Table of contents

- Crypto Loan vs. Bank Loan

- How to Borrow Against Crypto

- How Borrowing Against Crypto Actually Works

- How to Find the Best Crypto Lending Rates

- Why Borrow Against Crypto

- Exploring the Types of Crypto Borrowing

- CeFi Lending: Centralized Crypto Loans Explained

- DeFi Lending: Decentralized Crypto Loans Explained

- DeFi vs. CeFi Lending: A Side-by-Side Comparison

- Crypto Lending Risks

- How to Choose the Best Crypto Lending Platform

- Crypto Loans: Final Thoughts

Table of contents

- Crypto Loan vs. Bank Loan

- How to Borrow Against Crypto

- How Borrowing Against Crypto Actually Works

- How to Find the Best Crypto Lending Rates

- Why Borrow Against Crypto

- Exploring the Types of Crypto Borrowing

- CeFi Lending: Centralized Crypto Loans Explained

- DeFi Lending: Decentralized Crypto Loans Explained

- DeFi vs. CeFi Lending: A Side-by-Side Comparison

- Crypto Lending Risks

- How to Choose the Best Crypto Lending Platform

- Crypto Loans: Final Thoughts

For a long time, holding Bitcoin, Ethereum, or other cryptocurrencies tied the owner to that asset: if they needed funds “right here and now,” selling was the only way to access them. Today, this has changed: crypto lending protocols allow users to borrow stablecoins by providing cryptocurrency as collateral, or to earn interest by lending out their digital assets.

These products gave users something traditional cryptocurrency storage lacked: access to liquidity without having to sell their assets. Holders could borrow against crypto such as ETH or BTC, receive stablecoins, and use them for spending, investing, or portfolio management, all while retaining their underlying position.

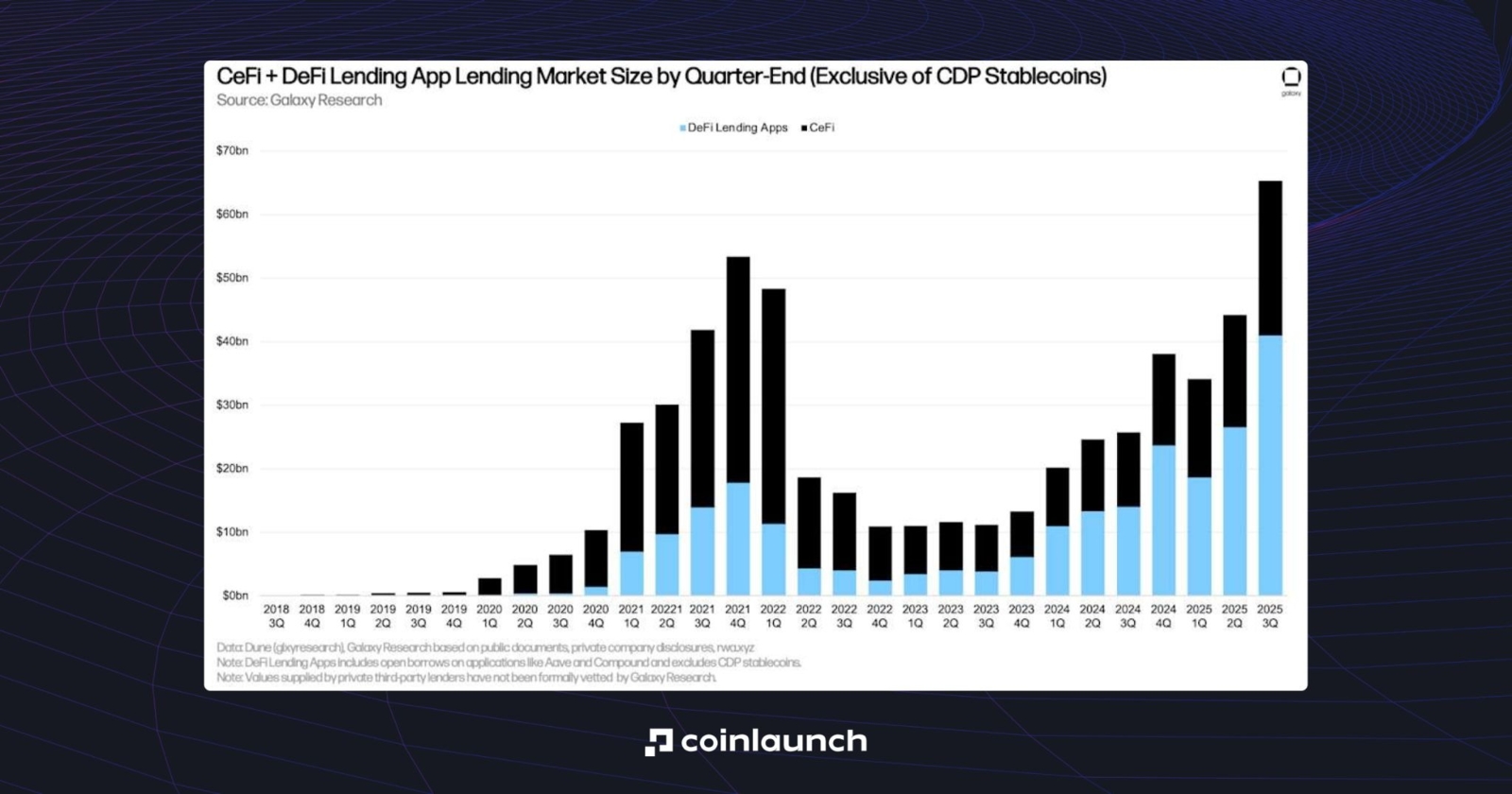

Such a product revolution sparked massive market growth. The first protocols emerged in 2017: over the following years, Maker, ETHLend (now Aave), and Compound were launched. CeFi lending platforms such as BlockFi, Celsius, Genesis, and Nexo also entered the market.

Comparison of CeFi and DeFi lending platforms by market share, 2018-2025. Source: galaxy.com

But in such a large industry, how do you take advantage of the market? In this article, we’ll explore exactly how this process works, the mechanics underlying lending, the differences between CeFi and DeFi models, and the rates and terms offered by platforms.

Crypto Loan vs. Bank Loan

Any topic related to crypto assets is best understood by comparing it with traditional finance. In the case of cryptocurrency lending, we’ll apply the logic of bank lending and examine the key differences between crypto loans and bank loans.

Bank lending is based on solvency and credit rating: an employee at, say, Goldman Sachs would evaluate the borrower’s salary, assets, debts, and property. However, even having enough assets to cover the loan is not always enough for approval. At a bank, the human factor also plays a role: the customer’s reputation and their loyalty to the specific bank from which they are taking out a loan.

When it comes to crypto collateral loans, the only thing that matters is the value of the collateral: not your skin color, not your reputation, not your job, only whether you have enough funds to cover the loan if you lose it.

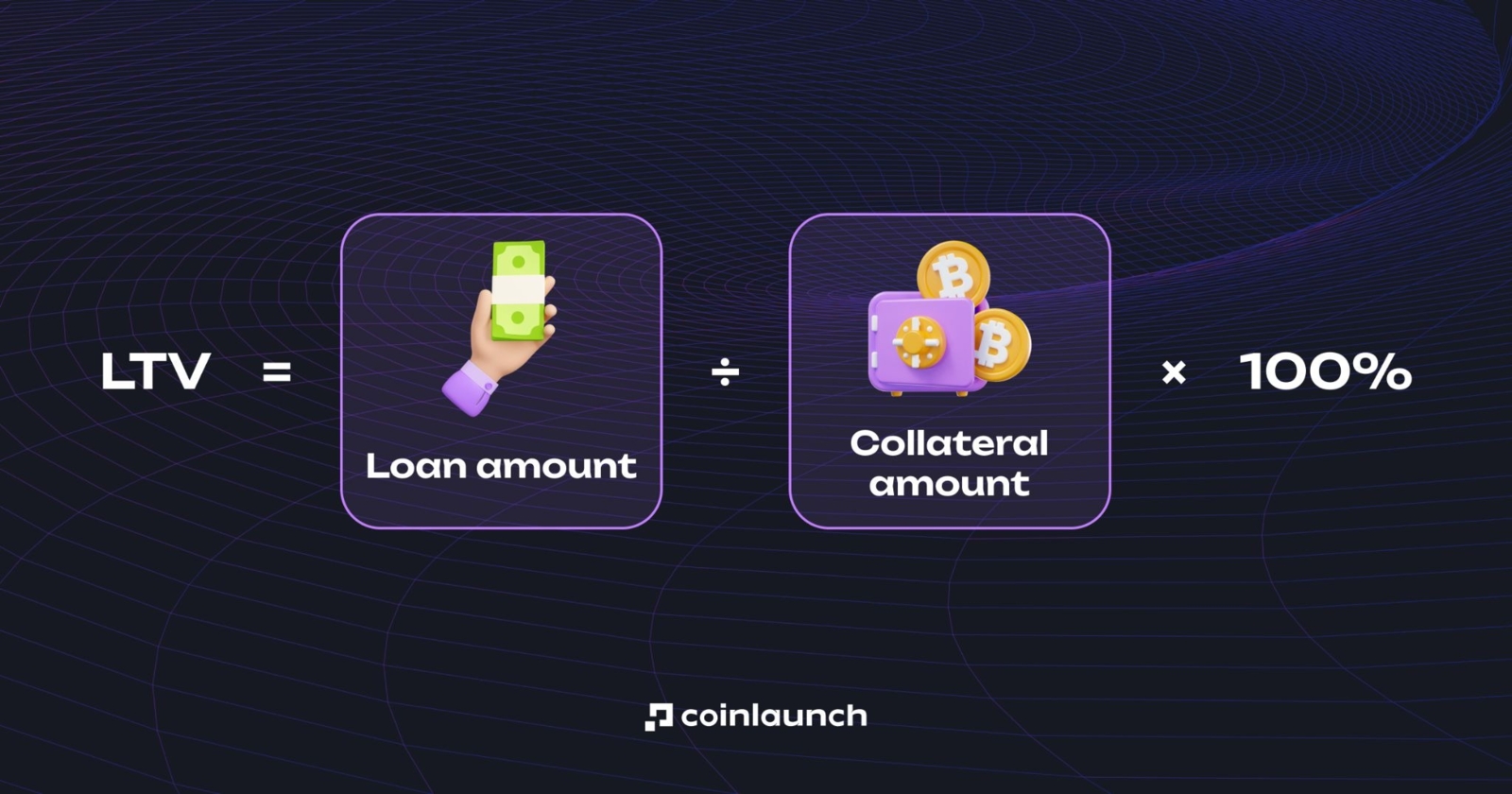

This is determined by the LTV (loan-to-value) ratio. It shows how much you can borrow relative to the value of the collateral. For example, with an LTV of 50%, you can only get a crypto loan for half the value of the collateral. In other words, with a $5,000 deposit in Ethereum, you can borrow $2,500.

What is LTV (loan-to-value) in crypto lending? Source: cropty.io

If the value of the collateral drops and the LTV exceeds the platform’s acceptable limits, the protocol requires additional collateral. If those requirements are ignored long enough and the LTV approaches a certain value (usually around 80 to 85%, depending on the platform), it liquidates your position. Meanwhile, at a bank, if a borrower defaults on a loan, recovering the funds usually takes much longer and, moreover, does not always result in repayment. This is often what causes banks to fail.

As you can see, a bank loan is suitable for those who have verified income, a good reputation, and a solid credit history. Crypto backed loans, on the other hand, are suitable for those who have a reserve of crypto assets they do not want to sell but need cash right now.

How to Borrow Against Crypto

The best way to illustrate the process of borrowing against crypto is to use a specific platform as an example. To see the difference between these services in practice, we’ll use the Sats Terminal aggregator. We’ll demonstrate the rest of the process on this platform, but you’re free to choose whichever one works best for you.

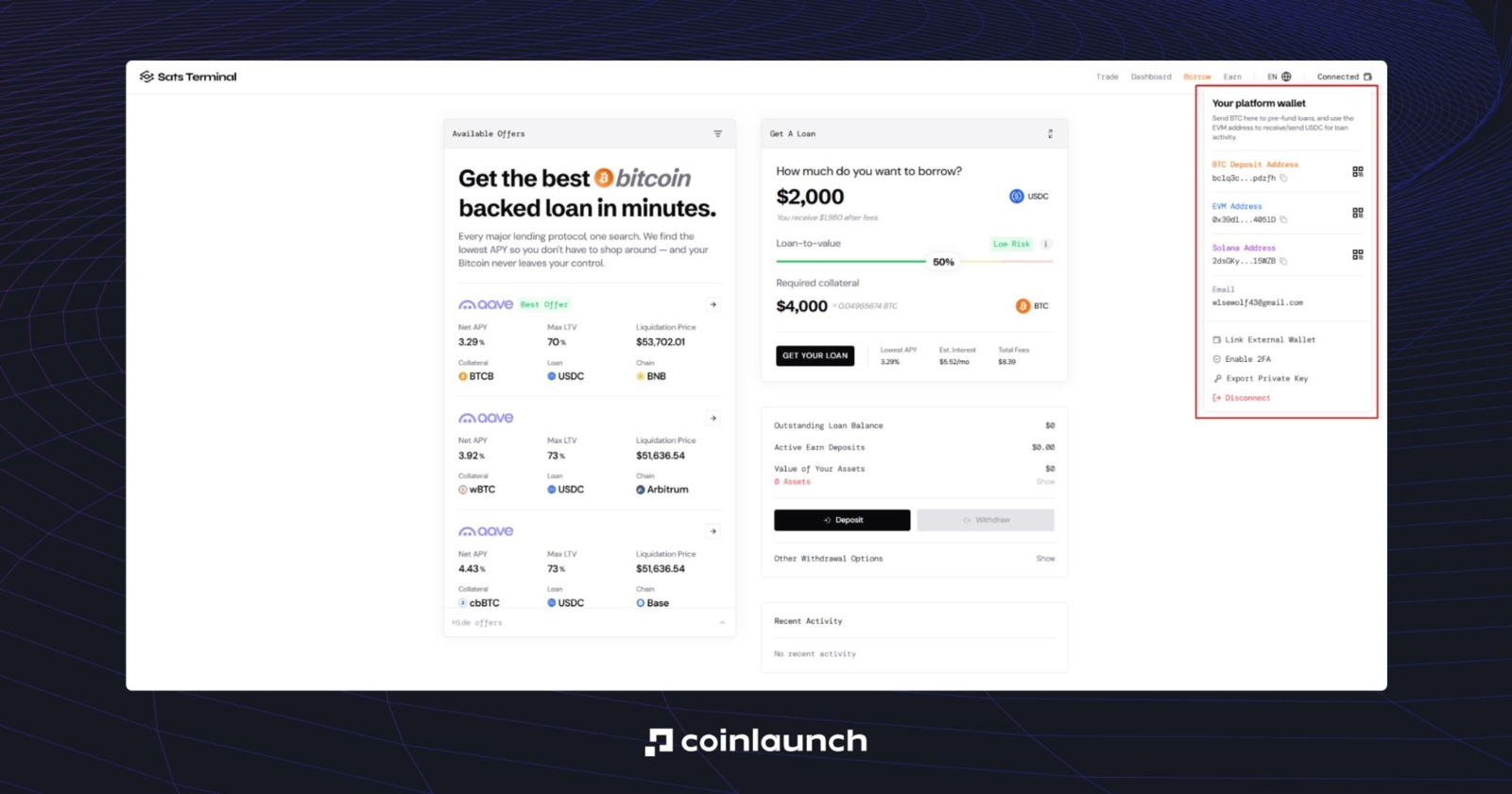

Go to the aggregator’s page and connect your cryptocurrency wallet. Sats Terminal will ask you to enter your email for identity verification: enter it, confirm it with a one-time code, and proceed to the next step. At this stage, your personal Privy wallet has already been created: no KYC required.

A cryptocurrency wallet on the Sats Terminal. Source: satsterminal.com

Now enter the loan amount you wish to borrow. The platform defaults to $2,000; click on this field to change it to the appropriate amount.

Below is the Loan-to-Value (LTV) slider: use the slider to set the desired value. A level up to 50% is considered Low Risk, up to 65% is Medium Risk, and anything higher is High Risk. The higher the LTV, the higher the risk of liquidation: if the value of the collateral begins to fall, the platform may require you to add collateral or forcibly close the position.

The value of the collateral obviously falls along with the price of the collateral asset. Therefore, a low LTV and a low-volatility cryptocurrency present the lowest risk of loss. Collateral in ETH and collateral in some memecoin are not the same thing: the price of a memecoin can drop so quickly that the protocol will automatically close the position, and you won’t have time to add additional collateral.

This is precisely why Sats Terminal supports only BTC lending: you can deposit only BTC and receive USDC.

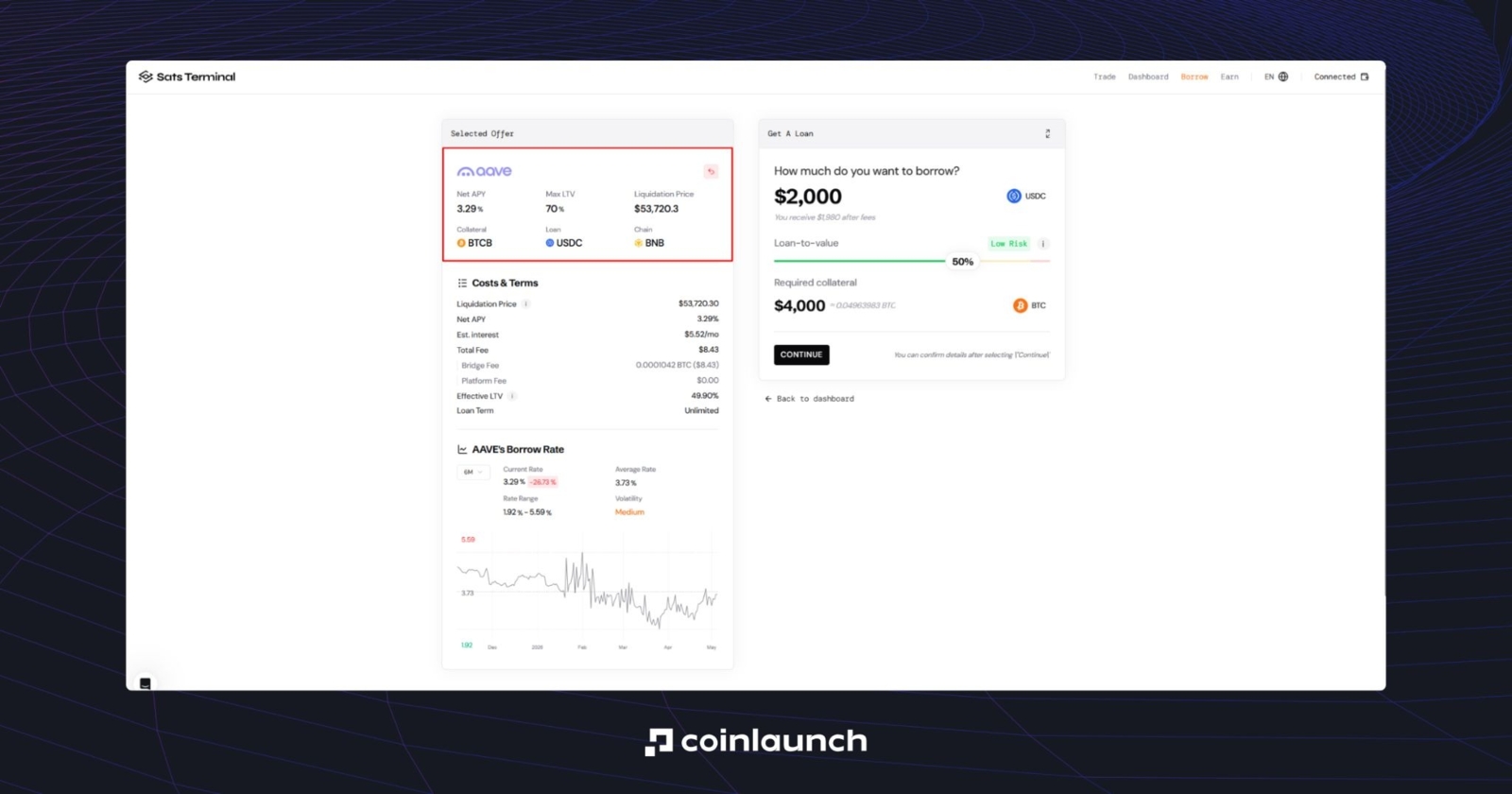

On the left side of the website page is a list of crypto assets available for borrowing crypto. Net APY shows the total annual rate, taking into account costs and returns; Max LTV is the maximum loan-to-value ratio; and Liquidation Price is the asset price at which the platform will forcibly close the position.

Net APY, Max LTV, and Liquidation Price on Sats Terminal. Source: satsterminal.com

Read this article to the end to understand these and other metrics — we’ll go over them in more detail below.

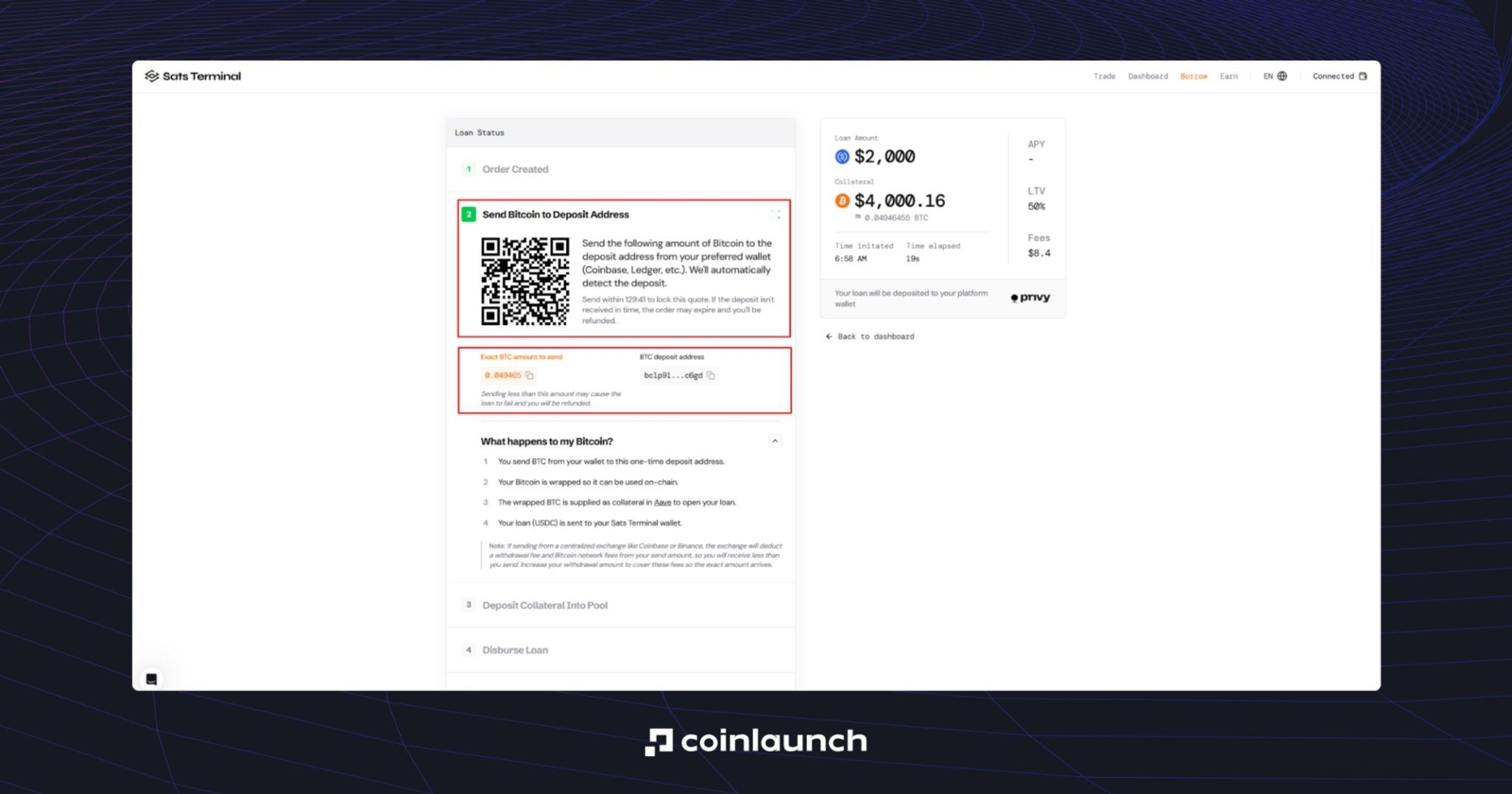

Let’s say the selected offer works for us, click “Continue.” At this stage, the platform generates a unique BTC address for your loan. Send your funds from your wallet or exchange. It’s important to transfer exactly the amount specified in the order: you can do this either via the address or the QR code.

An interface for obtaining a crypto loan by transferring collateral to a unique BTC address. Source: satsterminal.com

First, BTC is sent to a one-time deposit address. The asset is then converted into a protocol-compatible format (wBTC on Ethereum, cbBTC on Base, BTCB on BSC, and so on) and used as collateral on Aave (or another selected crypto lending platform) to take out a loan.

The final step is to deposit USDC into your Sats Terminal wallet. From there, you can withdraw the funds to your wallet, to an exchange, and then into cash.

How Borrowing Against Crypto Actually Works

The key metrics in crypto lending are LTV and Health Factor. These metrics determine the financial security of your position. For example, on Aave, a position is liquidated when the Health Factor falls below 1, while on Morpho, it is liquidated if the current LTV reaches the LLTV (Liquidation Loan-to-Value) threshold, after which the collateral is put up for sale.

However, liquidation is not caused only by a collapse in the market value of the collateral. A position can weaken even in a consolidating market because of accrued interest. This increases the principal amount of the debt, which automatically puts pressure on the Health Factor.

In other words, when borrowing against crypto, you need to monitor the market value of the collateral, the amount of debt, and the margin to liquidation levels at the same time. Remember: if liquidation has already occurred, you will not be able to recover these funds.

For those who use crypto lending to reinvest borrowed funds, it is important to know how to correctly calculate Net APY, the annual percentage yield on investments.

A common mistake is to calculate Net APY as simply the difference between Supply APY (annual return on deposits) and Borrow APY (annual interest rate on loans). This approach only works if the market value of the collateral and the debt are the same, such as with USDC and USDT, but in practice this is rarely the case.

First, you need to calculate Net Return:

Deposit income − interest expense − (change in debt price − change in collateral price) − fees.

Then divide the result by your initial Equity, that is, the value of the collateral minus the debt, and annualize it.

How to Find the Best Crypto Lending Rates

Interest rates in DeFi and CeFi crypto lending are not static: they fluctuate based on market demand and liquidity in specific pools. Manually checking each protocol is inefficient, which is why data aggregators are used to find the best terms.

These tools aggregate data from dozens of sources on a single platform, allowing users to compare the annual percentage yield (APY) as well as risk parameters: maximum LTV and liquidation threshold.

Key tools for comparing interest rates:

- Sats Terminal: One of the most user-friendly aggregators. It compiles the best offers from Morpho, Aave, and other platforms. It immediately displays the total cost of the loan (Net APY) and calculates the liquidation price based on your collateral amount.

- DefiLlama: A global service for DeFi analytics. In the “Borrow” section, you can filter offers by a specific asset (e.g., USDC or ETH) and see where the most favorable terms are currently available.

Beginners often prefer data aggregators: they allow users to get a broader view of the market, find a suitable platform, and continue working with it.

Why Borrow Against Crypto

The only truly important reason to borrow against crypto is to access liquidity without selling the asset. You may need cash at any moment, but not everyone is willing to fully exit their position and forgo the asset’s potential growth after selling.

These funds can then be used as a tool for a more sophisticated investment strategy: to participate in upcoming token sales, CEX promotional campaigns, staking, restaking, speculating on short-term trends, and so on. If the cryptocurrency owner is an entrepreneur in the traditional economy, they can also use the collateral to finance the business’s operating expenses.

Loans for crypto are also used to increase market exposure without opening a futures position. In this case, the investor takes out a loan against an existing asset and uses the borrowed funds for additional purchases or other yield-generating strategies. This is similar to using leverage, but without the funding rate typical of perpetual futures.

What’s more, it can be done fairly quickly: whether in CeFi or DeFi, it usually takes just a few minutes to secure a loan. Yes, it takes longer than simply selling an asset, but you retain your position and gain the right to redeem the asset later at the same loan value plus the protocol’s fee.

In addition, crypto borrowing is generally not considered a taxable event in many jurisdictions, as it does not constitute the sale of an asset. However, tax implications may still arise depending on the country, the structure of the transaction, and how the platform handles the collateral.

Exploring the Types of Crypto Borrowing

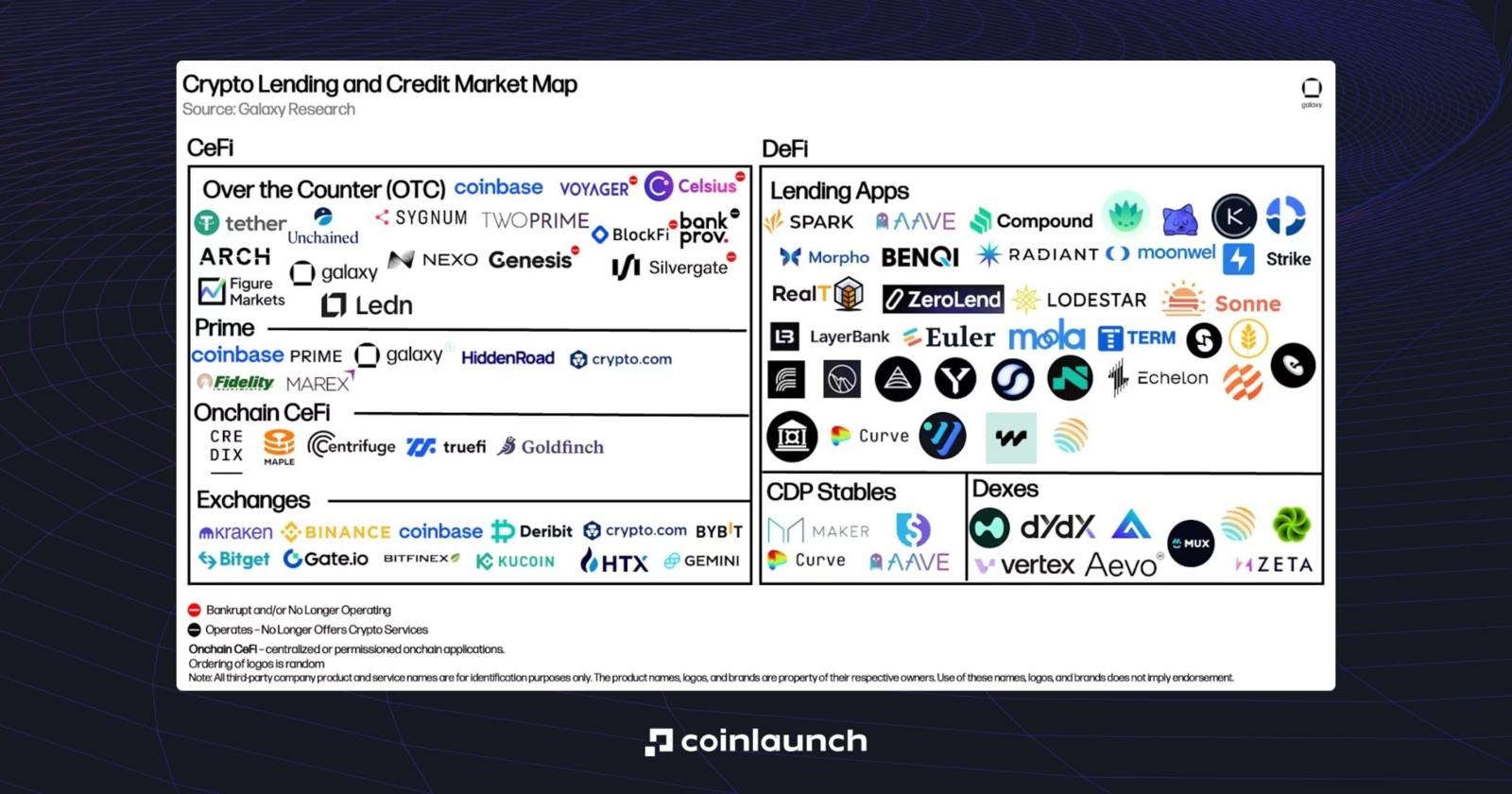

Crypto lending is traditionally classified by its degree of decentralization: CeFi or DeFi. Additionally, the CeFi segment includes OTC lenders, prime lending services, on-chain CeFi solutions, and centralized exchanges. DeFi includes lending apps, CDP protocols (where loans are structured through the issuance of a stablecoin backed by collateral), and DEXs.

The crypto lending project market. Source: galaxy.com

In the first case, the user interacts with a centralized platform that handles asset custody, sets loan terms, and may require identity verification. In the second case, the protocol manages loan issuance, interest calculations, and position liquidation without an intermediary.

CeFi Lending: Centralized Crypto Loans Explained

Centralized crypto lending platforms emerged in response to the cumbersome user experience of DeFi protocols at the time. The main feature of centralized crypto loans is a more familiar user experience: they often offer fixed interest rates, customer support, and the ability to use a wider range of collateral assets.

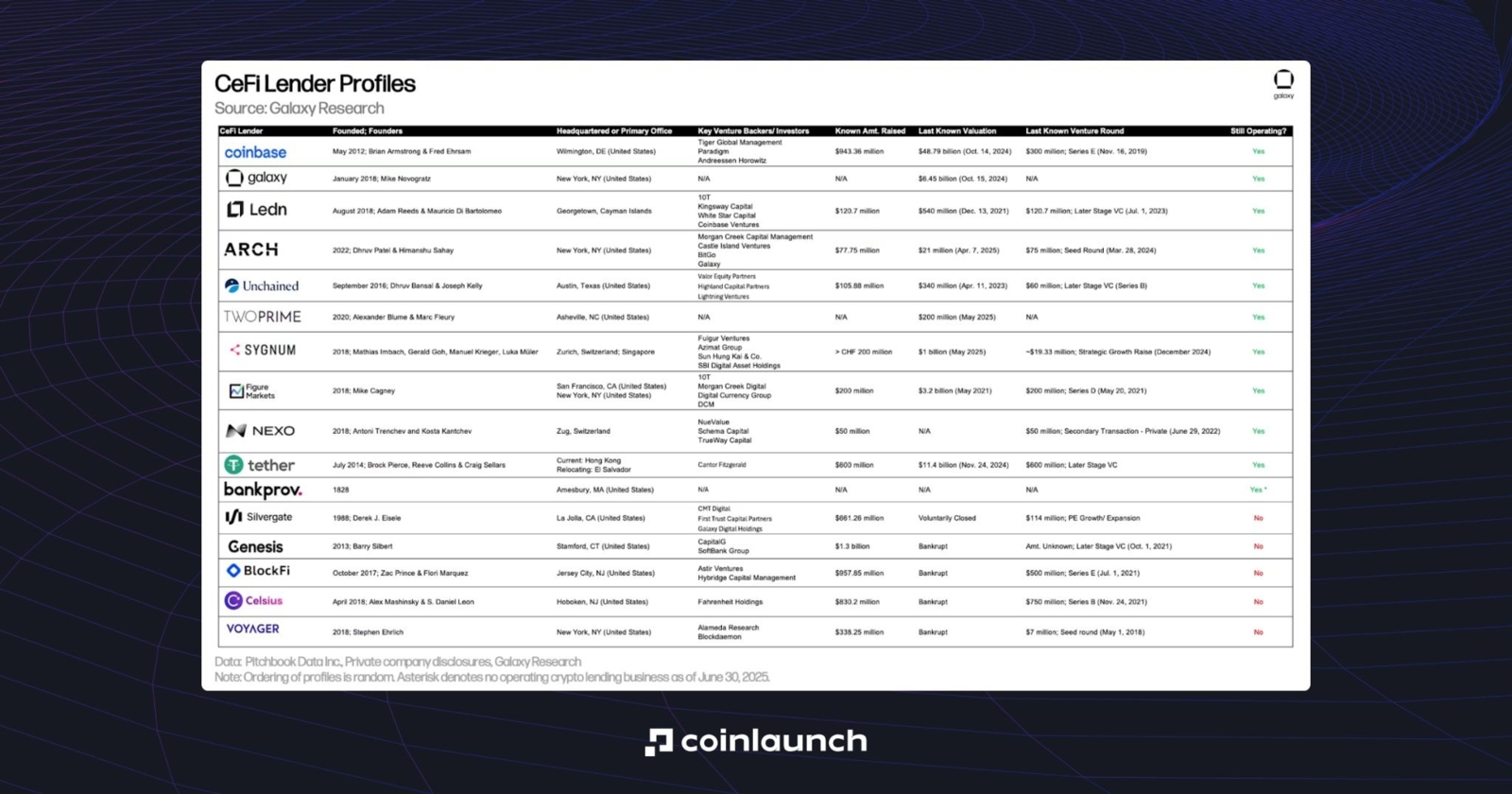

The CeFi segment began to gain popularity in 2018 with the launch of BlockFi, Celsius, Genesis, and Nexo, and reached its peak during the 2021 bull market.

However, the 2022 bear market proved disastrous for the CeFi lending sector. The collapse of the Terra-LUNA ecosystem triggered a “domino effect” that also affected other players in the segment:

- Three Arrows Capital defaulted on its loans to Genesis and Voyager.

- In June 2022, Celsius froze withdrawals and soon filed for bankruptcy.

- Later that year, BlockFi followed suit.

CeFi platforms failed because of the human factor, which had a clear impact during the bear market. To keep big clients, intermediaries most probably ignored liquidation risks and lowered LTV requirements. Ultimately, this could lead to massive liquidity gaps.

DeFi platforms, on the other hand, remained resilient: they automatically enforce loan terms, make no exceptions, and adhere to risk management rules. This is arguably DeFi’s most significant advantage over CeFi.

List of active and defunct CeFi lending platforms. Source: galaxy.com

Today, Nexo, Ledn, and Unchained, as well as leading centralized exchanges, remain among the most active players in this segment.

DeFi Lending: Decentralized Crypto Loans Explained

DeFi platforms remain the choice of true crypto enthusiasts and those who value confidentiality, privacy, and the absence of KYC requirements. This type of borrowing crypto operates without third parties: funds are held in a liquidity pool managed by a smart contract.

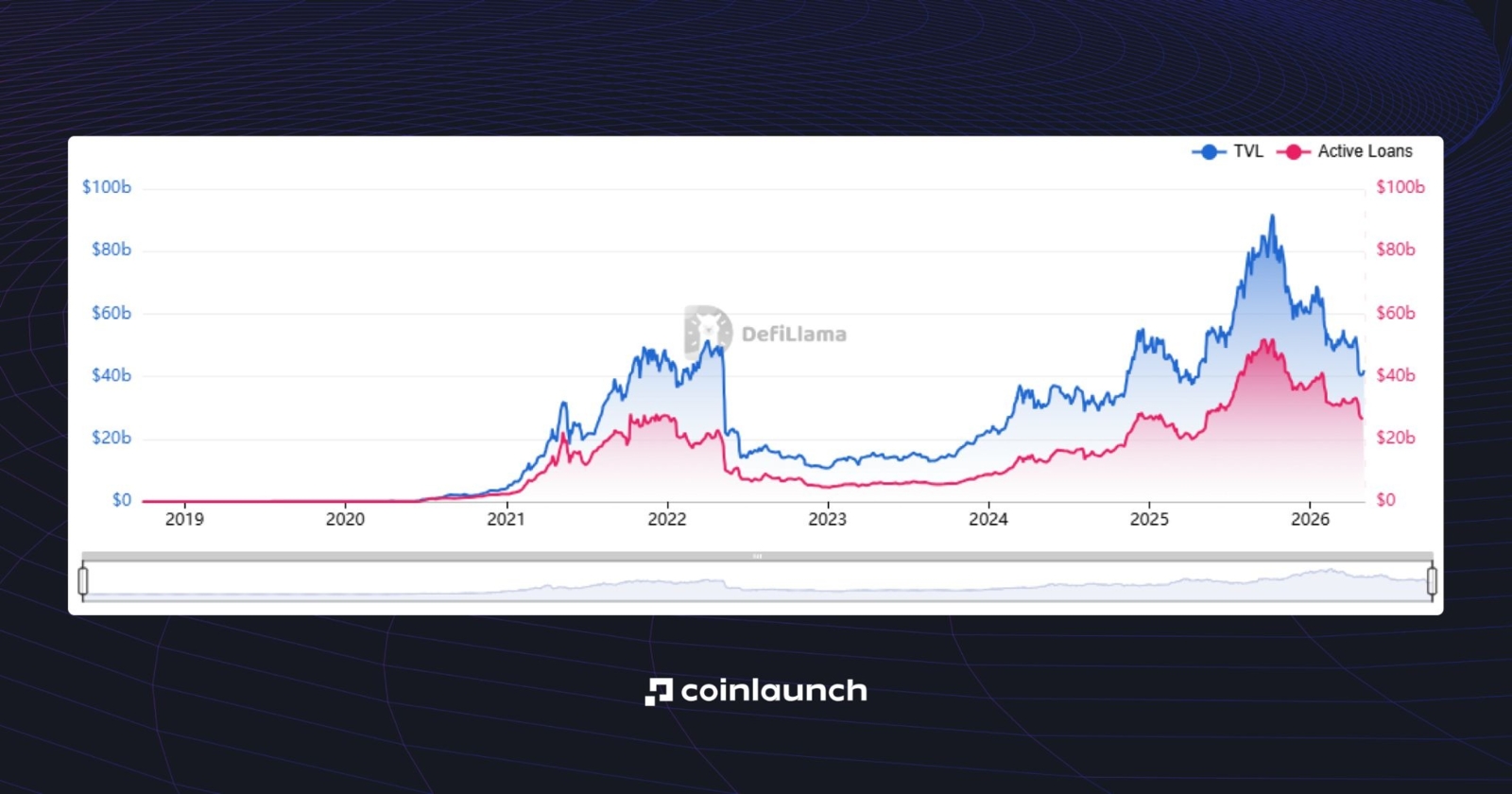

The largest players include Aave, Morpho, Kamino, and others; at the time of writing, the combined TVL (Total Value Locked) of these protocols stands at $42.7 billion. Most of these funds are held on the Ethereum blockchain ($24 billion), as well as on Tron, BSC, and Solana.

Chart showing TVL and active DeFi loans across lending protocols. Source: defillama.com

Interest rates on DeFi loans for crypto are typically variable and are determined algorithmically based on the current load on the lending pools.

DeFi vs. CeFi Lending: A Side-by-Side Comparison

Parameter | CeFi Lending | DeFi Lending |

Asset custody | The platform takes custody of assets and holds them on behalf of the user. | The user interacts with a smart contract through their own wallet. |

Identity verification | KYC required. | No KYC required. |

How loans are issued | Through a centralized company that sets terms and manages the process. | Through a smart contract and liquidity pool. |

How rates are determined | Often set by the platform, sometimes with fixed rates. | Floating and calculated algorithmically based on pool utilization. |

Customer support | Customer support is available. | No traditional customer support. |

Privacy | Lower: the platform knows the customer and controls access. | Higher: the user acts directly through their wallet. |

Control over funds | Lower: assets are held by the platform. | Higher: funds are held in a non-custodial pool. |

Main risks | Counterparty risk, platform bankruptcy, hacks, account freezes. | Risk of hacks, vulnerabilities, and oracle manipulation. |

Crypto Lending Risks

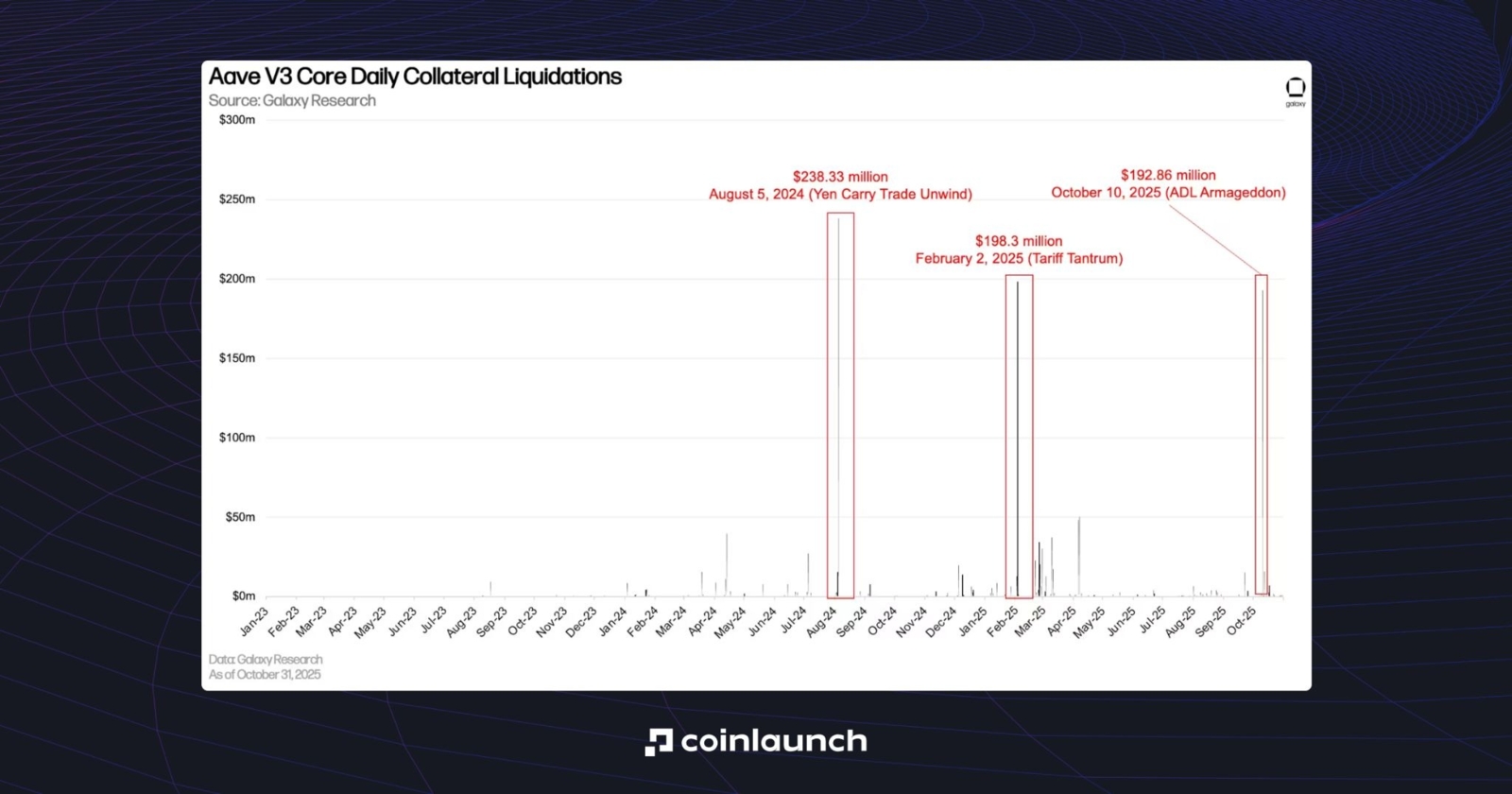

One of the main crypto lending risks are liquidation risks. Since collateral is tied to the market value of the asset, a sudden change in that value can result in the user being unable to provide additional collateral in time, especially if it happens at night.

The most recent major wave of liquidations occurred on October 10, 2025, following the so-called “Trump tariffs.” At that time, users on Aave lost approximately $200 million, making it the third-largest user loss event in the protocol’s history. So, make sure to account for unexpected market conditions when you borrow cryptocurrency.

The largest liquidations on Aave. Source: galaxy.com

Interest rates also remain a volatile factor in crypto lending. This is particularly evident in DeFi: during periods of high demand, they can spike sharply. Imagine your surprise when you open a position at one set of interest rates, only to close it a month later at rates that are twice as high.

Additionally, there is always a risk of hacking in DeFi. In 2021, C.R.E.A.M. Finance suffered a major exploit: the protocol lost approximately $130 million in liquidity. In 2023, Euler Finance fell victim to a flash loan attack, resulting in losses of roughly $197 million. In 2024, UwU Lend was attacked twice: the protocol lost $19.3 million in the first attack and another $3.72 million in the second.

KelpDAO and LayerZero are the most recent examples: on April 18, 2026, $292 million in rsETH was withdrawn, triggering issues at Aave and Compound, where markets were frozen for weeks before normal operations could resume.

How to Choose the Best Crypto Lending Platform

Borrowing against crypto may have been a complicated process back in 2017, but today even a child could figure it out. Amidst rising Web3 adoption around the globe, crypto lending platforms have simplified the process to just a few clicks: the bulk of the work comes down to choosing the right product. The rest is just details.

That choice is no longer trivial. The market now includes dozens of lending products with different terms, risk models, and levels of transparency. For readers who want a more practical comparison, we have also published a separate ranking of the leading crypto lending protocols.

Read more: TOP 10 Crypto Lending Platforms

Start by understanding your needs: if centralization is important to you, choose CeFi platforms like Nexo or Kraken; if decentralization is important, choose DeFi platforms like Aave, Sky, or Morpho.

Additionally, there are aggregators like Sats Terminal: they collect data from the most popular lending platforms on their website, giving users a broader picture of what is happening. At the time of writing, Sats Terminal supports Morpho, Aave, Kamino, Ledn, and Arch.

Crypto Loans: Final Thoughts

Crypto backed loans have evolved from a niche tool in the early days of DeFi into a fully fledged market. The collapse of CeFi platforms in 2022 wiped out part of the industry, but at the same time exposed the weaknesses of the products of that period. Afterward, DeFi confirmed the resilience of its mechanics, CeFi revised its approach to risk, and traditional financial companies began to look in this direction.

Today, crypto lending is a way to obtain liquidity without selling an asset. In certain strategies, such loans are also used to increase market exposure, that is, effectively to increase leverage without directly selling the underlying asset. However, it is not without risks: choosing the wrong protocol or a sharp market movement could result in the liquidation of a position.

So, we’ve looked at how crypto-backed loans work, what has driven the growth of this market, how CeFi and DeFi models differ, and why these products have become an important part of the crypto economy. If regulation becomes even more lenient toward the industry, crypto backed loans have a chance to become a normal part of the broader credit system.

So, if you’ve got the hang of how crypto loans work, share this article with your friends! Your support means a lot to us.

Was this article helpful?

Share this blog post

Research

Daniel Bennett

July 14, 2026

15 min

The 10 Best Web3 Marketing Agencies of 2026, Ranked by 220+ Verified Reviews and Real Case Data

Research

Daniel Bennett

July 10, 2026

20 min

Crypto Narratives 2026: SpaceX, HYPE, Zcash, Stablecoins, and ANSEM

Research

Daniel Bennett

July 7, 2026

11 min

USDC Lending: How to Borrow and Lend USDC

No Comments

No comments yet