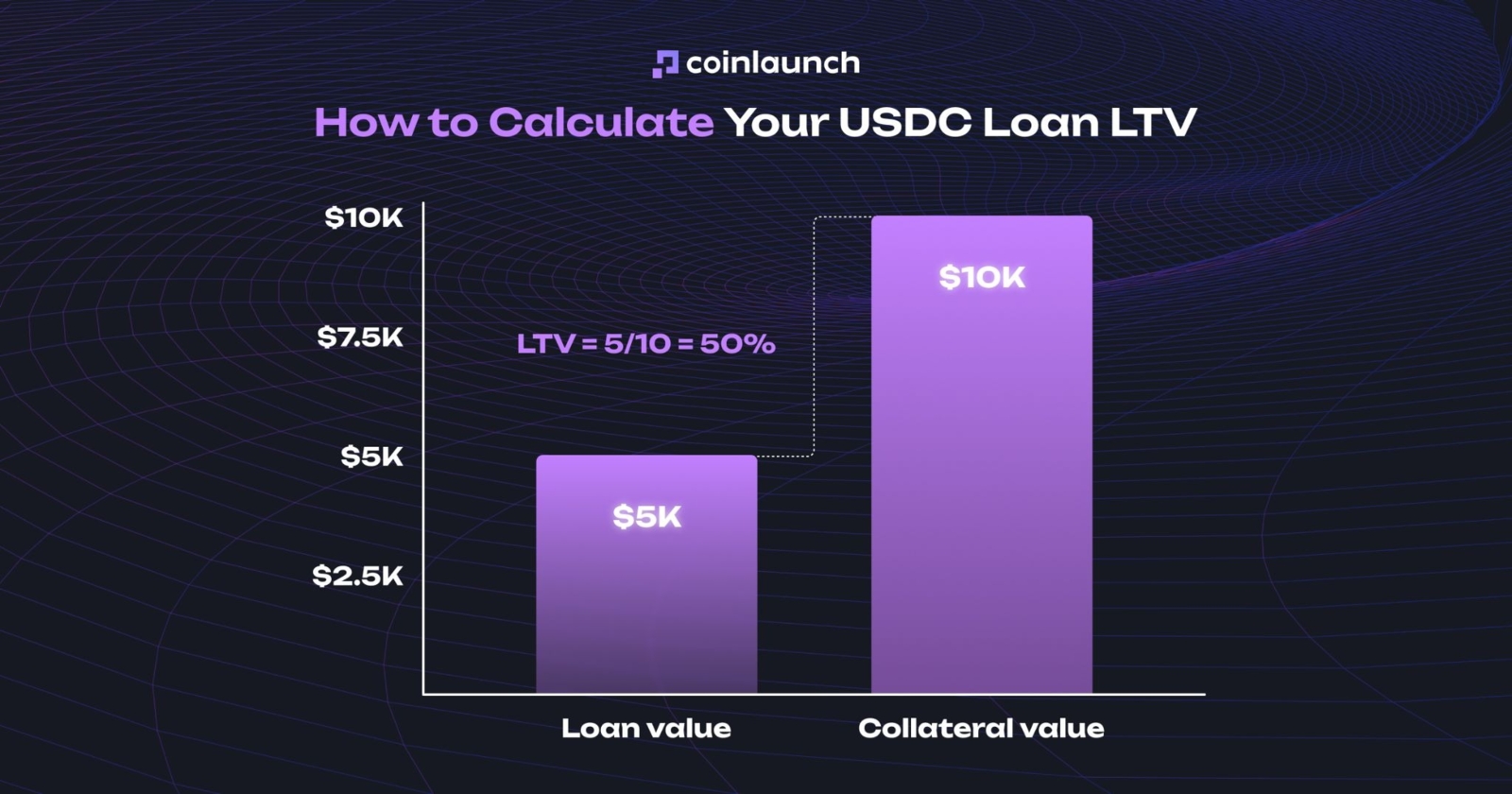

The key variable is LTV. It shows how much you can borrow relative to the collateral value. For example, with a USDC loan at 50% LTV, $10,000 in ETH lets you borrow $5,000 in USDC. The lower the LTV, the safer the position. The higher the LTV, the closer you are to liquidation.

How to calculate your USDC Loan LTV. Source: coinlaunch.space

USDC loan rates are usually stated as APR, the annual cost of the loan, including interest and fees. For example, on a $5,000 loan with 10% APR, you pay $500 per year. Depending on the platform, interest may be charged regularly or accrue until the position is closed.

If the collateral value rises, the LTV falls. Your position becomes safer, and you may be able to borrow more USDC against the same collateral. If the collateral value falls, the LTV rises. In that case, the platform may require additional collateral, partial debt repayment, or liquidate the collateral to close the position.

How to Borrow USDC With Sats Terminal

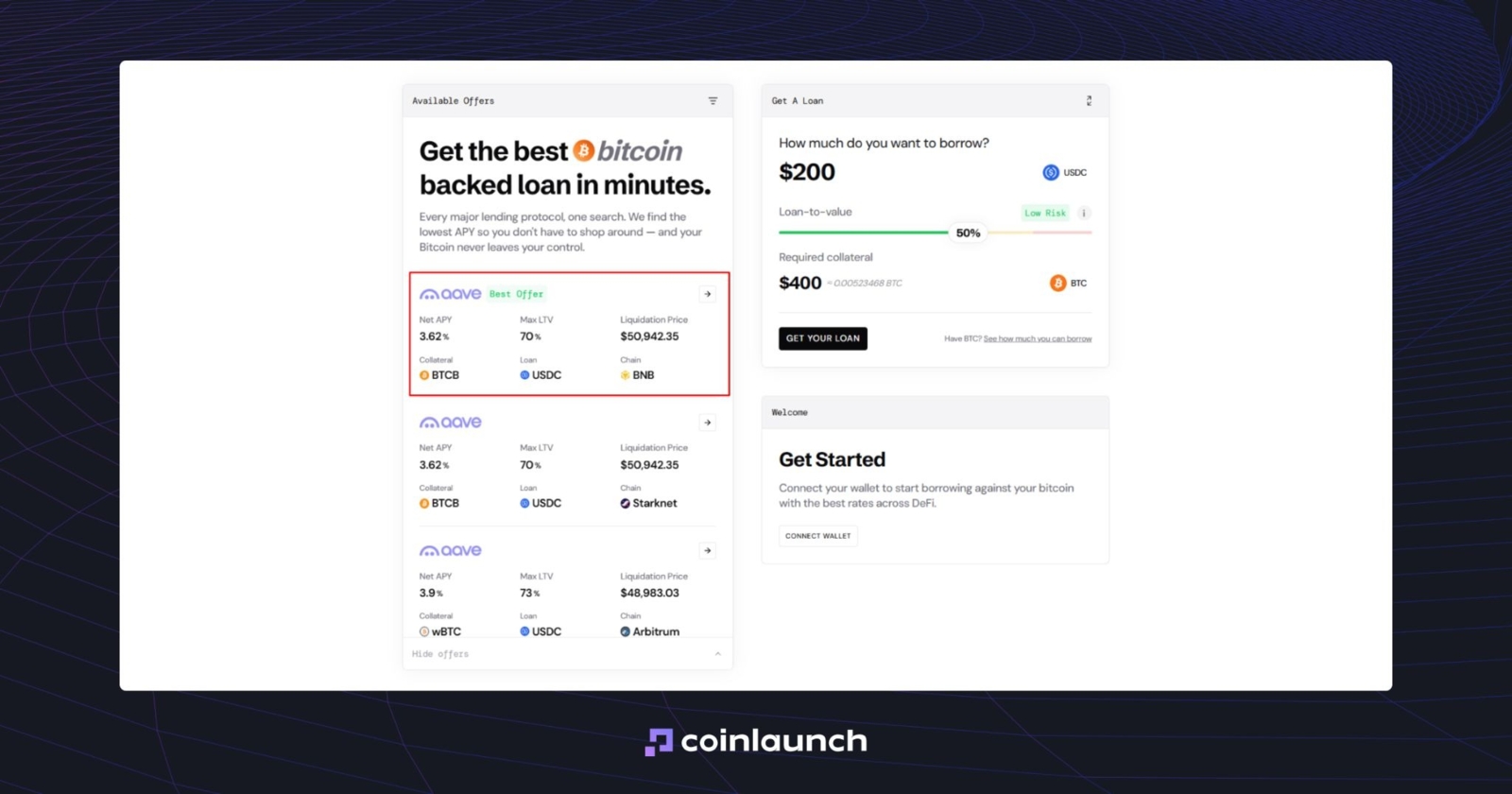

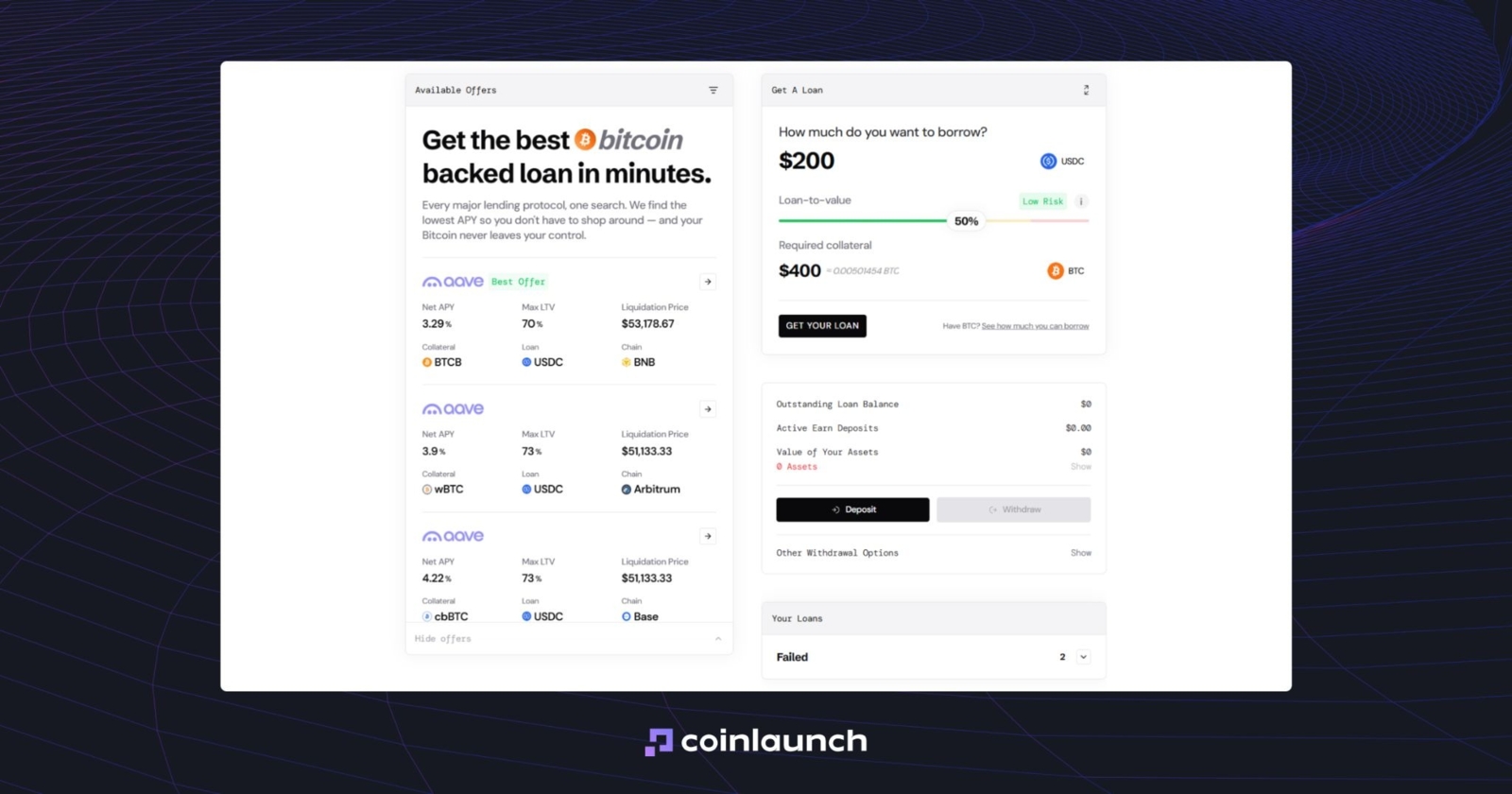

When you borrow USDC, you lock BTC as collateral and receive USDC. This is not called a USDC loan secured by Bitcoin. To show you step by step how to borrow USDC, we will use Sats Terminal, but the flow usually is the same for every platform — only the login options may vary from protocol to protocol.

First, open the aggregator and log in with your email. Sats Terminal will send a one-time code to verify it. The platform then creates a Privy wallet for you without KYC.

Next, enter the loan amount. Sats Terminal may suggest a starting amount, but you can change it yourself. You choose how much USDC you want to receive, and the platform shows how much BTC is required to open the position.

Available offers appear on the left. Net APY shows the total annual rate, including costs and returns. Max LTV is the maximum ratio of the loan amount to the collateral value. Liquidation Price is the BTC price at which the platform will liquidate your position. Currently, the best USDC Net APY is 3.62%.

The best Net APY for borrowing USDC against BTC on Sats Terminal. Source: satsterminal.com

If the details are correct, click “Continue.” Sats Terminal will generate a unique BTC address for the selected USDC loan. Transfer the exact BTC amount displayed to this address by copying the address or scanning the QR code.

After your deposit is confirmed, the BTC arrives at a one-time deposit address. The asset is then automatically wrapped into the standard required by the protocol, such as wBTC on Ethereum, cbBTC on Base, or BTCB on BSC, so you do not need to bridge it yourself. It is then used as collateral on Aave or another crypto lending platform.

Does It Make Sense to Use USDC as Collateral Stablecoin?

Using USDC as a collateral stablecoin usually makes less sense than pledging BTC, ETH, or another asset. USDC already functions as the dollar layer of crypto, so locking it as collateral to borrow dollars or another stablecoin only adds friction to a simple transaction. Instead of accessing liquidity, you take on USDC loan rates, fees, repayment terms, and platform risk.

This only makes sense if you want to avoid realizing capital gains for tax reasons, cannot sell the asset directly, or face withdrawal restrictions.

For most use cases, USDC works better as a lending asset than as collateral. If you already hold USDC, it is usually more logical to lend USDC and earn yield than to borrow against a dollar-pegged asset.

How to Lend USDC With Sats Terminal

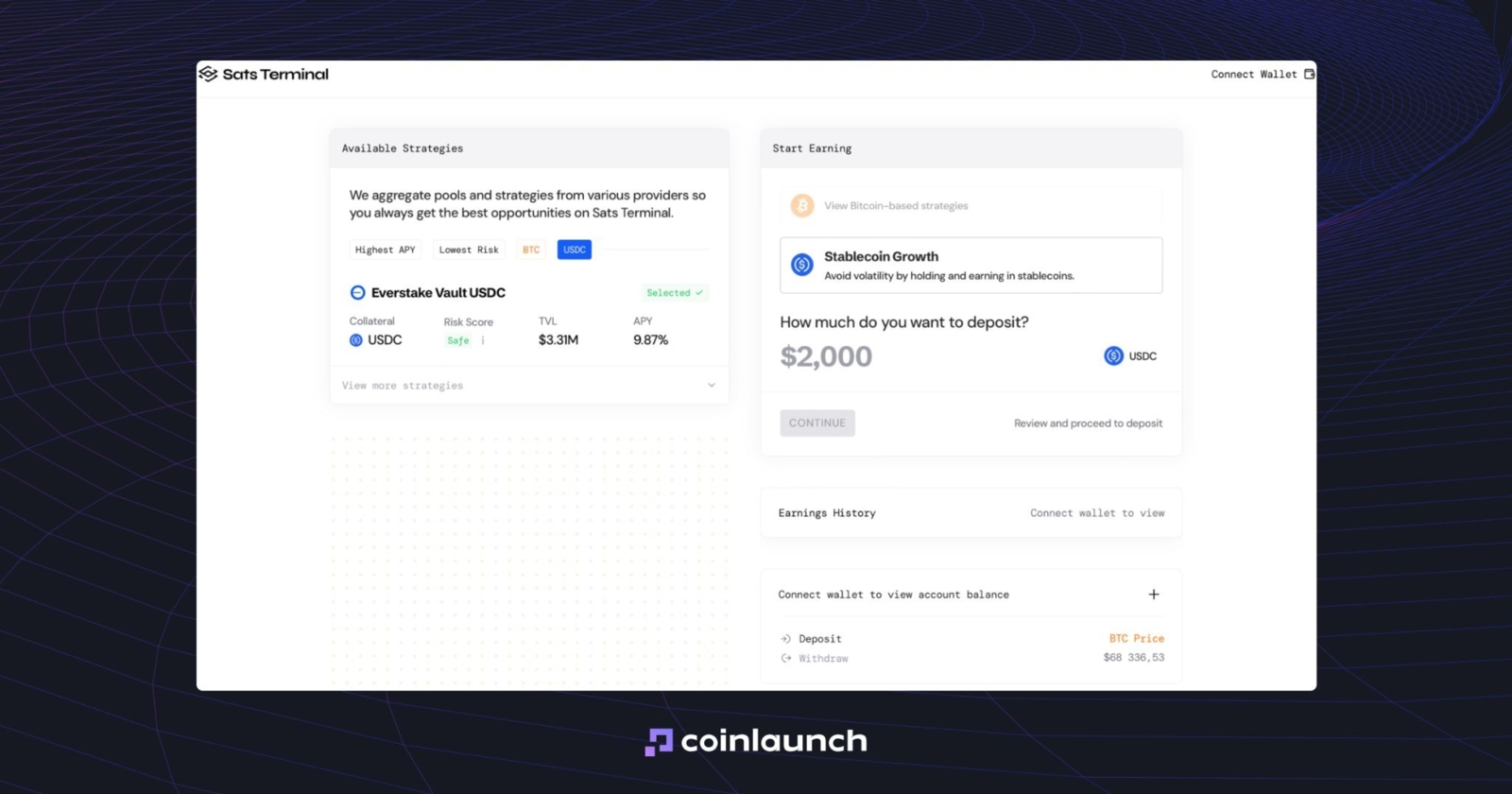

USDC lending is easier to explain through a specific product. Once again, we will use an example Sats Terminal to show you how to lend USDC. Sats terminal features a separate Earn section where you can earn yield on Bitcoin and USDC. With USDC, this is not a collateralized loan, but rather a stablecoin deposit to earn yield on your stablecoins across leading lending protocols.

Stablecoin Growth in the Earn Sats Terminal section. Source: satsterminal.com

Enter the lending amount and select the position that fits your needs. With the Sats Terminal, you do not need to open several USDC DeFi lending platforms, compare vaults, networks, fees, and terms manually. The platform aggregates available yield options in a single interface and displays current competitive rates.

If the chosen strategy fits your needs, proceed with the deposit. Earn generates a unique address for the principal deposit. Send USDC from your wallet to this address. If the asset is already in your platform wallet or was received through another Sats Terminal product, you can skip this step.

After you send the funds, the platform waits for blockchain confirmation.

Sats Terminal handles the final technical steps automatically. If the strategy requires a different network, supplying assets to a specific provider, or staking into a vault, Earn handles it for you.

Once processed, the principal begins to generate yield. Currently, Earn allows users to lend USDC at up to 8.77% APY. This is the highest rate available for USDC lending.

USDC Lending Rates: How Is the USDC Interest Rate Set?

USDC lending rates depend on where the asset is deployed: a CeFi product, a DeFi protocol, or an aggregator such as Sats Terminal. Some platforms show a fixed rate upfront. Others adjust the USDC interest rate based on borrowing demand, available liquidity, and provider terms.

Higher demand for borrowing USDC usually means higher potential yield for those lending USDC. If borrower demand is high and available liquidity is low, the platform raises the rate to attract more USDC. If liquidity is sufficient but loan demand is weak, the rate usually falls.

In DeFi, the utilization rate also affects yield. It shows how much of the lending pool borrowers have already drawn down. If the pool holds a lot of USDC but few users are borrowing, the yield tends to be lower. If borrowers are using most of the pool, the rate rises: the protocol needs to retain liquidity and avoid a liquidity crunch.

Aave showed this in April 2026, when its Ethereum Core USDC pool stayed near full utilization for four days, with variable borrow rate around 14%.

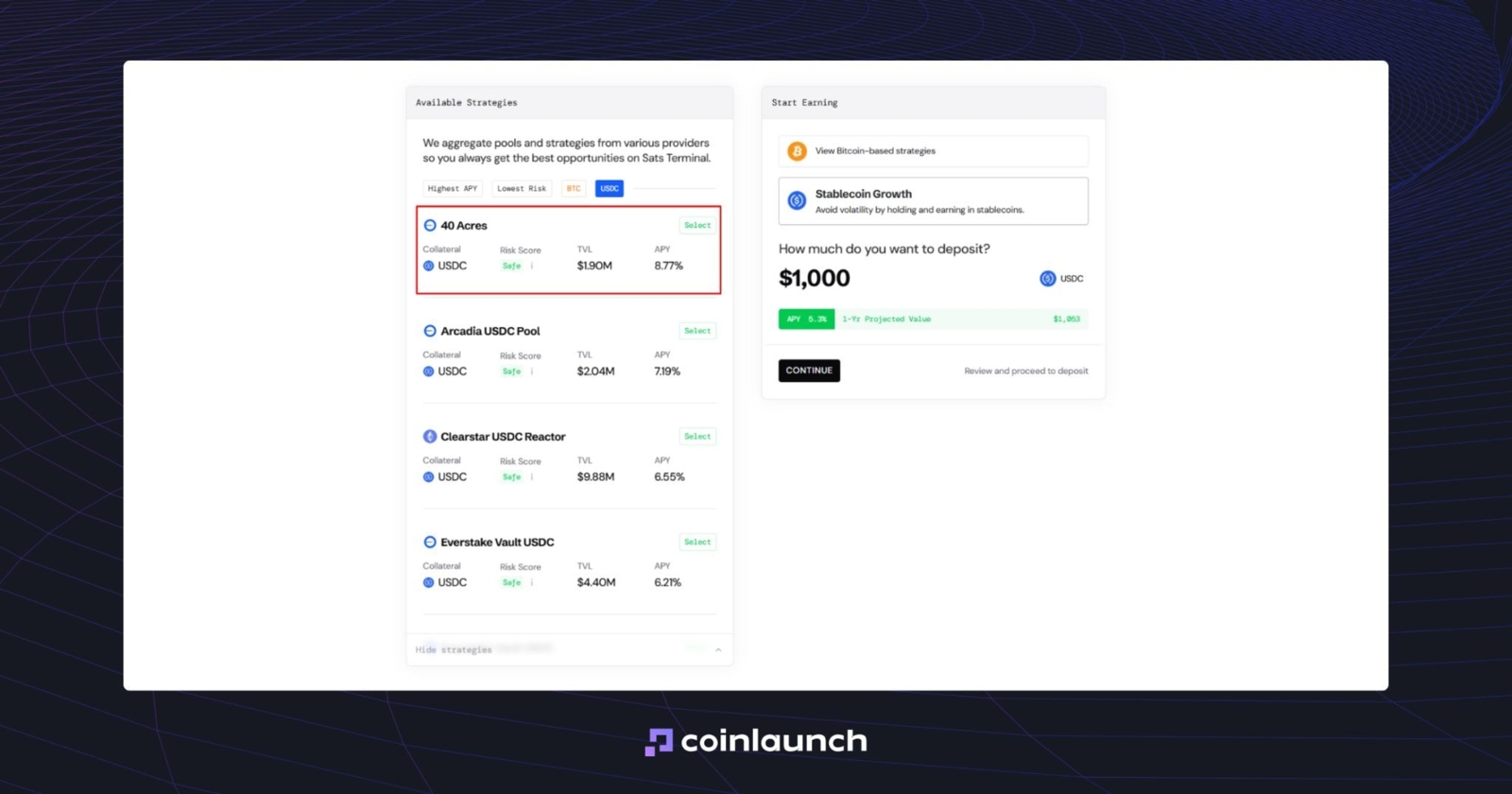

In Sats Terminal Earn products, you can see the final terms right on the dashboard. The platform shows the strategy name, collateral, risk score, TVL, and APY. For example, the 40 Acres strategy for USDC shows a Safe risk score, $1.9M in TVL, and 8.77% APY.

An example of an Earn strategy on Sats Terminal. Source: satsterminal.com

❗ Important: Do not confuse the USDC interest rate with a guaranteed return. The rate may change if loan demand, pool utilization, provider terms, or market conditions shift. The best USDC lending rates are therefore not simply the highest APY, but the rate that makes sense after you factor in risk, terms, fees, and the platform model.

Where To Lend USDC: 6 BEST Stablecoin Lending Platforms

USDC lending is available through DeFi protocols, CeFi platforms, exchanges, and aggregators. Here are six of the most relevant options.

Aave and Compound give users access to DeFi liquidity pools without KYC, but they also require users to choose the network, track gas fees, and monitor market risk. Lending USDC on Aave yields 3.68% APY. On Compound, liquidity provider yields range from 0.05% to 3.33%.

Coinbase offers USDC lending through Morpho. Users can deposit USDC into a Morpho-connected vault and earn up to 10.3% APY, but the product is available only to verified customers. Nexo and Ledn cover the CeFi side: Nexo offers up to 9.5% APY on USDC, while Ledn offers 6.5% APY on balances up to $100,000 and 8.5% APY on balances over $100,000.

APY alone is not enough to compare these options. Each platform has its own supported stablecoins, minimum deposit, custody model, KYC requirements, networks, TVL, and withdrawal terms. Choosing a USDC lending platform quickly turns into manual research across protocols, vaults, and Earn products.

Read more: “6 BEST Stablecoin Lending Platforms to Loan and Borrow USDC or USDT”

An aggregator makes this easier. Sats Terminal brings Earn strategies into a single interface, so users can lend USDC without tracking Aave, Morpho, CeFi platforms, networks, and strategy terms themselves.

The main interface of Sats Terminal. Source: satsterminal.com

Through Earn, users can lend USDC at up to 9.64%. Among the highest-TVL strategies, Everstake Vault USDC stands out with $4.41M in TVL, a Safe risk score, and 6.52% APY.

Is Lending USDC Safe?

Calling USDC lending entirely risk-free would be inaccurate. USDC is less exposed to market volatility than BTC, ETH, or SOL, but lending is still a credit product. Once assets move into a protocol, you are exposed to protocol risk.

The main USDC lending risks are platform risk, rate changes, and the quality of the collateral backing borrower loans. If a borrower receives USDC against BTC, ETH, or another major crypto asset, the risk of a sudden drop in collateral value is much lower than with smaller altcoins.

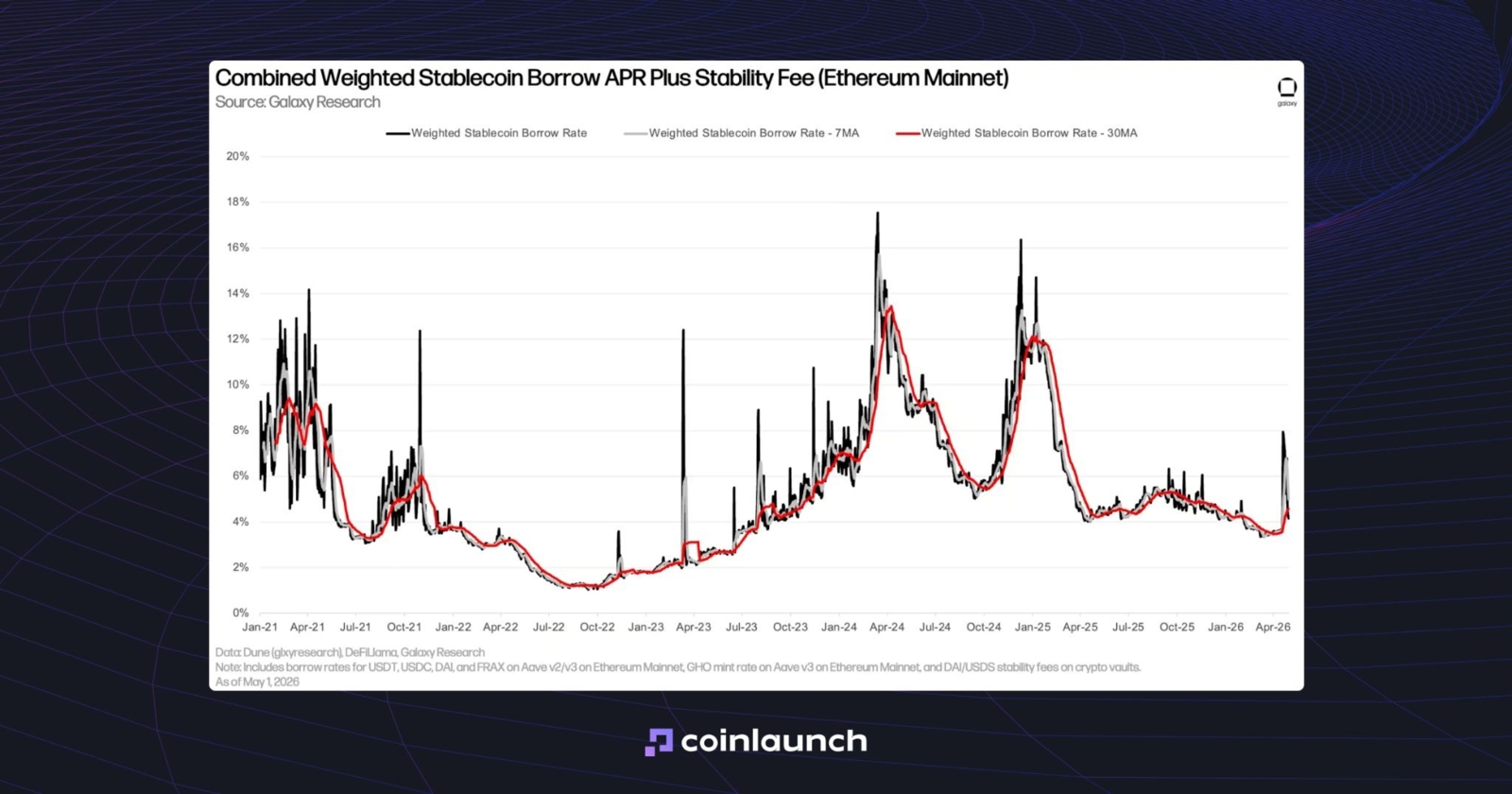

Rate volatility also matters. On-chain rates depend on loan demand, available liquidity, and market conditions. For example, after the rsETH exploit, stablecoin lending rates spiked because liquidity dried up.

Stablecoin yields rose to 7.9% after liquidity dried up following the rsETH vulnerability. Source: galaxy.com

Before lending USDC, do not focus only on yield. TVL, risk score, collateral quality, vault terms, custody model, and platform reputation - all of them matter.

Final Thoughts: Should You Borrow or Lend USDC?

If you need liquidity against BTC, ETH, or other crypto collateral, you can borrow USDC. You keep exposure to the asset, receive a stablecoin for use across crypto or off-platform withdrawals, and avoid selling your position. But this liquidity comes with an interest rate.

If you already hold USDC, you can use it as collateral to borrow dollars or another stablecoin, but that often makes little sense: USDC already functions as a dollar-denominated asset.

For most users, the better option is to lend USDC. The stablecoin goes into a lending pool, vault, or Earn product and earns yield. But APY should not be the only factor: before choosing a platform, consider the risk score, TVL, custody model, strategy terms, and provider risk.

Was this article helpful?

Share this blog post

Research

Jason Shaw

August 6, 2026

15 min

The Best Crypto Marketing Agency for 2026: Our Insider's Shortlist backed by Real Reviews and Case Studies

Research

Jason Shaw

August 5, 2026

14 min

Best Solana DEX List: How to Choose the Best DEX on Solana

Research

Daniel Bennett

August 4, 2026

21 min

9 Top Web3 Branding Agencies of 2026: Crypto & Blockchain Design Studios, Judged on Shipped Work

No Comments

No comments yet