Table of contents

- What Are Bitcoin Backed Loans?

- Types of Bitcoin Lending Platforms

- Centralized Bitcoin Lending Platforms

- Peer-to-Peer and Decentralized Bitcoin Lending Protocols

- How Does Borrowing Against Bitcoin Actually Work?

- LTV (Loan-to-Value) and Bitcoin Lending Rates

- How LTV Changes When Bitcoin Price Moves

- Margin Calls and Liquidation: What Happens If Bitcoin Price Drops?

- The Best Way to Borrow USD Against Bitcoin in 2026

- How to Borrow Against Bitcoin: Step-by-Step Guide

- Borrowing Against Bitcoin vs. Selling: Core Benefits

- Final Thoughts: Is a Bitcoin Loan Right for You?

Table of contents

- What Are Bitcoin Backed Loans?

- Types of Bitcoin Lending Platforms

- Centralized Bitcoin Lending Platforms

- Peer-to-Peer and Decentralized Bitcoin Lending Protocols

- How Does Borrowing Against Bitcoin Actually Work?

- LTV (Loan-to-Value) and Bitcoin Lending Rates

- How LTV Changes When Bitcoin Price Moves

- Margin Calls and Liquidation: What Happens If Bitcoin Price Drops?

- The Best Way to Borrow USD Against Bitcoin in 2026

- How to Borrow Against Bitcoin: Step-by-Step Guide

- Borrowing Against Bitcoin vs. Selling: Core Benefits

- Final Thoughts: Is a Bitcoin Loan Right for You?

Bitcoin collateral loans are one of the most useful tools in cryptocurrency finance. They allow users to obtain additional liquidity by choosing to borrow against Bitcoin instead of selling the asset. This tool is popular among both novice and seasoned investors.

Borrowing can also help avoid paying taxes, depending on local tax laws. A loan against Bitcoin is not considered a taxable event, unlike a sale. Therefore, some investors prefer to get a Bitcoin loan and pay interest rather than sell the asset and pay up to 20% federal capital gains tax.

But how do you get a Bitcoin loan? This article explains how.

What Are Bitcoin Backed Loans?

First, let’s break down: what is a Bitcoin backed loan?

Bitcoin backed loans are a type of crypto loans in which BTC serves as collateral. These transactions are popular among long-term investors, large whales, and institutional players who hold digital gold. This is due to Bitcoin’s status among the market’s giants, unlike Ethereum and Solana, which are more commonly used as collateral by DeFi enthusiasts.

As with other crypto loans, users can borrow against Bitcoin through specialized services. The user deposits a certain amount of BTC, and the system calculates how much they can borrow. The amount depends on BTC’s market value and the Bitcoin lending rates of the specific platform.

Related: What is Crypto Lending & How to Loan Against Your Crypto?

During the loan term, your locked BTC is stored either within the protocol in the case of DeFi Bitcoin borrowing or in the wallets of a custodial service in the case of CeFi. You remain the owner of these assets, but you cannot transfer or sell them until you have repaid the principal and any additional Bitcoin lending rates.

This way, you maintain exposure to the assets without selling them. In exchange, you pay APR (Annual Percentage Rate), the total annual cost of the loan, including interest and fees. Rates typically range from 7% to 12% APR: for example, a Bitcoin backed loan at Arch starts at 7.25%, while Ledn starts at 11.9%, dropping to 9.99% for large loans.

Types of Bitcoin Lending Platforms

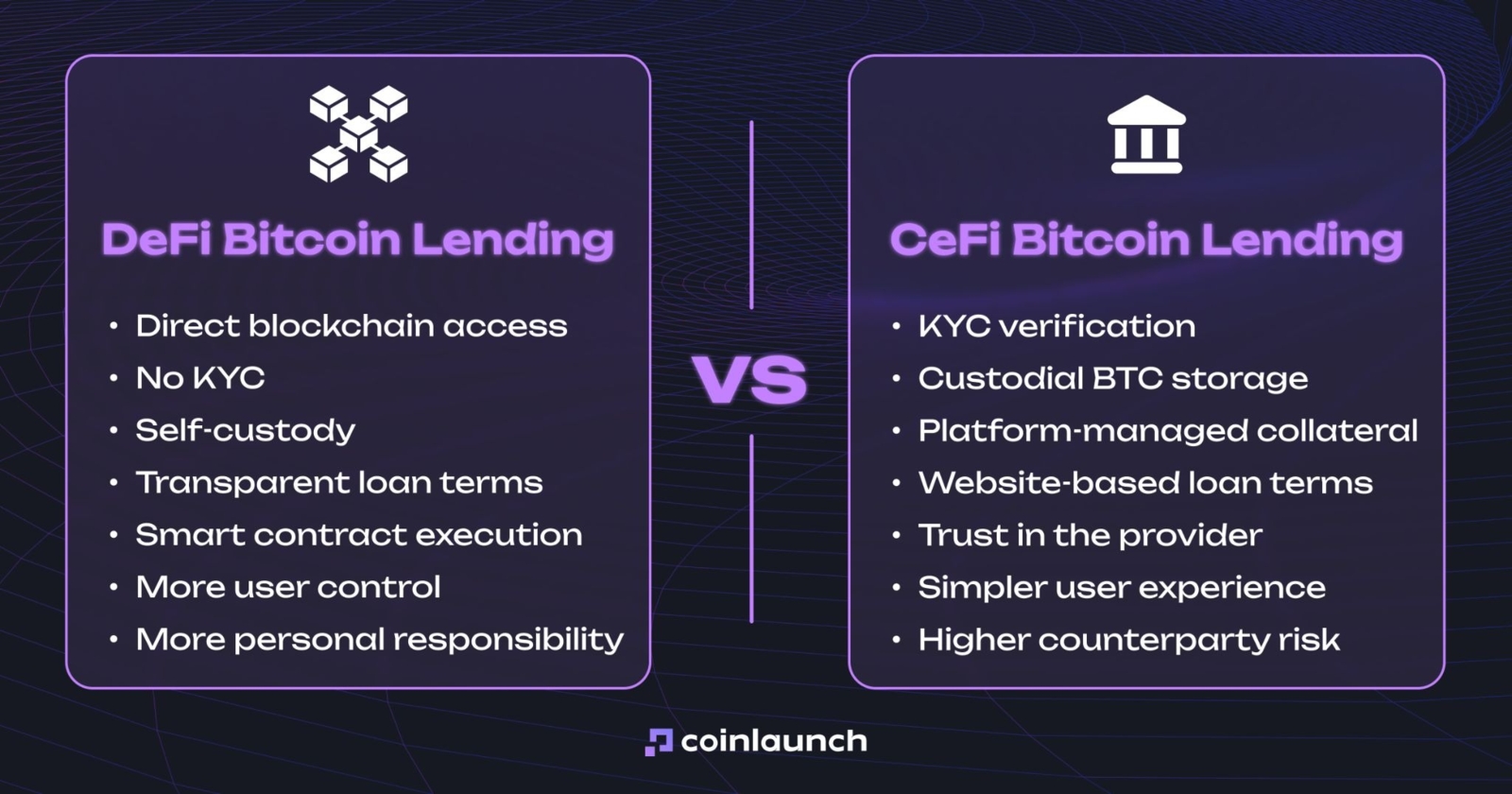

As with everything in crypto, Bitcoin lending platforms are usually divided into CeFi and DeFi. With DeFi, the user interacts with the blockchain directly: they do not disclose their identity, do not give up custody of their funds, and the loan terms remain transparent. On the CeFi side, the user completes KYC, transfers BTC to a custodial service, and trusts the platform to follow the terms listed on its website.

The difference between DeFi and CeFi Bitcoin lending. Source: coinlaunch.space

This is the main difference in CeFi vs DeFi Bitcoin lending. Loan terms, interest rates, and liquidation rules also vary by platform. In CeFi, the initial LTV for BTC is usually around 50%, and the user typically receives a margin call before the position is forcibly closed. In DeFi, max LTV can be higher, but the position is liquidated automatically.

You can also use aggregator platforms like Sats Terminal. They consolidate offers from multiple Bitcoin lending platforms in a single interface and make it easier to compare terms without manually checking each platform.

Centralized Bitcoin Lending Platforms

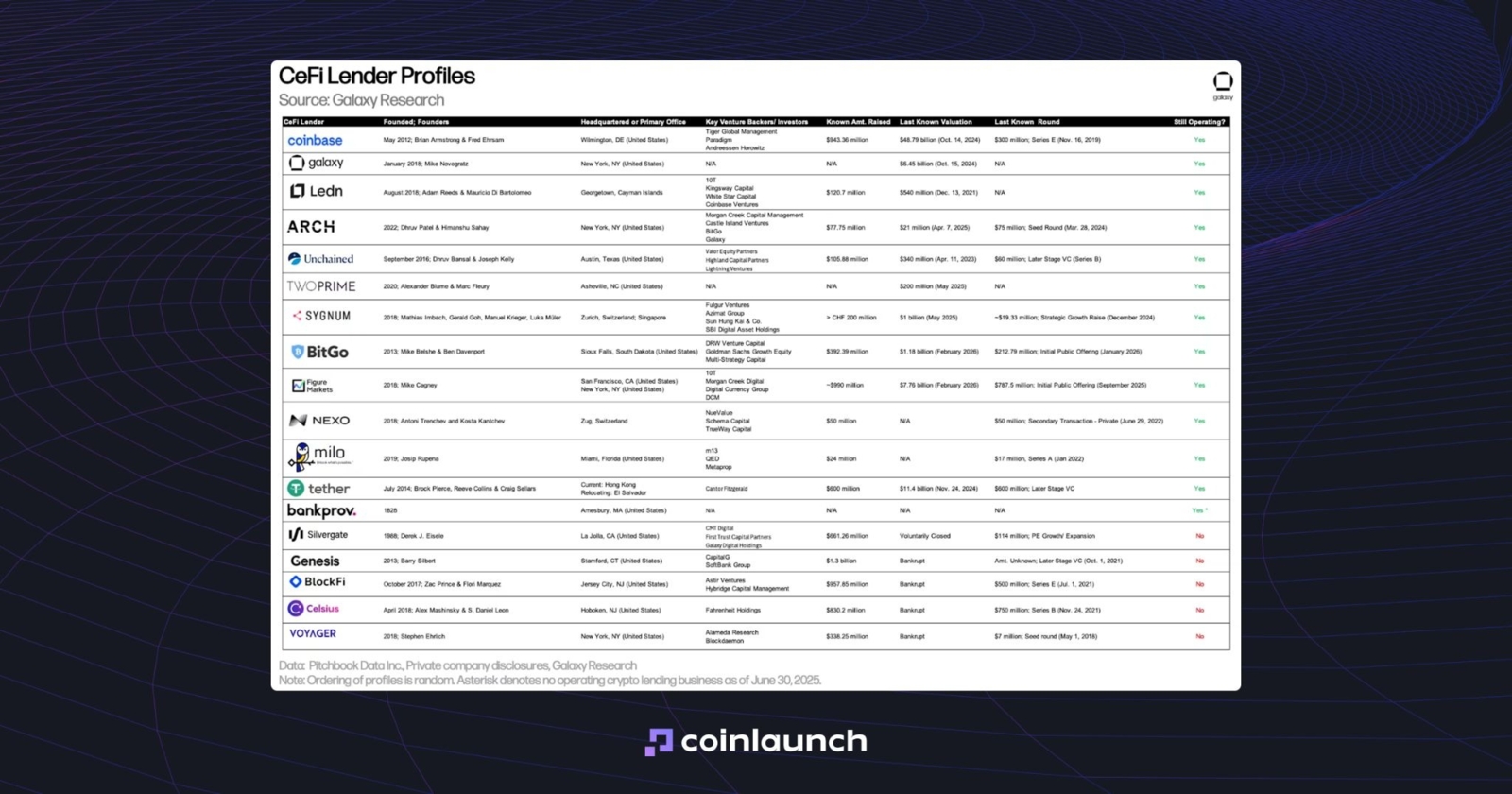

Centralized Bitcoin lending platforms are typically integrated into crypto exchanges like Binance or Coinbase rather than operating as standalone services. At the same time, standalone platforms like Ledn, Nexo, and Arch remain the most popular CeFi options for Bitcoin loans.

CeFi platforms stand out for their intuitive UI/UX and customer support. They usually have Google ratings and reviews on Trustpilot. But they are less transparent: even if a website claims 100% Proof of Reserves and no rehypothecation, that does not guarantee the claims are completely accurate.

Profiles of the best-known CeFi Bitcoin lending platforms. Source: galaxy.com

Celsius had positive reviews at the time, but that did not prevent its bankruptcy. In April 2021, Celsius won Best Cryptocurrency Wallet at the FinTech Breakthrough Awards, and in October that same year, it raised $400 million from WestCap and CDPQ.

The press release described Celsius as a “leading global cryptocurrency earning and borrowing platform.” Nine months later, the company filed for bankruptcy and disclosed a $1.19 billion balance-sheet shortfall in its bankruptcy filing.

Other CeFi players met a similar fate:

- BlockFi was named to the 2021 Forbes Fintech 50, reached a $3 billion valuation, and had $20 billion in assets under management. In November 2022, however, it filed for bankruptcy due to its ties to FTX and Alameda, after Alameda failed to meet its obligations on $680 million in secured loans.

- In 2021, Voyager Digital described itself as a “transparent, safe, secure, and trusted personal cryptocurrency platform.” In July 2022, it filed for bankruptcy after Three Arrows Capital defaulted on a loan of 15,250 BTC and $350 million in USDC.

- Genesis Global Capital was one of the largest Bitcoin lending platforms. In January 2023, it filed for bankruptcy amid the fallout from 3AC and FTX, owing approximately $3.4 billion to its 50 largest creditors.

By the end of 2025, total outstanding CeFi loans across all collateral types (not only Bitcoin collateral) stood at $27.5 billion. DeFi loans totaled $33.5 billion. In other words, the gap in CeFi vs DeFi Bitcoin lending is relatively narrow.

Peer-to-Peer and Decentralized Bitcoin Lending Protocols

A key feature of decentralized Bitcoin lending protocols is their independence from human intervention. The platform’s creators cannot influence the protocol’s operations: they cannot decide who gets approved for a loan, who gets rejected, or on what terms. Human mismanagement, which likely contributed to the collapse of CeFi platforms, is eliminated in DeFi.

However, this does not mean that taking out a loan against Bitcoin in DeFi is completely safe. Protocols remain vulnerable to hacks, oracle manipulation, and issues with wrapped BTC, which is how BTC most often enters DeFi.

For example, in 2023, Euler Finance lost approximately $197 million in a flash loan exploit, with wBTC among the stolen assets. In 2024, UwU Lend first lost $19.3 million, including WBTC, and suffered a second hack a few days later, losing another $3.7 million. That same year, Radiant Capital lost over $50 million in an attack on its lending protocol.

In DeFi protocols, BTC is represented by wrapped tokens on other blockchains. BTC is locked on the source network, while new tokens, WBTC, are minted on the target network.

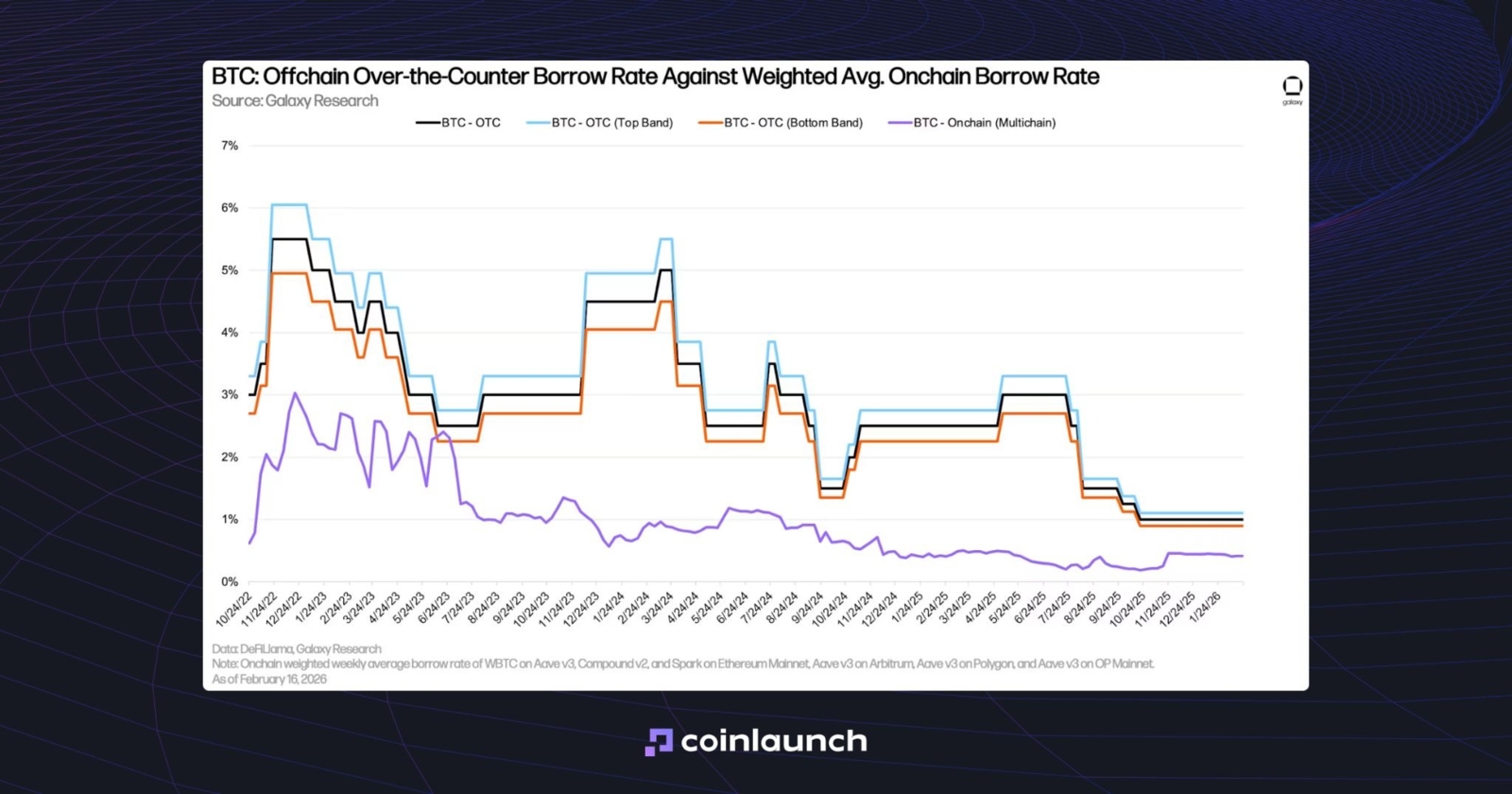

DeFi Bitcoin borrowing rates for WBTC are typically lower than off-chain and OTC rates for BTC. This is because wrapped Bitcoin in DeFi is more often supplied as collateral than borrowed, which keeps demand for borrowing WBTC lower. By the end of 2025, the on-chain borrowing rate for BTC had risen from 0.22% to 0.44%, while OTC rates over the same period fell from 1.25% to 1%.

OTC Bitcoin borrow rate vs Avg. onchain borrow rate. Source: galaxy.com

The gap persists because, in the OTC market, BTC is used not only as collateral for cash and stablecoin loans but also to short BTC. In DeFi lending, that demand is virtually nonexistent.

How Does Borrowing Against Bitcoin Actually Work?

This section explains how does borrowing against Bitcoin work, including the key variables involved in the process, how loan terms are determined, and how liquidation and margin call thresholds are calculated.

LTV (Loan-to-Value) and Bitcoin Lending Rates

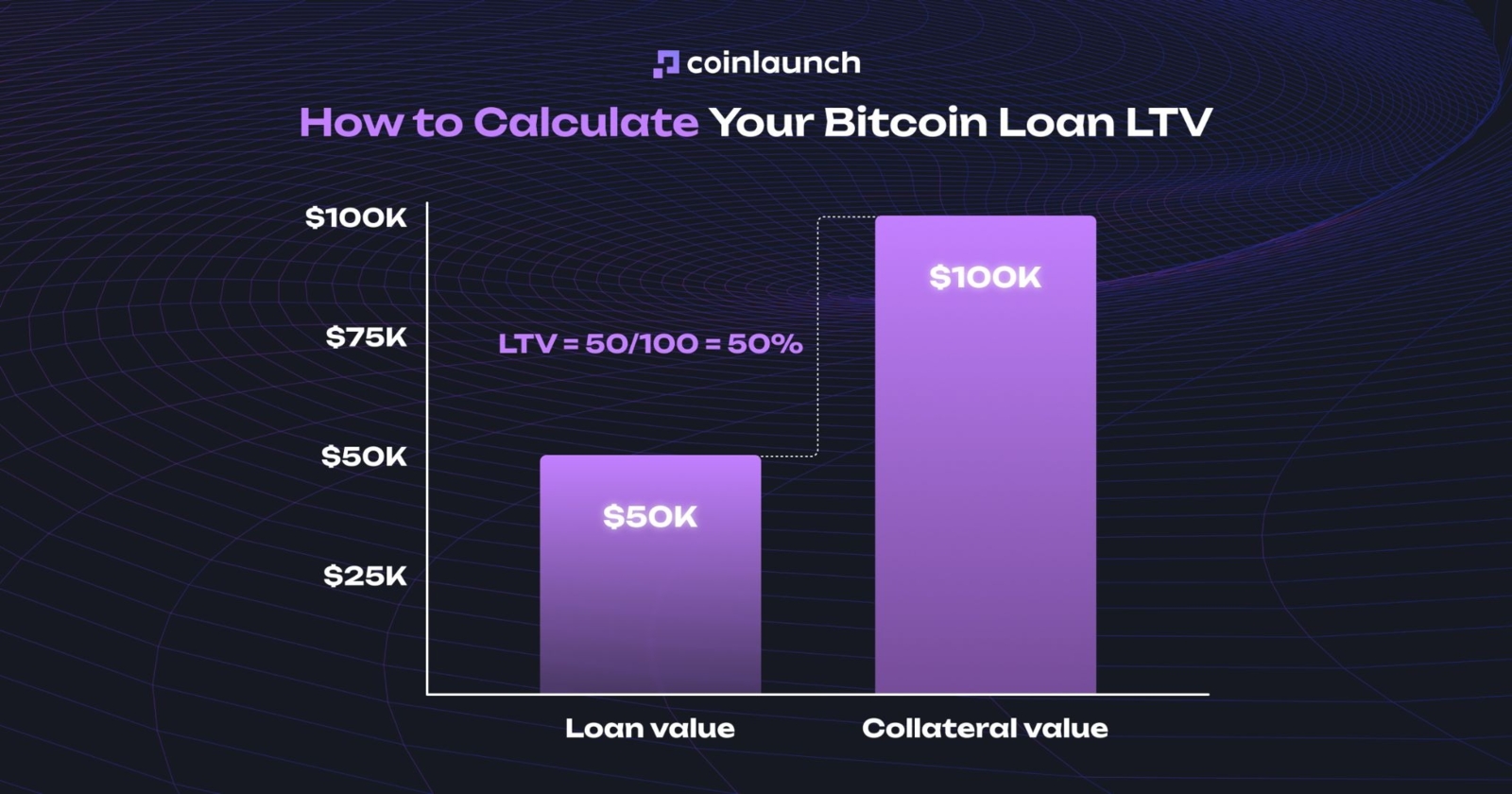

The LTV (loan-to-value) ratio determines the maximum loan amount available against collateral. LTV is calculated as the ratio of the loan amount to the collateral value. For example, a loan against BTC with an LTV of 50% lets you borrow a dollar amount equal to half the market value of Bitcoin. A Bitcoin loan backed by 1 BTC at a price of $100,000 would therefore provide $50,000 in loan funds.

How to calculate Bitcoin loan LTV. Source: coinlaunch.space

Many Bitcoin lending platforms quote interest rates annually as APR. For example, on a $50,000 loan with a 10% APR, the borrower pays $5,000 per year. Depending on the platform, interest is paid regularly, for example, once a month, or as a lump sum at maturity. If the borrower defaults, the lender may demand repayment, charge additional fees, or liquidate the collateral to cover the loan.

That said, most Bitcoin loans are open-ended: they have no fixed maturity date. This means you can keep the loan as long as you maintain sufficient collateral and pay interest. However, keep in mind that a sharp change in BTC’s market value could worsen your position.

How LTV Changes When Bitcoin Price Moves

If the price of BTC rises, the loan’s LTV decreases. The value of the user’s collateral increases, and liquidation risk falls. This allows the user to borrow more against the same collateral. For example, if Bitcoin rises to $200,000, the loan’s LTV will drop from 50% to 25%.

If the price of BTC falls, the LTV rises. This means the borrower will need more collateral to borrow the same amount. For an existing position, however, LTV becomes the variable that determines the margin call level, the specific LTV ratio at which additional collateral must be deposited, or the liquidation level, at which the lender can liquidate the collateral to cover the loan.

Margin Calls and Liquidation: What Happens If Bitcoin Price Drops?

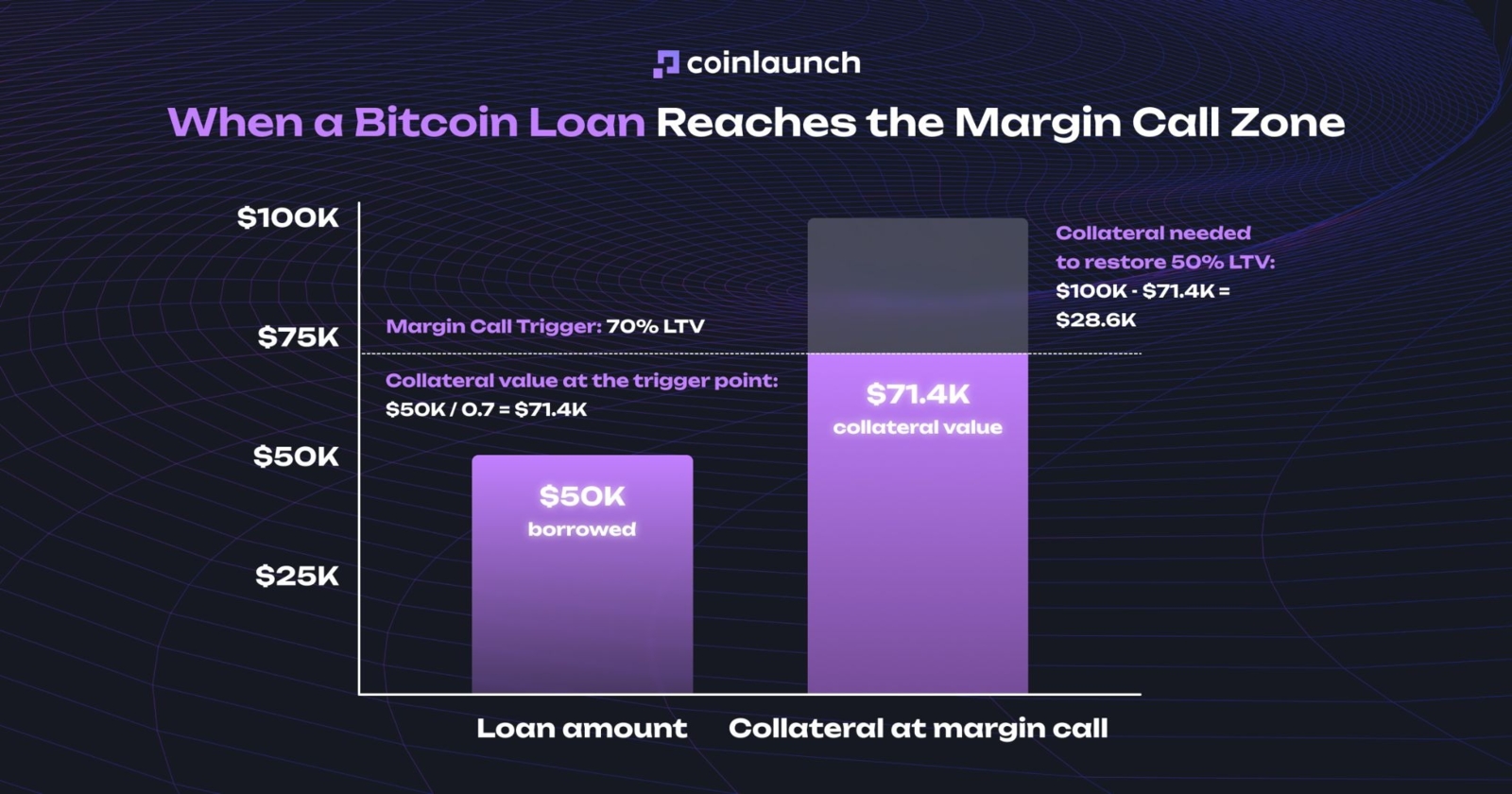

A margin call typically triggers at 70% LTV. When LTV reaches this threshold, the platform requires the borrower to add collateral and bring the position back to its initial LTV. Borrowers are typically given 3–5 days to meet this requirement.

In our example, a margin call triggers at 70% LTV. For a $50,000 loan, this happens if the collateral value drops to $71,429. To bring the position back to the initial 50% LTV, the borrower needs to add $28,571 in collateral. With Bitcoin priced at around $71,400, this equals approximately 0.4 BTC.

When a Bitcoin loan reaches the margin call. Source: coinlaunch.space

If the user fails to meet the margin call requirements and the collateral value continues to fall, the Bitcoin lending platform has the right to forcibly close the position: it will sell the collateral to cover the Bitcoin loan provided. This sale is called liquidation.

Liquidation most often triggers at 80% LTV. In our example, this happens when the collateral value drops to $62,500. The platform then sells $50,000 worth of Bitcoin to close the BTC loan, and the remaining collateral, 0.2 BTC minus interest, is returned to the borrower.

The Best Way to Borrow USD Against Bitcoin in 2026

Let’s get this out of the way: there’s no one-size-fits-all answer to the question “Whats the best way to borrow against my Bitcoin”. There are many players in the market, and each focuses on its own metrics. So instead of searching for the perfect solution, it’s better to choose a product that fits your specific needs.

It makes more sense to start with an aggregator like Sats Terminal. It consolidates Bitcoin lending platforms in a single interface and displays key metrics: LTV, interest rate, fees, loan type, and liquidation terms. The platform also handles the technical side of the process: users deposit BTC on the Bitcoin network without bridging or buying WBTC. Sats Terminal then automatically selects a lending option, whether it’s a Morpho or Aave BTC loan, and delivers USDC on an EVM network.

For the convenience and simplicity of a CeFi product, you can use Ledn or Nexo. Ledn works more like a traditional crypto loan: Ledn BTC loan LTV is 50%, with fixed APR and early repayment without penalties. Nexo operates as a credit line: users manage their collateral, partially repay the debt, and borrow again without fully closing the position.

If you want to keep your Bitcoin collateral as secure as possible, look into Unchained. The platform stores BTC in a 2-of-3 multisig wallet, the borrower holds one key, and the collateral itself is not rehypothecated.

How to Borrow Against Bitcoin: Step-by-Step Guide

The process of borrowing against Bitcoin is easiest to explain through a specific example. Let’s use the Sats Terminal aggregator mentioned earlier: it is a convenient way to see how term selection, wallet connection, and loan management work. We’ll show how to borrow against Bitcoin on this platform, but you can use any service that best suits your needs.

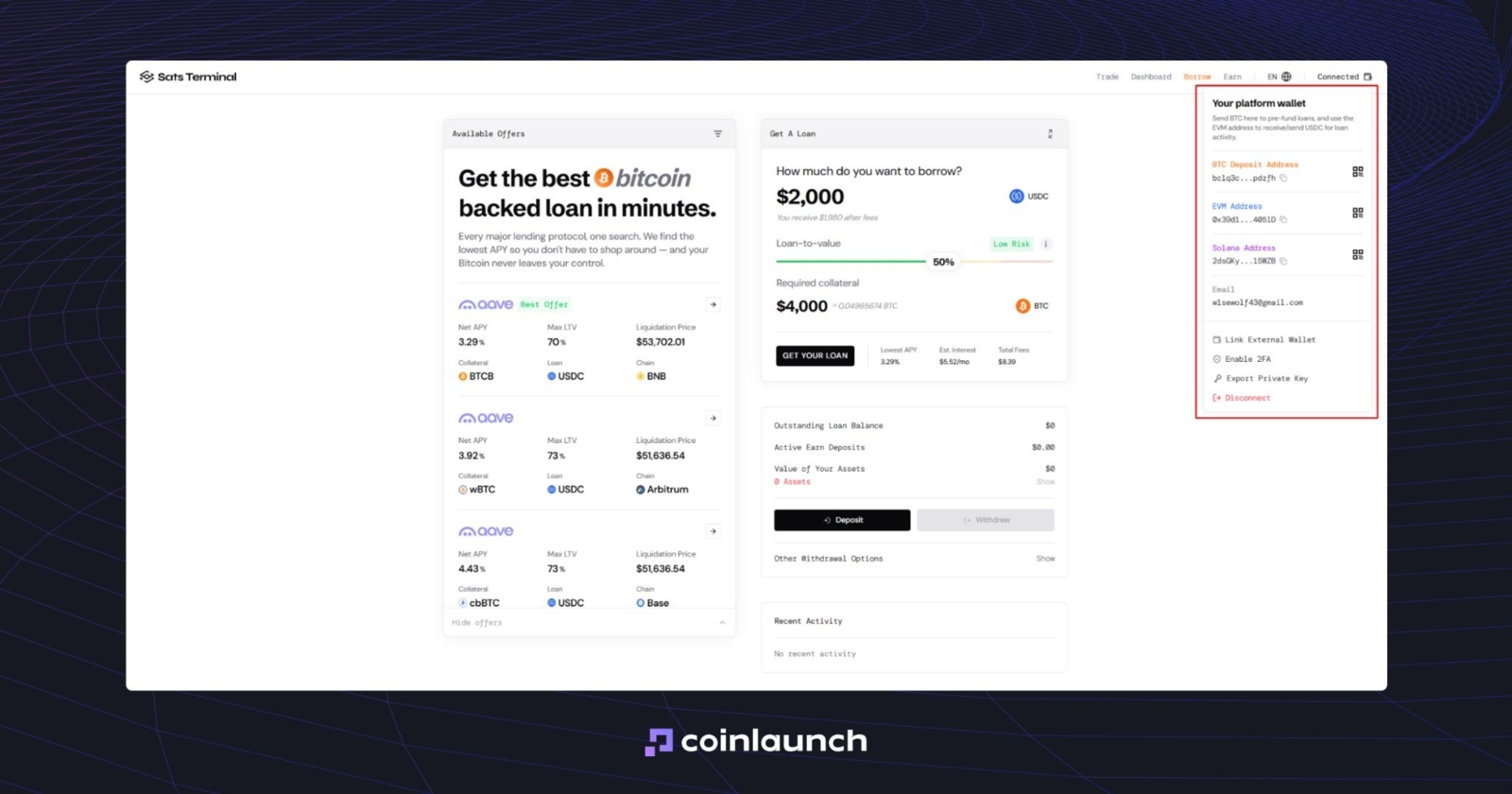

First, open the aggregator’s webpage and connect your cryptocurrency wallet. Sats Terminal will ask for an email address: enter it, confirm it with a one-time code, and proceed. At this stage, a personal Privy wallet is already created for you. No KYC is required: this is literally a BTC loan without verification.

Cryptocurrency wallet on the Sats Terminal platform. Source: satsterminal.com

Next, specify the amount of the BTC collateral loan. By default, Sats Terminal suggests $2,000, but you can change this value manually: use the built-in BTC loan calculator and enter the desired amount.

Below is the loan-to-value (LTV) slider. Use it to select the LTV at which you want to open the position. The platform classifies loans with an LTV of up to 50% as Low Risk, up to 65% as Medium Risk, and anything above that as High Risk. If the collateral value drops, the platform may request additional collateral or liquidate the position.

The collateral value falls along with the asset price. This is one reason why, on Sats Terminal, you can only get BTC loan: the user deposits BTC and receives USDC.

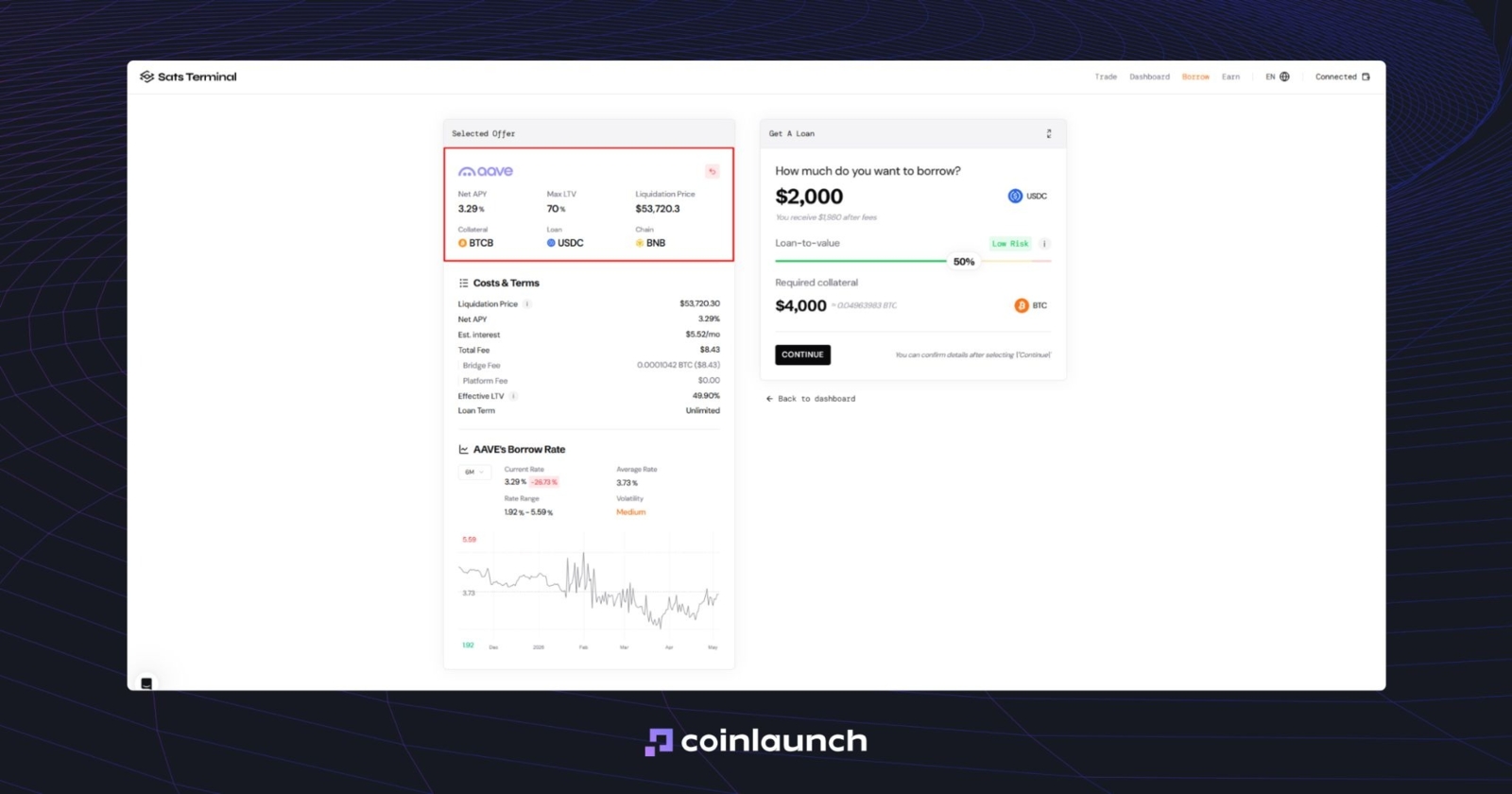

On the left, you’ll see a list of available positions for a loan against Bitcoin. Net APY shows the total annual rate, including costs and returns. Max LTV is the maximum ratio of the loan amount to the collateral value. Liquidation Price is the asset price at which the platform will forcibly close the position.

Net APY, Max LTV, and Liquidation Price metrics on Sats Terminal. Source: satsterminal.com

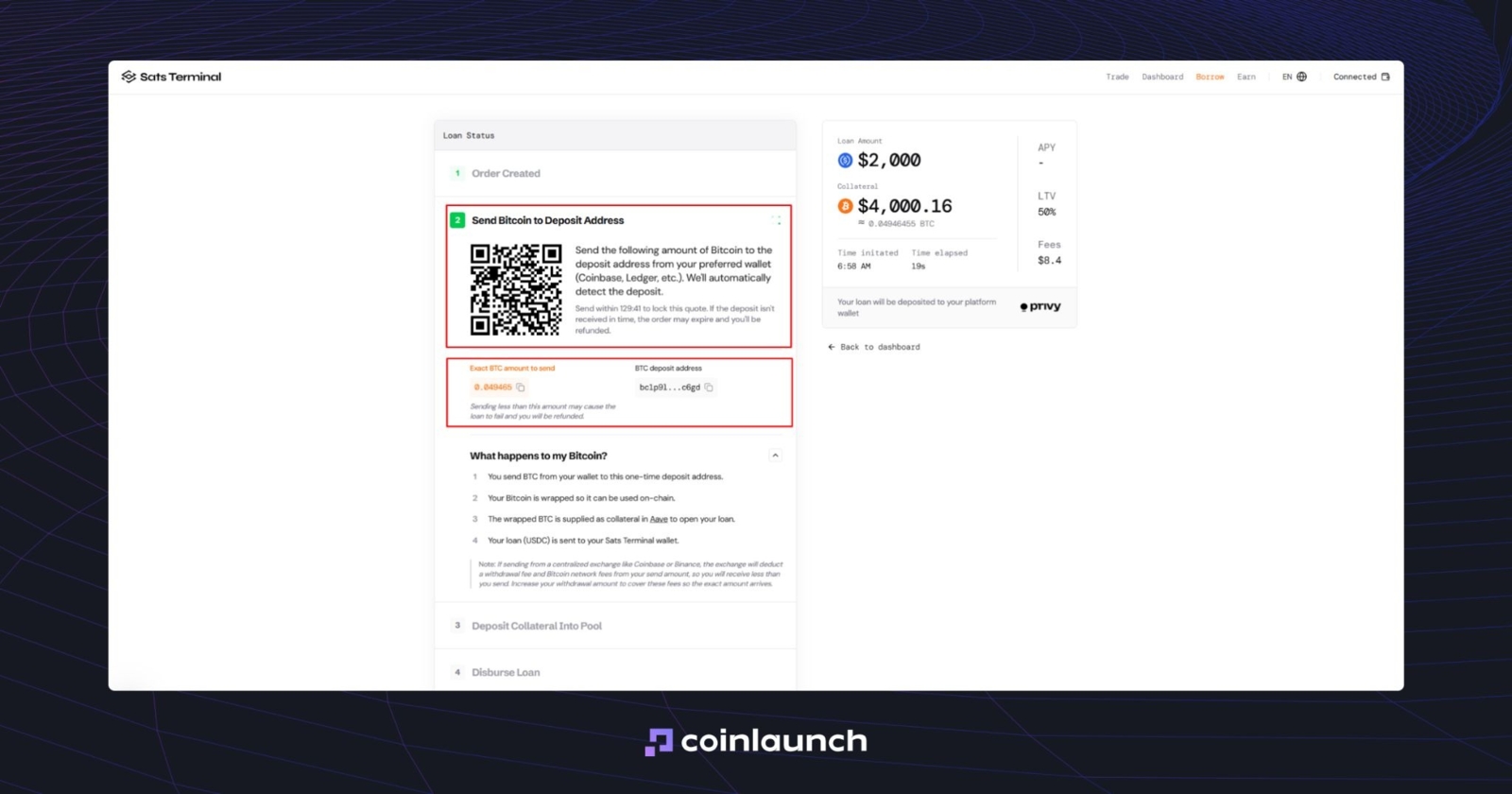

If the selected offer fits your needs, click “Continue.” Sats Terminal will then generate a unique BTC address for the loan. Transfer funds from your wallet or exchange. It is important to send the exact amount specified in the order: you can either enter the address manually or scan the QR code.

An interface for obtaining a crypto loan by transferring collateral to a unique BTC address. Source: satsterminal.com

First, BTC is sent to a one-time deposit address. The asset is then converted into the format required by the selected protocol, such as wBTC on Ethereum, cbBTC on Base, or BTCB on BSC. It is then used as collateral on Aave or another selected crypto lending platform to secure a loan.

In the final step, USDC is credited to your Sats Terminal wallet. From there, you can withdraw the funds to your personal wallet, send them to an exchange, or convert them into cash.

So, if someone asks, “Can you borrow against Bitcoin?”, the answer is yes. Sats Terminal and other Bitcoin lending platforms make this possible in just a few clicks.

Borrowing Against Bitcoin vs. Selling: Core Benefits

The main advantage of borrowing against Bitcoin is liquidity without having to sell the asset. Why you need the extra funds and how you use them is up to you. But if you need to repair your car, pay a doctor’s bill, or buy a new computer, a BTC-backed loan instead of selling your BTC allows you to get the money you need while maintaining exposure to the asset.

Borrowed liquidity can also be used to hedge a BTC position. For example, you hold 1 BTC with an average purchase price of $50,000, and the current market price is around $77,639. If you expect a decline, you can open a short position in the futures market to partially offset the downside risk.

If BTC drops, the loss on the spot position will be offset by profit from the short position, but this protection comes with costs: the Bitcoin loan’s APR, trading fees, a potential funding rate, and liquidation risk if the price moves against your position or the loan’s LTV rises sharply.

Final Thoughts: Is a Bitcoin Loan Right for You?

If you need liquidity but don’t want to sell your BTC, you can borrow against Bitcoin: you receive USD, maintain exposure to the asset, and avoid locking in a sale. This is useful for long-term investors who need funds for expenses, business, hedging, or portfolio management without exiting Bitcoin.

But a Bitcoin loan isn’t free liquidity. It is a loan with risks. Before opening a position, you need to understand LTV, APR, margin call and liquidation thresholds, collateral storage rules, and the platform’s model.

If you’re not prepared to monitor the BTC price, top up your collateral, and pay interest on the loan, selling part of your position might be a better fit. If you are, start by comparing terms through Sats Terminal or another Bitcoin lending platform and choose the product that’s right for you.

Was this article helpful?

Share this blog post

Research

Daniel Bennett

July 14, 2026

15 min

The 10 Best Web3 Marketing Agencies of 2026, Ranked by 220+ Verified Reviews and Real Case Data

Research

Daniel Bennett

July 10, 2026

20 min

Crypto Narratives 2026: SpaceX, HYPE, Zcash, Stablecoins, and ANSEM

Research

Daniel Bennett

July 7, 2026

11 min

USDC Lending: How to Borrow and Lend USDC

No Comments

No comments yet